News Analysis

International wealth-management firms recently received a fast introduction to how Beijing conducts business, when a UBS banker on a business trip to China was barred by authorities from leaving the country.

The Singapore-based UBS private-client banker was held in Beijing and was required to answer questions from authorities. UBS temporarily asked its employees to delay traveling to China during the ordeal, which lasted a total of 24 hours.

The event alarmed other international banks. Banks including BNP Paribas, JPMorgan Chase, and Julius Baer asked their staffers to reconsider traveling to China in the immediate hours after the UBS employee was held, according to Reuters.

This type of questioning has become business as usual for Asia’s biggest economy. In 2012, a banker from UK-based Standard Chartered was detained and questioned as part of an anti-corruption investigation into one of the bank’s clients.

UBS didn’t disclose the nature of the questioning, but CEO Sergio Ermotti told reporters during the firm’s quarterly earnings call that the inquiries had nothing to do with the bank or the employee. He reiterated that the firm has a strong franchise in China.

A New Frontier for Private Banking

UBS has the biggest wealth-management operation in Asia, with around $383 billion in assets under management, according to Asian Private Banker.The Swiss bank is one of a few international banks with an onshore presence in mainland China, whereas several competitors have set up offshore operations in Hong Kong to service Chinese clients.

UBS has become one of the most aggressive Western banks in scaling its operations in China, after Beijing authorities lifted restrictions placed on the banking sector earlier this year. Foreign firms are now permitted to own a 51 percent stake in an onshore investment firm, and within two years, foreign banks will be allowed to wholly own Chinese subsidiaries.

In early October, UBS took steps to become the first foreign bank to own a majority stake under the new rules after two partners put their stakes up for sale, according to Reuters. The deal hasn’t yet been approved.

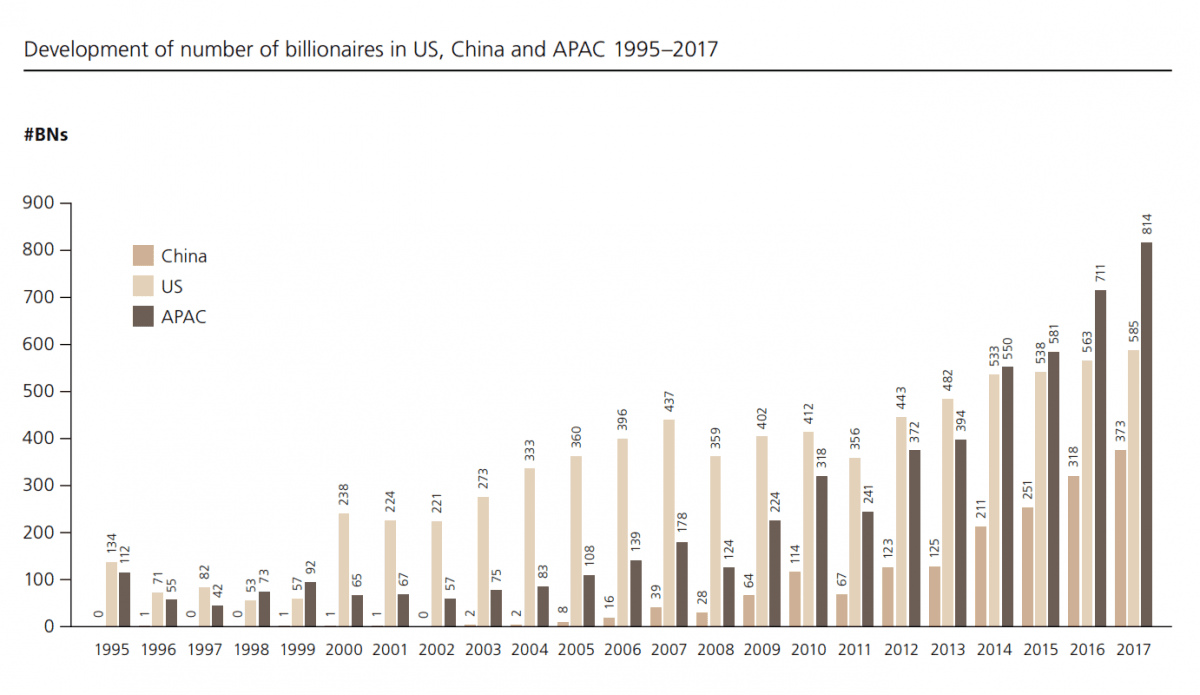

It’s not surprising that UBS, which has the biggest wealth-management business among global banks, wants to take share in China. The 2018 edition of the annual “Billionaires Insights” report released by UBS and consulting firm PwC found that the 332 billionaires were created last year, with China leading the way.

“There were 373 Chinese billionaires at the end of 2017, and 97% of them were self-made,” the report said. “This phenomenon has happened in little more than 10 years—as recently as 2006, there were just 16 Chinese billionaires.” According to the report, growth is largely driven by an entrepreneurial hub around the southern city of Shenzhen, which has been challenging Silicon Valley in value creation within the technology sector.

Courtesy of UBS / PwC

Increasing Scrutiny

But as international banks prepare to expand their presence in China, they must also be prepared to potentially compromise existing business policies, and hand over client information to the Chinese communist regime.The industry will face scrutiny from Beijing authorities who closely monitor the country’s wealthy and their financial transactions for potential transgressions, including capital flight, regulatory wrongdoings, or other activities deemed by the regime as illicit behavior or corruption.

China’s wealthy have looked to diversify their assets abroad in recent years as the domestic property market cools. Chinese authorities, on the other hand, fearing further weakening of the yuan currency, have placed restrictions on capital leaving the country. In some cases, wealthy elites have resorted to loopholes such as funneling cash to Macau or Hong Kong, or using bitcoin to transfer assets abroad.

Certain economic transgressions appear to stem from politics. Last year, billionaire Chinese businessman Xiao Jianhua was abducted in Hong Kong by Chinese agents and hasn’t been seen in public since. Xiao is believed to be a financial conduit of certain political opponents of regime leader Xi Jinping.

And Western bankers and business leaders—who advise and serve such wealthy Chinese clients—could increasingly find themselves in the crossfire.

“Last time I was in China, I was forced to turn in my iPhone prior to a meeting. I suspect that tracking or listening apps may have been installed onto it,” a partner at a U.S.-based investment firm told The Epoch Times, asking not to be named.

“Now, I make sure to carry a ‘dumb’ phone when I go over there.”