This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

NEW YORK (May 12)—April Consumer Price Index (CPI) inflation printed at an 8.3 percent, year-on-year, yesterday morning, down from 8.5 percent in March, but 2/100ths (or “20 bps”) higher than the market consensus estimate of 8.1 percent. Core inflation, which includes all items, less food and energy, came in at 6.2 percent, down from 6.5 percent in March, but also 20 bps above the consensus estimate. Market futures, which had been up before the release, did a “U-Turn” and moved lower, but then moved higher at the open. The 10 year spiked at 3.076 at the release, before moving sharply lower at around 9:00 a.m. as investors assessed the release more fully. (When rates go up, bond prices fall because bond prices have a negative correlation with rising rates.) Wednesday’s auction of the 10 year yielded 2.943 percent, the highest since 2018.

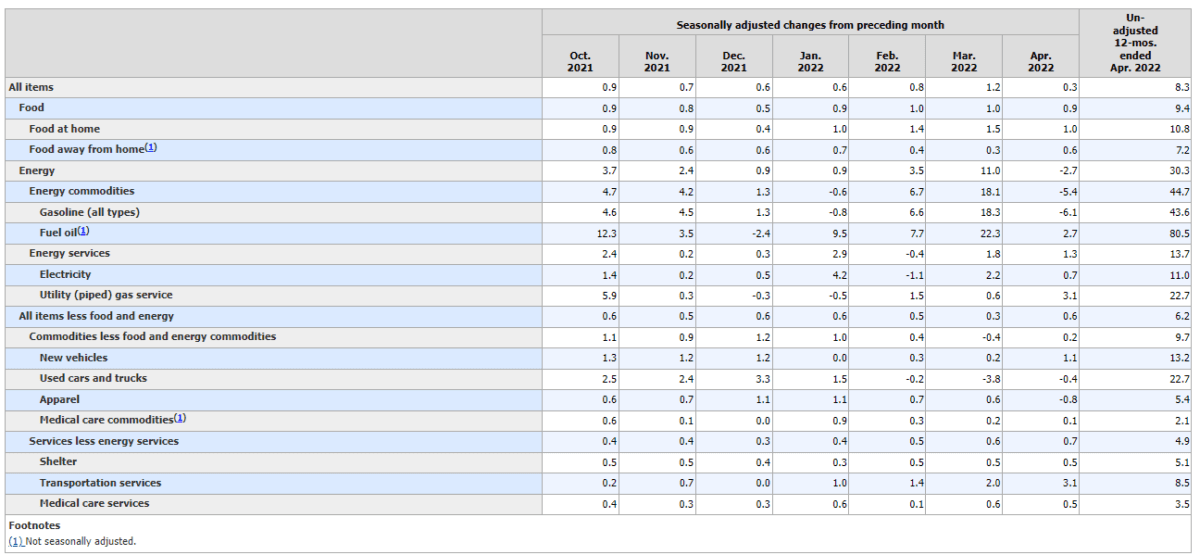

The granular data showed large annual increases in basic living expenses like food (10.8 percent for food at home) and fuel oil (80.5 percent). See the detail below.

Consumer Price Index Summary for April 2022. Bureau of Labor Statistics

This morning, the April Producer Price Index (PPI) printed at an annual rate of 11 percent, continuing the double-digit rate of annual increase it has maintained since December, led by increases in transportation services.

The increase in the PPI ultimately tends to work its way down to the CPI, so this is a harbinger of continuing high CPI inflation.

Commentary

A second print in a row of monthly CPI inflation above 8 percent should disabuse anyone of the notion that the current inflation is “transitory,” a notion the Federal Reserve and Biden administration had floated for most of last year. It is more than clear that, at best, inflation will plateau if not go higher.

Federal Reserve (“Fed”) monetary policy and Biden administration fiscal policy has—so far—been entirely inadequate to reduce inflationary trends. While the Fed raised the Federal Funds rate, the rate of interest the Fed charges member banks, to between 75 to 100 bps, the Fed balance sheet, which affects longer-term rates on things like mortgages, capital investment, and business planning, won’t see a significant reduction until at least June, when the Fed will start allowing the securities it acquired in the aftermath of the pandemic to “burn off” at maturity.

What’s needed—and as I’ve written here before nearly six months ago—is, instead, for the Fed to signal several months ahead that it will reduce the balance sheet aggressively, so that firms can reduce leverage and longer-term rates can be boosted by having the fed off-load the Treasurys and Mortgage Backed Securities (MBS) that it acquired at the start of the pandemic.

The simple fact is that low-interest rates have pumped up asset valuations far beyond what they are worth. That includes real estate, equities, commodities, and crypto currency. Now that the Fed is “withdrawing the punch bowl,” asset values—some of which have been pledged as collateral for borrowings—have declined. Consequently, the Fed has issued a warning—entirely appropriately—about the risks to market liquidity.

At this point, there are no good choices. The Fed can continue to accept aberrant ongoing inflation, gamble that supply chains and the Labor Participation Rate improve so that inflation subsides, or accept a recession.

Personally, I favor a deep, hard, short recession—akin to 2008, but without Fed bailouts. Let the chips fall where they may. Stepping in, again, as we did in 2008 and 2020, will only re-start the mayhem again. It needs to stop here, as hard as it may be.

DISCLOSURE: The views expressed, including the outcome of future events, are the opinions of The Stuyvesant Square Consultancy and its management only as of May 12, 2022, and will not be revised. Statements herein do not represent, and should not be considered to be, investment advice. You should not use this article for that purpose. This article includes forward-looking statements as to future events that may or may not develop as the writer opines. Before making any investment decision you should consult your own investment, business, legal, tax, and financial advisers. The writer is Managing Director of the Stuyvesant Square Consultancy which associates with principals of TechnoMetrica on survey work in some elements of our business.

J.G. Collins is managing director of the Stuyvesant Square Consultancy, a strategic advisory, market survey, and consulting firm in New York. His writings on economics, trade, politics, and public policy have appeared in Forbes, the New York Post, Crain’s New York Business, The Hill, The American Conservative, and other publications.