Since the second half of 2021, the economic and finance world has been focused on inflation numbers that are both high and increasing. This is the first in a series where we’ll focus on what higher inflation means to you, how and why it’s being mismeasured, and what steps you can take to protect your portfolio in a high-inflation environment.

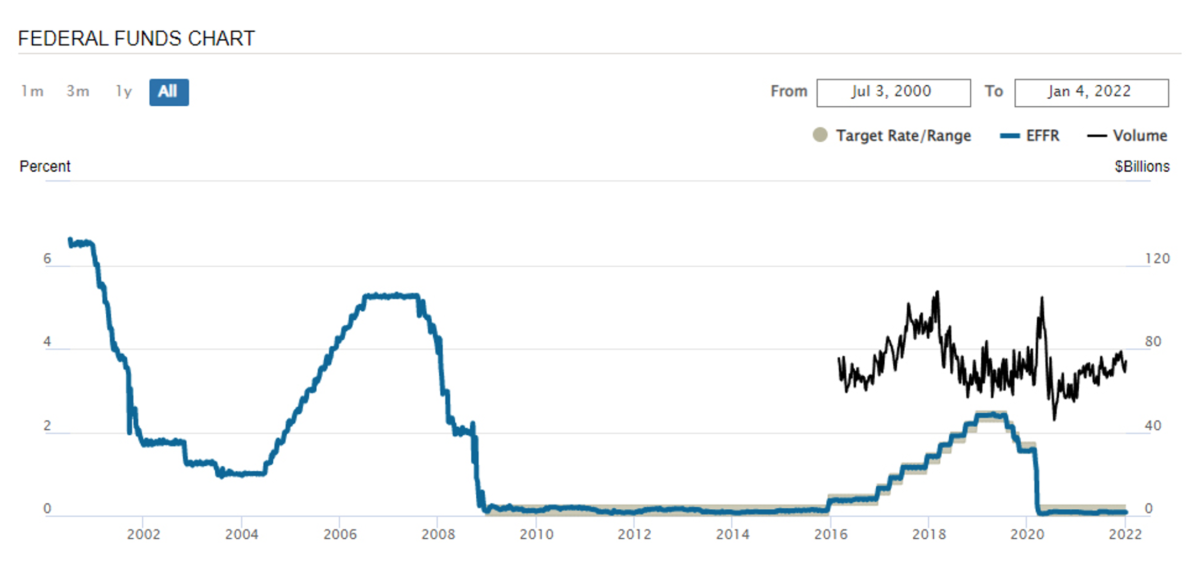

A common definition of inflation states that it’s what happens when too much money is chasing too few goods. The Federal Reserve (“the Fed”) has been pursuing two policies that have caused inflation.

The second policy is called quantitative easing. The Fed increases the money supply by creating dollars in its account and then using those newly-created dollars to buy government bonds or other assets.

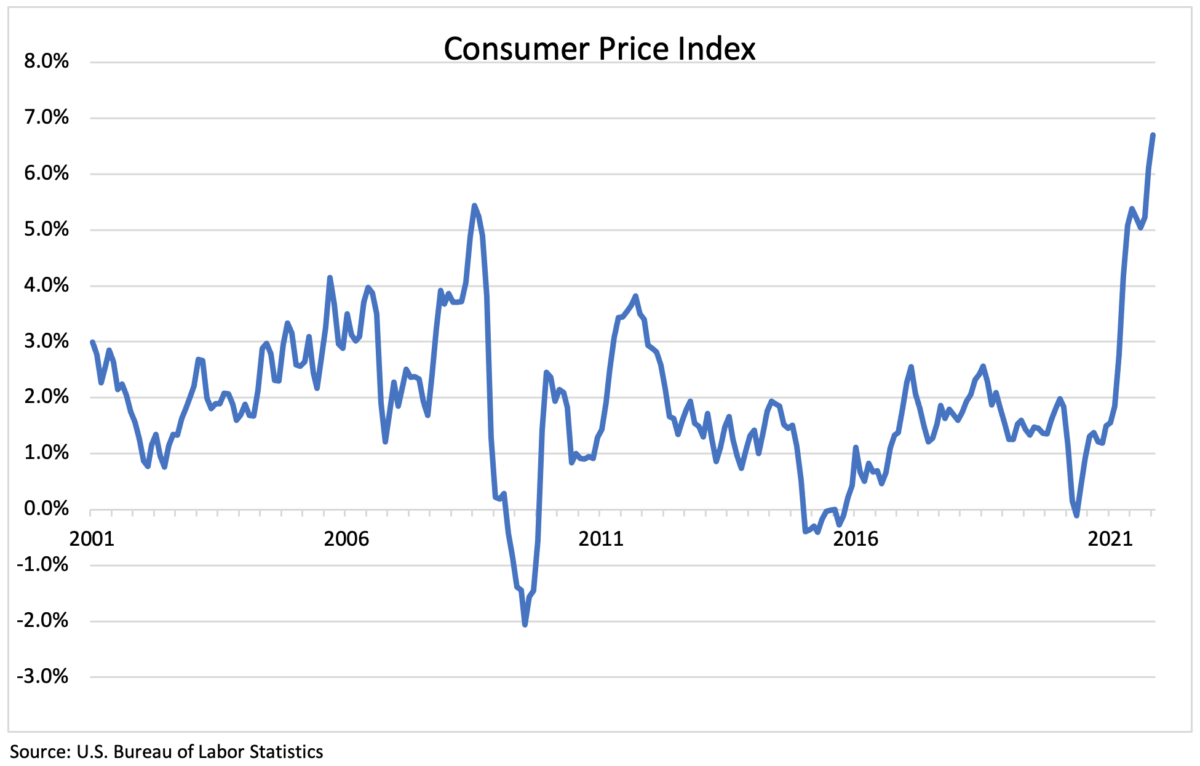

It’s clear that there’s now a lot more money chasing goods and services. That, combined with widely-reported supply chain issues and a huge labor shortage, has led to a massive increase in prices. That’s typically measured by the Consumer Price Index (CPI) which is intended to be an attempt to measure an overall change in prices across time.

Besides the fact that not everyone spends money on the same items, as a measuring metric, the CPI suffers from deliberate attempts to understate the level of inflation. We’ll cover that more in next week’s article. For now, here’s what the U.S. Bureau of Labor Statics shows as the official inflation rate.

Looking at the chart, it’s easy to see why we’re tying Federal Reserve policy to the increases in prices you’re seeing in your daily life. Because consumer prices can rise in real-time, but salary increases tend to come once a year, it’s easy for increases in the cost of living to outstrip after-tax wages. This is particularly true for any of you looking at large purchases.

According to the Case-Schiller U.S. National Home Price Index, the cost of the average home has increased by about 30 percent over the past year and a half. Looking at the Manheim Used Vehicle Value Index shows used car prices have almost doubled in the same time period[4]. New car prices have also risen if you can find the model you want.

Let’s take the example of a couple earning $100,000 a year. Depending on the state they live in, they’re probably paying around a 30 percent tax rate leaving them with disposable income of about $70,000. Let’s assume this couple is prudent, and lives on $60,000 and invests the other $10,000. If they experience the current CPI inflation of 6.7 percent, that reduces their buying power by $4,000 a year and cuts their yearly savings/investing by 40 percent.

Assuming you’re dealing with housing costs (up 20 percent–30 percent), buying a new or used car (up almost 100 percent), or dealing with much higher energy costs, and our once prudent couple now has the choice of dipping into their savings to maintain their current standard of living, or to start making cuts to their lifestyle. This is where dry economic statistics from the Federal Reserve press releases or the U.S. Bureau of Labor Statistics start to affect people’s home life.

To make matters worse, the Federal Reserve is reacting to rising inflation by ending the quantitative easing that is flooding the market with cash, and by raising interest rates. That typically has a negative effect on stocks in general, and high-growth stocks in particular. Those high-growth stocks are the ones that many investors have been riding to high returns over the past few years. This is also true if you own indexes like the S&P 500 or the NASDAQ 100.

So, not only does our careful couple lose the ability to save and may have a reduced quality of life, it’s likely that their stock market returns on money they have invested are going to be lower or negative in a rising interest rate environment.

In the coming weeks, we’ll cover why we think the official inflation number is under-stated, why we think the Federal Reserve isn’t doing enough to fix the problem, and most importantly, the things you can do in your portfolio to reduce your risk. And for those of you who are interested in why bonds and high-growth stocks decline when the Fed raises rates, let us know in the comments, and they could be the subject of future columns.