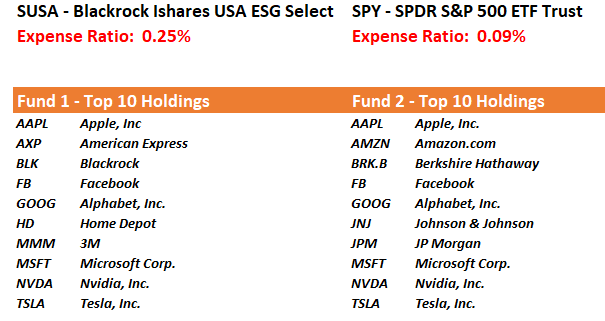

With ESG now all the rage, the “demand” drives product development. However, there is also an understanding of why large asset managers have embraced the strategy so readily—higher fees.

Yes, you too can own an ESG fund that is almost three times as expensive as the S&P 500 index, all for the sake of “feeling good about yourself.”

Been There, Done That

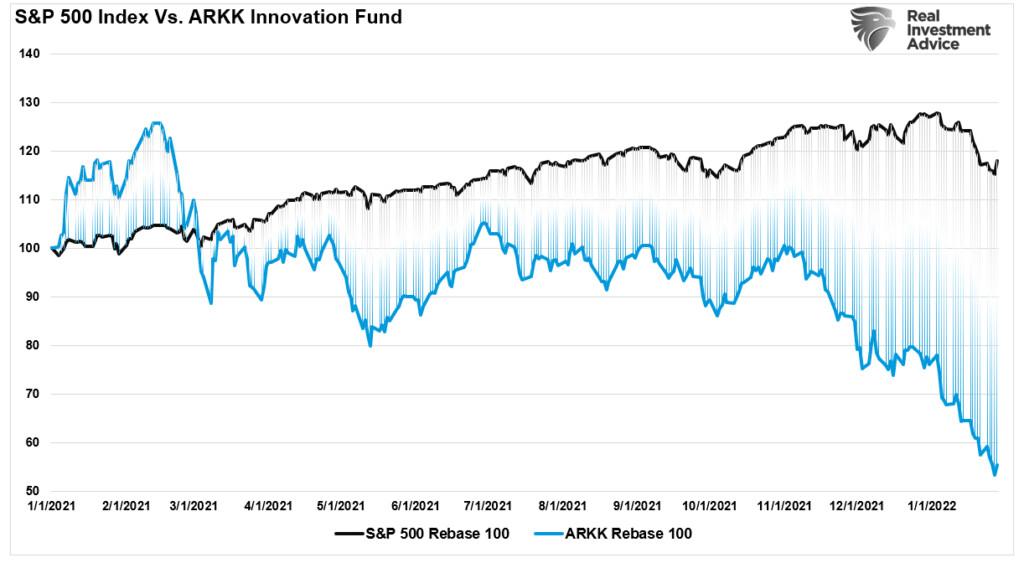

In the late 1990s, there was a significant movement by Wall Street to limit investing in “sin” stocks such as gambling, tobacco, etc. Investors initially jumped on board, but when returns failed to match the S&P index, that “fad” died away.The same occurs today as investors who want to be “woke” are demanding products that make them feel good to purchase. However, just as we have witnessed with the various ARKK ETFs, while you may “feel good” about owning “disruptive” companies, that changes quickly when those companies are no longer performing.

Such is inherently an issue facing ESG funds. Investors will be willing to pay higher expense ratios as long as they are earning higher returns. However, despite the best of intentions, individuals are subject to emotional biases and ultimately focus on performance.

The performance issue will likely become more prevalent as funds that were already underperforming and losing assets simply rebrand themselves.

None changed their stock or bond holdings at that point.”

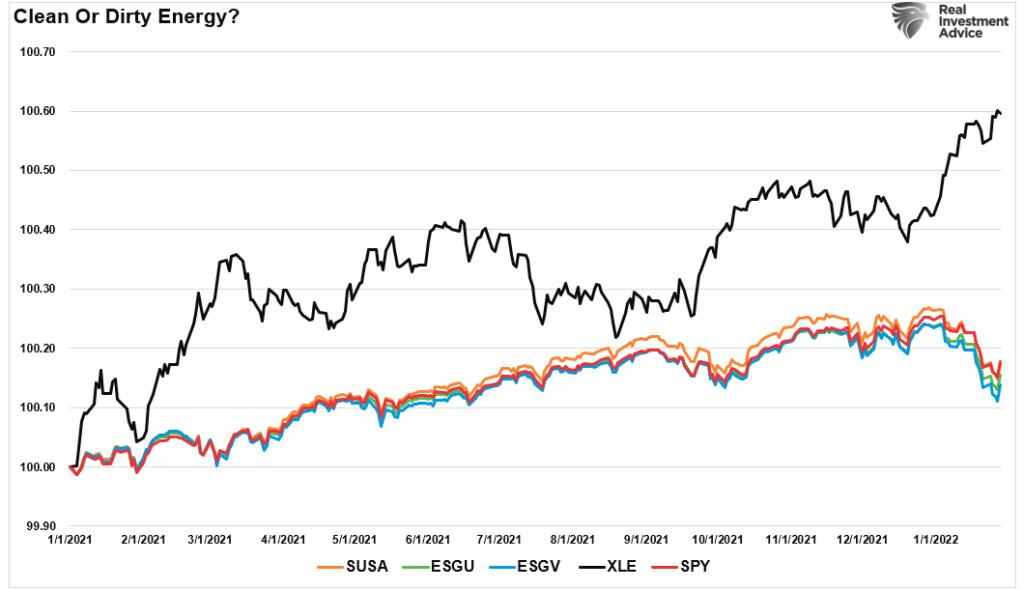

Inflation Could Kill ESG

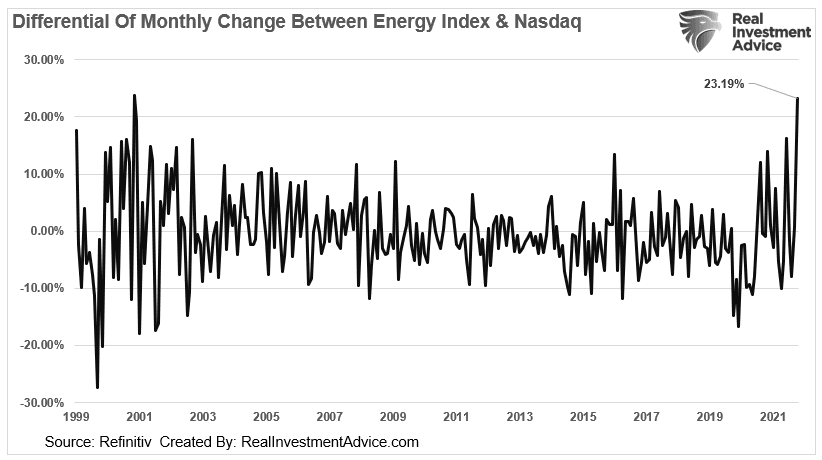

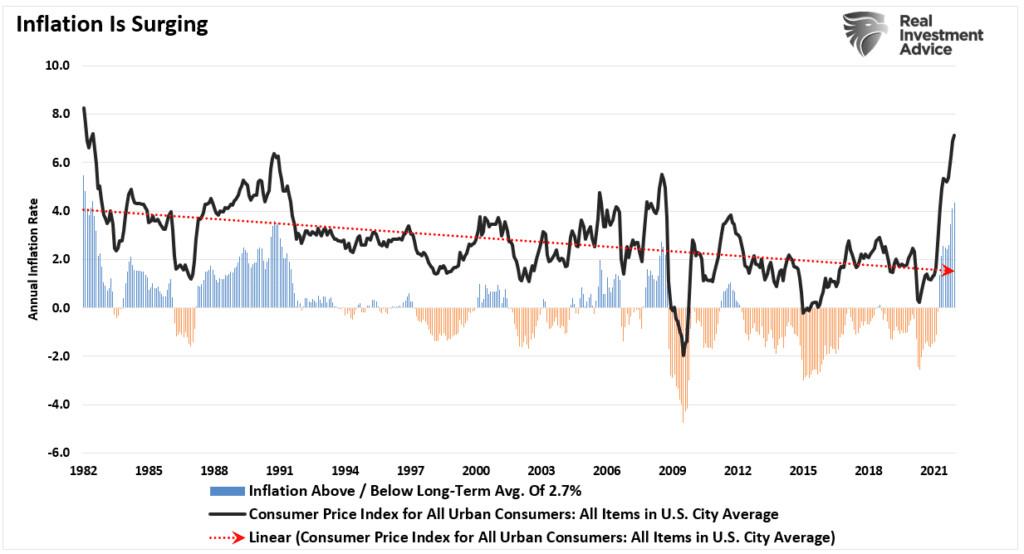

If you believe that inflation is here to stay, then ESG will grossly underperform. While 2022 has been a year of “inflation” concerns by the Fed, the underperformance of ESG relative to the energy sector has been quite profound.“As Deutsche Bank’s Jim Reid puts it, ‘one of the side effects of the hawkish pivot from the Fed in 2022, that continued this week’ is that it could finally crack the facade of ESG and make January a catastrophic month for ESG investors; this is shown in Reid’s Chart of the Day which lays out the 1-month rolling difference between S&P 500 Energy sector returns and the NASDAQ,” ZeroHedge reported last month.

Not surprisingly, that inflationary surge showed up at the gasoline pump as oil prices shot up. As a consequence, and of no real surprise, investors dumped ESG funds in favor of “dirty energy.”

As shown, the SPDR Energy Sector ETF (XLE) has vastly outperformed not only the S&P 500 index, but some of the leading ESG funds from BlackRock, Vanguard, and IShares. Which would you have rather owned?

Want to Be ESG, Plant a Tree

Here is another problem with ESG investing—it makes NO difference to the environment.Think about how mutual fund investing works for a moment.

An investor buys shares of a mutual fund. The fund manager, in turn, purchases shares of the underlying investments from the open market. The underlying companies receive no capital from the transaction, nor are they aware a transaction occurred.

In this scenario, how were carbon emissions reduced? Were trees planted? Did companies take a different direction with their management teams? Of course, not.

“ESG frameworks are entirely superfluous. Simply follow the profits to find those companies enhancing humanity the most. Profits reflect the moral evaluations of billions of customers around the world voting with their hard-earned money. The good financial performance sought by investors can only result from strong value creation.”

“ESG designations are also counterproductive,” Levine adds. “The freer the market the more purely profits indicate ethically good companies. Deferring to a handful of groups, committees, and organizations is not only inefficient but narrow-minded and potentially morally corrupt. It creates a system ripe for gaming by the biggest, the most connected, and those with the most resources to spare.”

Ultimately, investors always seek out investment performance over time, As such, ESG investing will either evolve or give way to a new breed of “sin stocks.”

I suspect that Wall Street will win whichever way it eventually turns out.