Federal Reserve Governor Michelle Bowman said Monday that national economic tailwinds and supportive monetary policies would give local economies a lift.

“My outlook for the U.S. economy is for continued growth at a moderate pace, with the unemployment rate—which is the lowest it has been in 50 years—remaining low,” she said at the event. “I also see inflation gradually rising to the [Federal Open Market] Committee’s 2 percent objective.”

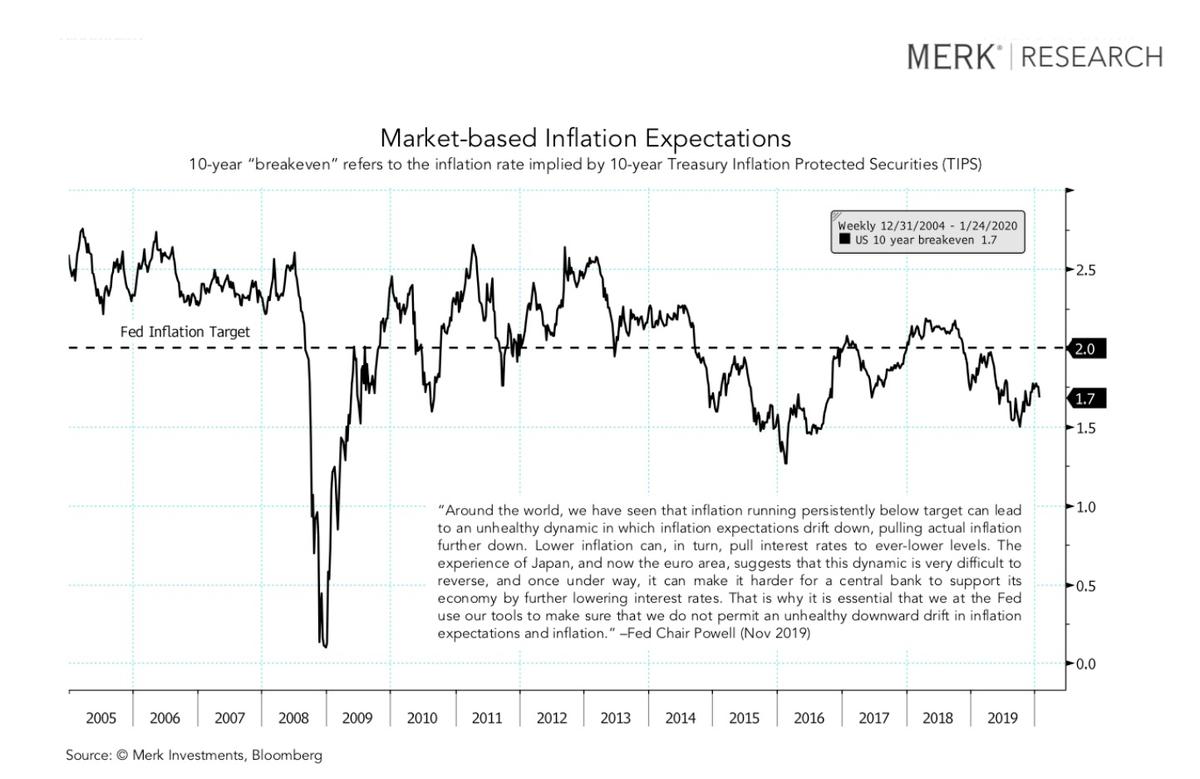

At recent meetings of the Federal Open Market Committee (FOMC), the central bank’s interest rate setting body, officials expressed concern about inflation running too cool.

One of the market-based inflation expectations measures the Fed considers in setting policy shows that markets believe average inflation over the next 10 years will hover around 1.7 percent.

Bowman’s remarks come after the FOMC’s most recent meeting, when the committee decided to keep the benchmark rate unchanged at a target of between 1.50 and 1.75 percent.

In justifying its decision to keep rates steady, the FOMC cited labor market strength, in particular solid job gains and low unemployment, as well as an economy that “has been rising at a moderate rate.”

In her speech in Florida on Monday, Bowman emphasized that the Fed’s “policy setting should help support the economic expansion, which is now in its 11th year.”

‘Lifeblood of their Communities’

In her remarks, Bowman said that by ensuring businesses and individuals enjoy reliable access to financial services, small banks served as “the lifeblood of their communities.”“By extending credit and offering specialized products and services that meet the needs of their borrowers, these banks empower communities to thrive,” she said, praising community banks for superior asset quality compared to larger institutions.

“The community bank net charge-off rate for total loans and leases was less than 0.2 percent at the end of the third quarter 2019,” she added. “Let me state that again—the net charge-off rate was less than 0.2 percent, less than half of the industry average.”

She encouraged small banks to embrace innovation going forward, while noting the challenges of rapid technological adoption.

“As I noted earlier, banks with less than $500 million in assets employ roughly 40 people on average—nowhere near the number required to exhaustively develop, test, and manage every element of novel technologies,” she said. “In my discussions with bankers, they note that the process of selecting, initially vetting, and continuing to evaluate third-party service providers is onerous and presents obstacles to successful innovation.”

Bowman said regulators and supervisors should help smaller institutions by tailoring their approach to the risk profiles and resources of community banks.

“I agree that the cost of complying with some of our regulations and expectations for third-party relationships can pose an outsized and undue burden on smaller banks,” she said.

“I believe regulators and supervisors have a role to play in ensuring that the burden is tailored to bank size, risk, complexity, and capacity,” she said.

“We should be mindful that when we apply the same expectations to banks with starkly different asset sizes, we are creating the same workload for a bank with about 30 employees as for a bank with roughly 180 employees, even though their resources and risk profiles are quite different,” she explained.

There are over 4,800 community banks in the United States, each with around 40 full- and part-time employees, on average.