Many believe that by year-end the United States will be in a recession. On March 31 both the 2-year and 10-year Treasury yields inverted, which is typically a signal that a recession looms ahead. While an inverted Treasury yield certainly creates a large ripple effect amongst economy watchers, the vast amount of money printed over the past two years is actually far worse than an inverted yield curve. Furthermore, a number of S&P 500 stocks just concluded their worst quarter ever, and technology stocks lost close to $2 trillion in market valuation.

The mix of COVID-19 related stimulus and an increase in the money supply have sent a shock to the United States economy. Inflation alone stifles growth, but with rising commodity prices, supply and demand problems, and the Russian-Ukrainian war, you have the potential for a proper disaster on your hands, let alone a recession.

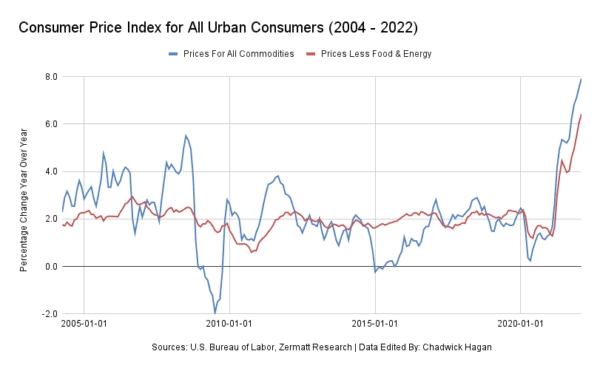

Inflation is already well out of hand, hitting 7 percent in some sectors. The Federal Reserve Bank of San Francisco admitted the measure to combat COVID created more inflation than the Fed could handle, stating in a March 28 release: “Estimates suggest that fiscal support measures designed to counteract the severity of the pandemic’s economic effect may have contributed to this divergence by raising inflation about 3 percentage points by the end of 2021.”

The Sahm Rule signals the start of a recession when the three-month moving average of the national unemployment rate increases by 0.50 percentage points from its low over the previous 12 months. Regardless of a major or minor recession, it is becoming a steady rule that readings of 0.5 or above indicate a recession.

Regardless, investors are worried. An inverted yield curve means investors are more worried about the immediate future than the longer term. While this does not mean that a recession is around the corner or that a recession is even happening for that matter, what it does mean is that the professional investor class is worried.

Furthermore, America’s economy is driven by sentiment and confidence. Small to medium-sized business owners hold off on investment into enterprises when they have low confidence in the economy. This creates a domino effect. When business owners and investors have low confidence in the short term, less money is deployed into investments and enterprises, and economic growth stalls.

It is worth noting that the National Bureau of Economic Research (NBER) considers a recession to be “a significant decline in economic activity spread across the market, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.”

Simply put a recession is a reduction in economic activity over a period of time. Inflation alone can cause a recession. Any more headwinds could be disastrous, including policy hiccups while the Federal Reserve raises rates and simultaneously tries to contain inflation.

Instead of fiscal austerity or price controls maybe we should do away with tariffs and unnecessary taxes on certain items, therefore making them cheaper. After all, as prices rise faster than wages increase, buying and spending grind to a halt.