NEW YORK—The biggest economic news of the year, so far, has been inflation—the highest in 40 years—and the Federal Reserve’s (Fed’s) efforts to fight it. And while there have been lots of finger-pointing at causes—from President Joe Biden’s fossil fuel policies to the war in Ukraine—all of which are at least somewhat true—there are myriad other causes that the media tends to ignore and that we need to address to tamp down the current inflation and avoid it in the future.

The Federal Reserve Balance Sheet Is Way Too Big

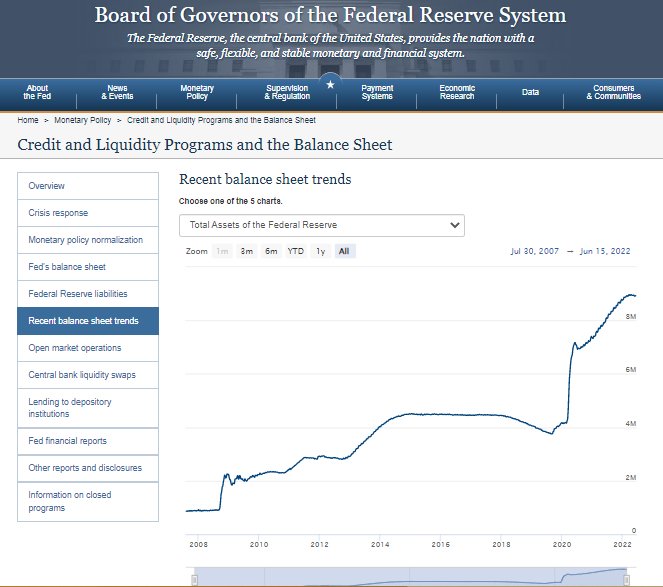

The foremost issue driving inflation is the enormous growth in the Fed balance sheet. We have simply produced far too much money, which has caused asset inflation in everything from real estate to equities to silly, one-of-a-kind, photos of monkeys (so-called “Non-Fungible Tokens,“ or ”NFTs").

Federal Reserve assets in millions of dollars. (Federal Reserve/Screenshot via The Epoch Times)

- In the fall of 2008, to maintain market liquidity with Quantitative Easing (QE) for the September 2008 Lehman Brothers collapse housing crisis (from $905 billion to $2.2 trillion);

- In December 2012, when the Fed gradually expanded its balance sheet in a slowing economy (from $2.9 trillion to $4.5 trillion);

- To address the CCP virus in 2020 and, again, to fulfill Biden administration fiscal policy, like the American Rescue Plan Act of 2021 that added $1.9 trillion, to an already recovering economy. All told, the Fed balance sheet went from just under a trillion dollars (from $4.2 in March 2020 to $7.2 trillion in June); then, again, to today as the Fed balance approaches $9 trillion.

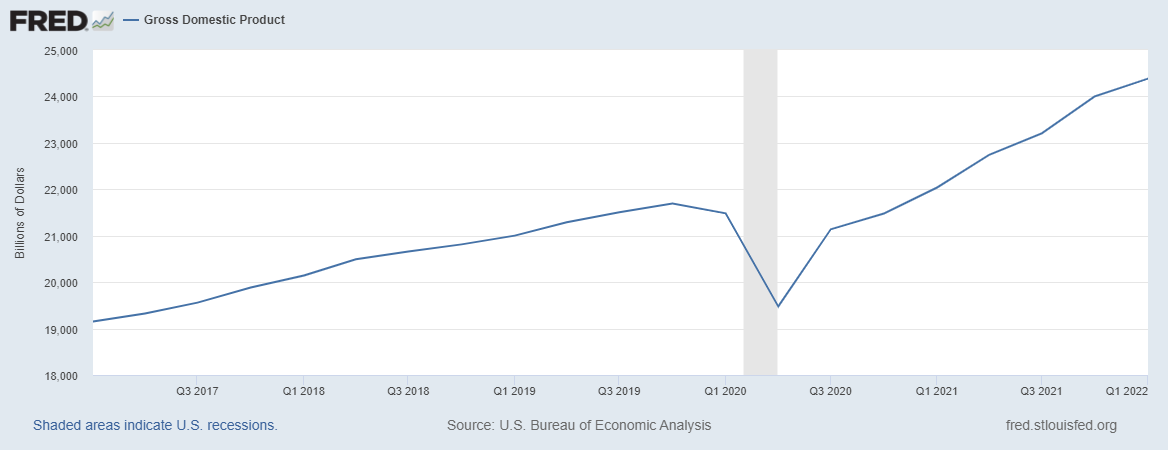

There’s Not Enough ‘Stuff’ in US Markets...

A glance at GDP shows the trajectory of GDP growth was considerably disrupted by the CCP virus. It is only now commencing a return to its pre-pandemic trajectory. Had GDP growth continued unabated, there would be more goods and services (the “Q” in the formula aforementioned) to “sop up” the excess money that’s in the system.

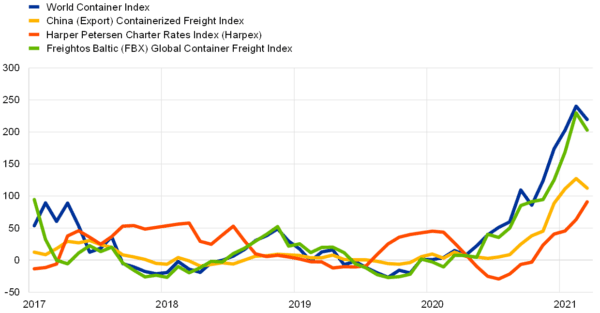

... and It Costs More to Get Stuff Here

As the European Central Bank (ECB) wrote in its March 2021 Economic Bulletin, costs for container ships had increased dramatically, even by the second half of 2021. “Reportedly, ports in Europe and the United States are congested amid logistics disruptions related to the coronavirus (COVID-19) pandemic and idle containers remain in several ports on the back of the uneven recovery of trade,” the ECB wrote.

‘Weaponizing’ the Dollar Over Ukraine Has Harmed Us

Foreign demand for US Dollars (USD) helps to retain its value relative to other currencies in our free-floating exchange system. “King Dollar,” meaning a strong USD relative to other currencies, and a frequent refrain of financial commentator Larry Kudlow, helps U.S. consumers buy goods, particularly imports, more cheaply.The Biden administration’s decision to attempt to “weaponize” the USD as part of its sanction campaign against Russia over Ukraine shook foreign central bankers’ confidence in the USD to some extent. A number of entities divested of dollar holdings, starting in March and accelerating in April, for fear that what the United States did to Russia’s reserves could happen to their reserves as well if they ran afoul of the United States. (See this chart from TradingEconomics.com based on Federal Reserve data for a graphic representation.)

The divestment reduced the demand for USD and, thereby, its purchasing power. It made things cost more. While we have imposed economic sanctions in prior conflicts, we have never before weaponized the USD to destroy another nation’s currency—not even against the Nazis.Lessons for Now and for Future Policy

Prospectively, we should recognize that there is a risk of expanding the Fed balance sheet and should keep it tied to GDP to make sure there is not “too much money chasing too few goods (and services).” I continue to maintain the Fed should sell off the Treasurys and MBS it acquired in the pandemic.Supply chains need to be made far more robust. Ideally, much of what we need (and particularly carbon-based fuels) should be sourced from the United States. But certain manufactured goods must come from overseas; making them here simply isn’t profitable. We should work with our North American trading partners to build out additional ports and port capacity along the Pacific Coast. On the Atlantic Coast, we should dredge ports to accommodate larger container ships. We should also have the Army Corps of Engineers perform a survey of the nation’s inland waterways with a view toward extending barge shipping along inland waterways. We should better integrate national rail lines with port operations to take the stress off the trucking industry. Truckers should be shipping the last few hundred miles, not coast-to-coast. And while we do that, let’s look at using GPS technology to maybe make trucking a “Pony Express” type of industry, with truckers driving a load outbound from their homes for four hours and then inbound for four, so that truckers can work as near as possible a regular work day and have dinner with their families. (Retiring “baby boomer” truckers have caused a shortage in the industry. Making the job less stressful and family-friendly might help add more workers.)

We’ve had experience dealing with inflation and we need to be extraordinarily wary of it. Biden’s oft-repeated cliche of, essentially, “I feel your pain,” does little for consumers deciding whether to choose to bypass their child’s dentist’s appointment or their car payment. Americans need solutions, not sympathy, from their government.

Future policymakers should be wiser in managing inflation than we have been the last several years. And take lessons from our shortcomings.