Since last Wednesday—when the Federal Reserve rate decision dropped at 2:00 p.m. EST—to the market close on Friday, the Dow Jones Industrial Average slipped 4.2 percent and the S&P 500 Index fell 4.9 percent. While most business columnists put those declines mostly on the Fed’s rate increase, a deeper dive speaks to a more negative outlook for the economy.

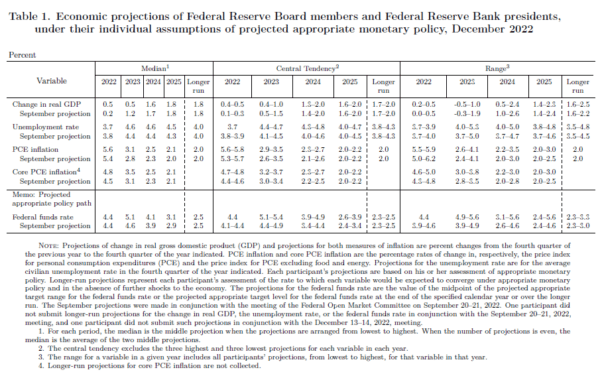

The FOMC also expects a generally higher unemployment rate as the economy slows. While the central tendency tops out at 4.8 percent, the range of estimates goes up as high as 5.3 percent.

Also higher are estimates of inflation, with the central tendency ranging as high as high as 5.8 percent this year and arguably sanguine estimates that it will decline to 2 percent by 2025.

Finally, the federal funds rate is targeted to go as high as 5.4 percent under the central tendency in 2024, but with a range as high as 5.6 percent. (That would easily equate to a mortgage rates as high as 8–9 percent!)

“That’s just ... changing our inflation goal is just something we’re not ... we’re not thinking about, and it’s something we’re not going to think about. It’s ... we have a 2 percent inflation goal, and we'll use our tools to get inflation back to 2 percent. I think this isn’t the time to be thinking about that. I mean, there may be a longer run project at some point [emphasis added]. But that is not where we are at all. The Committee, we’re not considering that. We’re not going to consider that under any circumstances. We’re going to ... we’re going to keep our inflation target at 2 percent. We’re going to use our tools to get inflation back to 2 percent.”Let’s hope so.

Continuing Inflation, Increasing Rates

Most of the inflation we’re seeing now is services inflation. Goods inflation is falling with supply chains being largely restored. And while there have been a lot of high-profile layoffs, many of those are by tech firms and among holders of non-immigrant H-1B visas. Those workers’ layoffs do not enter into the unemployment rate because they are no longer considered part of the workforce after 60 days of being laid off. So, with a relatively strong labor market, and a social safety net that has become, for some, a hammock (the 1996 work requirements to receive income support were eviscerated under President Barack Obama), we can anticipate continuing higher wages to get workers, higher services inflation, and low unemployment.Summary

Fiscal policy and monetary policy are working at cross-purposes. As the Fed tightens—and will likely continue to do so—Congress and President Joe Biden are set upon spending more.The result will be stagflation.