With inflation at 40-year highs, the Federal Reserve has indicated it’s going to start raising rates by next month.

This is already leading to an increase in mortgage rates which in turn, will affect home prices. While every family and house has individual circumstances, the typical home-buying process involves a 20 percent down payment and a mortgage payment that is tied to monthly income. Coming higher interest rates are already leading to higher mortgage rates which means higher monthly payments for new homeowners.

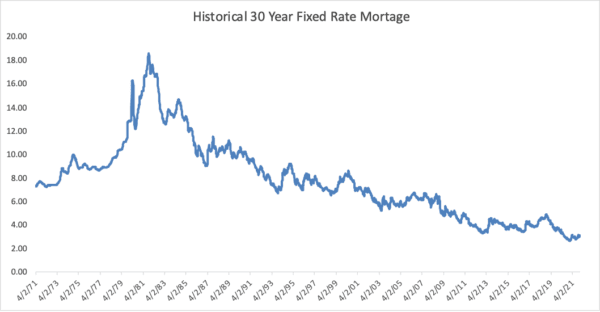

Mortgage rates are still historically low and could rise considerably.

We can see that mortgage rates have been coming down fairly consistently for the last 40 years, and only recently began to tick up slightly. Current rates are around 3.625 percent for a smaller mortgage and 3.750 percent for a jumbo mortgage. Right now, expectations for rate hikes in 2022 are around 1.50 percent.

If mortgage rates go up that much over the next year, home prices would need to be 16 percent lower in order for new homeowners to keep the same mortgage payment.

So, if there are no other changes in the real estate market, and the Federal Reserve raises interest rates six times this year, home prices would have to adjust by 16 percent in order to retain the same level of affordability. While it’s possible that the continued migration out of large cities and to the suburbs could lead to continued increases in real estate prices, rate increases are creating a very large headwind. The last two years aside, home prices don’t typically rise by double-digit percentages in one year.

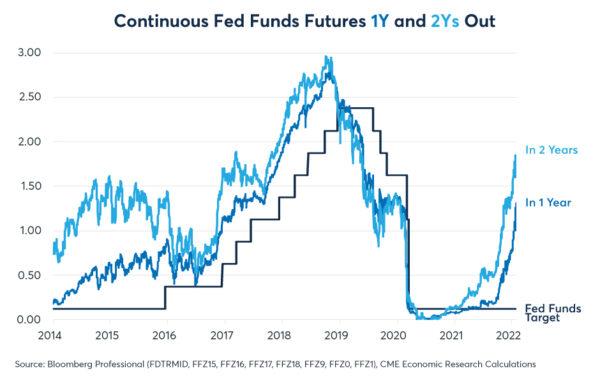

The better question is: what happens if expectations for interest rate hikes are too low? If we go back just a few months, we can see that expectations were for no rate hikes in 2022. Then, when Federal Reserve Chairman, Powell said he would raise rates in March, the market thought we were going to see three hikes of about 25 basis points (.25 percent) each. Now, many market observers are expecting five to seven increases.

As expectations adjust to historically high inflation numbers, it means our 1.50 percent increase in mortgage rates may be conservative.

If mortgage rates rise by two percent, home prices would need to fall by over 20 percent to keep monthly payments the same. That would take mortgages to a little over 5.5 percent which, as seen by the first chart, is still low by historical standards.

We’ve read commentary by smart people suggesting that home buyers rush to buy now in order to lock in a lower mortgage rate. Our counsel is the opposite. If you’re considering selling, move quickly because once interest rates rise, and mortgages become less affordable, the only way the buyer can afford your home is to lower the offering price.

One final way to view the situation is from the position of a homeowner who doesn’t want to move. If current mortgage rates are below the rate you’re paying now, this would be a good time to consider refinancing quickly. The thing we like about owning real estate right now (besides having a place to live) is that it’s easy to borrow money against it for three decades. If the current inflation rate is 7.5 percent (and we think it’s higher), then you’re paying your future mortgage payments with dollars that have declined in value. As long as the inflation rate is above the mortgage rate, the dollars you use to repay the bank will decline in value by more than the extra dollars you need to pay the interest on the loan.

There are many factors that affect what someone is willing to pay for a home. While we can’t tell you the future of the housing market, we are confident that higher rates will be a headwind on value, and inflation will be a benefit to those who have mortgages.