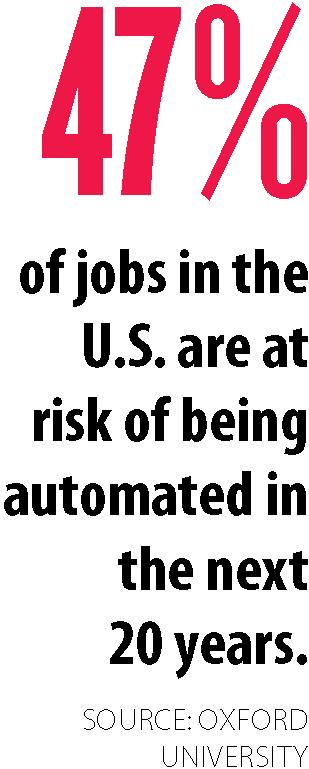

Despite the temporary injection of confidence in the American economy brought about by the election of President Donald Trump, major structural problems continue to lurk beneath the surface. These trends, decades in the making, are so entrenched and intractable that even Trump’s boldest plans may not be able to resolve them.

*