The tax reform has finally passed and to see whether it will fundamentally change markets and the economy, we need to look at three different factors. The Federal Reserve (Fed) interest rate agenda, the political implications for the 2018 mid-term elections and the actual effect on business spending, consumer spending, and economic growth.

Because the Fed’s policy dominates markets still many looked at the central bank to see whether the tax bill will have an effect on its policy.

Gradualism in hikes for 2017 didn’t hurt risk assets and a continuation of the same policy will likely keep equities bid, while not helping the dollar that much. The key comment from the departing FOMC Chair Yellen regarding the tax reform: “My colleagues and I are in line with the general expectation among most economists that the type of tax changes that are likely to be enacted would tend to provide some modest lift to GDP growth in the coming years,” Yellen said during her final news conference in December. It does not sound it will change the Fed’s rate hiking schedule.

Then there is politics. The public needs to decide how to balance growth against deficits. In economic terms, we may be reaching the level of Ricardian equivalence where tax cuts no longer push up expectations for growth given the need for future debt payments and taxes to cover them.

The divide of support remains one linked to partisanship as the New York Times highlights in its polls over last week. The net result is that the boost for Republicans into the mid-terms next year will have to pivot on the economy reacting to this change and responding as they expect with faster growth. The difference between 3 percent and 4 percent growth in the United States seems to be the dividing line not just for the Fed or the public but also political parties.

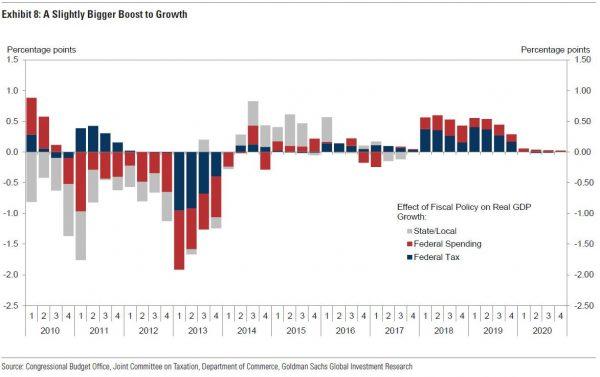

However, the real economy can benefit even in the late stages of an upswing. The biggest argument against the tax reform effect on the real economy is that labor markets are at or above capacity. This suggests we are due for inflation but so far none of that has been obvious to the Fed or the rest of the world.

The offset to increasing labor pressure is corporate investment with the deregulation campaign already showing some effect in 2017. And the ability to encourage more spending through the immediate depreciation of capital goods and other shifts may be underestimated. Most of Wall Street sees the net growth effect positive with the plan, but for how long remains a question.

In the final analysis, the United States economy is in the late stages of a long recovery. The tax reform will extend that until we see serious inflation leading to more aggressive Fed rate hikes. For now, the set up into 2018 is robust with 4 percent growth rather than 3 percent the more likely outcome.