Two months later, the crisis began.

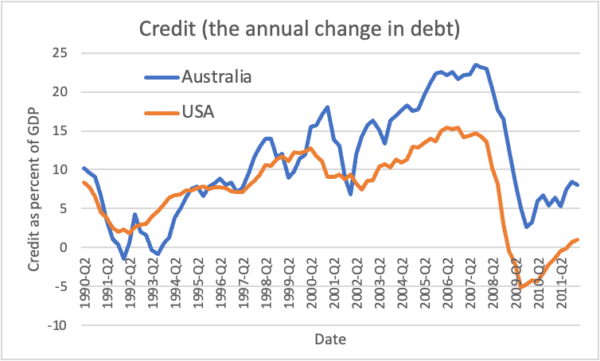

I’m one of a handful of economists to claim to have seen “It” coming, because, unlike the mainstream, I worry about private sector debt. In 2007, the level of debt was too high, and its rate of growth was also too high. I expected that a recession would occur when the rate of growth of debt dropped significantly—and especially if it turned negative.

You might think that mainstream economists would welcome alternatives that got right what they got so spectacularly wrong—in which case, you would also be spectacularly wrong! The universal reaction of mainstream economists to the claims of “heterodox economists” to have seen the crisis coming was to disparage and belittle their intellectual rivals.

It is often said of academic conflicts that the disputes are so acrimonious because the stakes are so small—a “storm in a teacup.” But this storm is over whether it is possible to predict economic tsunamis in the real world. So, the question of whether or not a crisis can be predicted—and, with better economic policy, prevented—matters a great deal.

At some point the ratio of debt to GDP must at least stabilise, and that when it does, the economy will go into recession—unless a substantial external stimulus counteracts the depressing impact of a debt correction.

At their public hearing, which coincidentally was held on the very day that the crisis began (Aug. 10, 2007, New York time, when the BNP shut down three funds based on the U.S. Subprime Housing Market), the inquiry asked the Reserve Bank of Australia to comment on my argument:

6.18 These conclusions were rejected by the RBA during the roundtable…

6.19 Chris Aylmer of the RBA … stated: “A slowdown in credit growth does not necessarily lead to a marked slowing in consumption and an economic downturn.”

Australia prevented a recession, as I said that it could, via a “substantial external stimulus.” Australia’s chief economic bureaucrat advised the government to “go hard, go early, go households,” and that’s precisely what it did.

It gave every taxpayer an AU$1,000 tax rebate, to encourage immediate spending. It undertook numerous spending programs of its own—including insulating houses for free, and building school meeting halls across the country. Most effectively of all, it restarted Australia’s housing bubble, by giving first home buyers grants of up to AU$34,000. This easily covered as much as 10 to 15 percent of the purchase price of a new house.

So yes, I predicted the crisis, and yes, I explained how Australia could avoid it as well—though the policies Australia’s government followed had the side effect of giving Australia the second-highest level of household debt in the world today.

But that’s just the “storm in the teacup.” The important point is that economic tsunamis like the GFC can be avoided, by controlling how much credit banks create.

We’re not likely to do this, unfortunately, because, despite their failure to see the crisis coming, conventional economic thinkers—like Peter Bofinger, and the Reserve Bank of Australia economist who assured the committee that a slowdown in credit wouldn’t have a significant impact on the economy—still dominate how politicians think about the economy. They refuse to learn the lesson of history, that credit matters. And while they continue to do so, we’ll continue running into economic crises that “no-one saw coming.”