Trump wants to dismantle Obama's bank regulations, saying they hurt the economy

US President Barack Obama signs the Dodd-Frank Wall Street Reform and Consumer Protection Act alongside members of Congress, the administration and US Vice President Joe Biden(L) at the Ronald Reagan Building in Washington, DC, July 21, 2010. The Trump administration may repeal the Act, which has come under fire for slowing down the economic recovery. SAUL LOEB/AFP/Getty Images

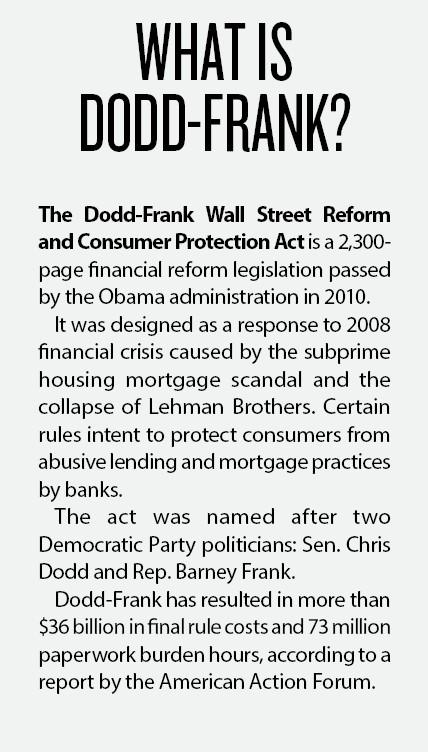

The Dodd-Frank Act, a massive compilation of banking regulations enacted in 2010, was meant to prevent another financial crisis like 2008 by promoting a safer and fairer banking system. Obama called it the most significant financial reform since the 1930s. But the Trump administration wants to repeal the act.

*

Emel Akan

Senior Reporter

Emel Akan is a senior White House correspondent for The Epoch Times, where she covers the policies of the Trump administration. Previously, she reported on the Biden administration and the first term of President Trump. Before her journalism career, she worked in investment banking at JPMorgan. She holds an MBA from Georgetown University.