Commentary

During a webinar last week on Ukraine, Russia, and U.S. Foreign Policy, a couple of expressed opinions drew a lot of attention. The first was that the conflict in Ukraine is likely to last somewhere between a couple of months and several years. The second was that western sanctions on Russia would have been more effective had they been applied prior to the start of the war. At this point, Vladimir Putin is committed to his course of action, and sanctions are unlikely to get him to back down now. This means that the United States is likely to be living with the effect of sanctions for an extended period, and the costs won’t be borne exclusively by Russia.

Oil Prices

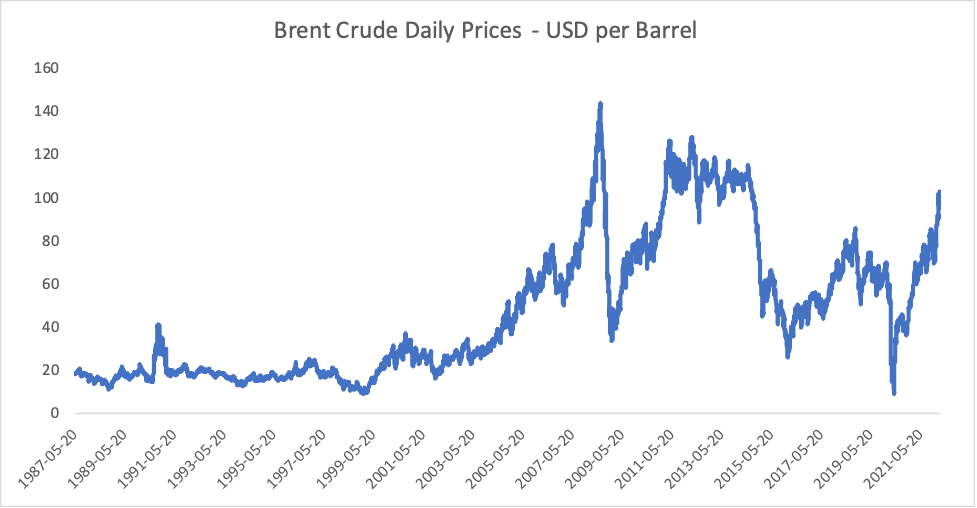

We spoke with Siddharth Singhai, the Chief Investment Officer at Ironhold Capital, a firm that specializes in global value investing. He points out that Russia was the third largest oil producer in the world, accounting for 12 percent of global production. Pipelines to Germany are being shut down and failing financially. Some Russian pipelines run through Ukraine. Many shippers are refusing any Russian cargo including oil for fear that international sanctions, port regulations, or insurance provisions could change while in transit. While oil is a commodity, it is difficult to restructure distribution of that much product in any reasonable time-frame. With Russian production of 11 million barrels a day, the recent release of 60 million barrels from emergency stockpiles is nothing more than a gesture. Oil prices have already skyrocketed and are approaching all-time highs. Investors realize that much of the Russian oil supply may be stranded.

A graph showing the price of Brent Crude including the recent spike in prices. Source: Federal Reserve Bank of St. Louis, Graph by Deep Knowledge Investing Intern, Guru Sidaarth

Food Prices

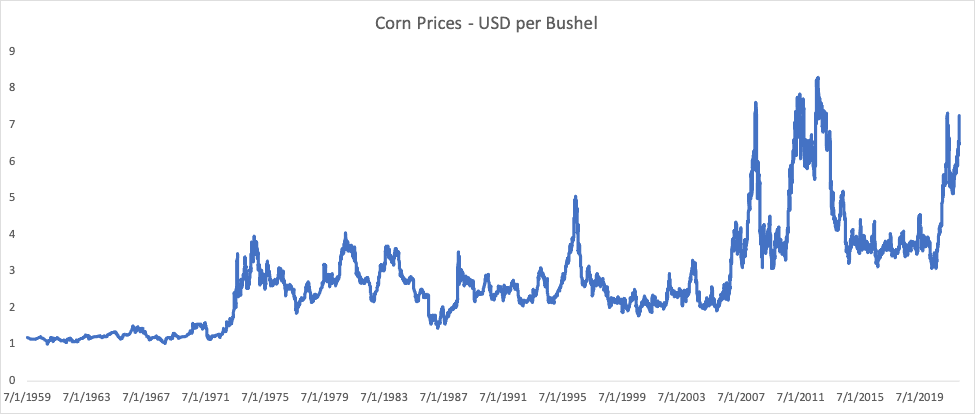

The coming increase in food prices could be worse than what we’re seeing in the energy sector. Mr. Singhai notes that Ukraine is the 4th largest exporter of corn at 15 percent of global trade, and Russia is 6th at a little over 2 percent. Many Ukrainian farmers have fled the country, and others are defending their nation. Either way, it’s likely that the spring planting season will be disrupted, affecting food prices all over the world. It’s very difficult to eliminate corn from your diet as it’s used extensively in cooking oil, sweeteners, and as feed for animals.

A graph showing that the price of corn is nearing all-time highs. Source: www.macrotrends.net, Graph by Deep Knowledge Investing

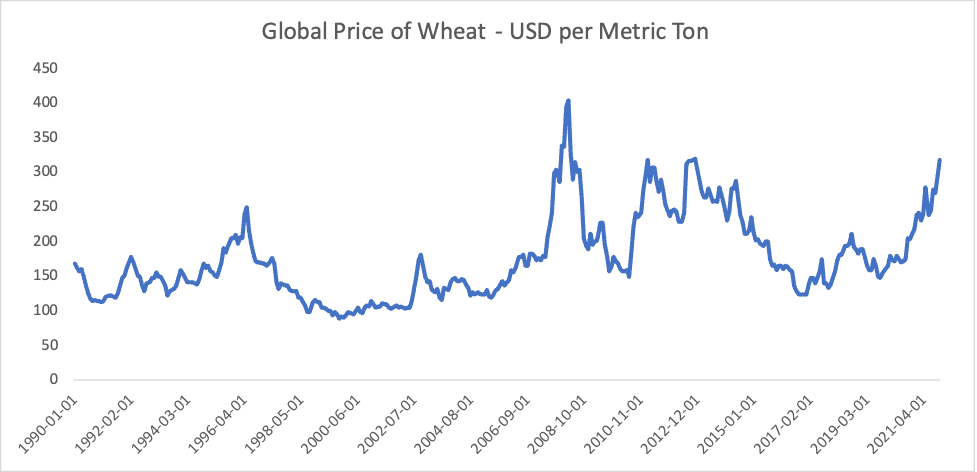

In addition to corn, Ukraine is also a large producer of wheat. Like corn and oil, wheat prices are nearing all-time highs, making it expensive to use as a substitute for corn, and further increasing inflationary pressure for food worldwide. Higher prices for corn and wheat will also add to the price of meat as those commodities make up much of the food supply for livestock.

A graph showing that the price of wheat is nearing all-time highs. Source: Federal Reserve Bank of St. Louis, Graph by Deep Knowledge Investing

Further complicating matters is the fact that Russia produces huge amounts of fertilizer and is now refusing to sell to the United States. As of this writing, there is talk that Russian fertilizer producers may make the decision to decline to export any product. Without sufficient fertilizer supplies, U.S. producers of corn, wheat, soybeans, and other food commodities will be less efficient and produce smaller crops. In addition, fertilizer production requires oil so any new additions to capacity are going to have a higher cost basis than Russian fertilizer did a year ago.

The Federal Reserve and Interest Rates

At a minimum, Americans are about to see higher energy and food prices, and this leaves Federal Reserve Chairman Jerome Powell in a terrible position. As we’ve covered in a prior column, official inflation statistics are at multi-decade highs, and real interest rates are at all-time lows. The Fed need to raise rates now to head off an inflation problem that’s affecting the standard of living for many U.S. citizens. Within the last week, Powell has expressed both caution about raising rates too quickly due to fears that war will hurt the economy, and also admitted that the Fed should have started raising rates sooner. It seems he agrees with us that we are in a position that can’t be solved without imposing some pain on the country.US Foreign Policy and Domestic Communication

Our wish for the Ukrainian people is for peace, prosperity, and self-determination. Ukrainians should be free to chart their own course free from outside influence and force. We accept that in order to support that goal, it’s going to add to the cost of living here in the United States, and to that end, we wish the White House would be honest with the country about what those costs are. The State of the Union speech on March 1 not only didn’t disclose the costs that would be borne by Americans; it also suggested policies that will exacerbate the current problem.The reason for the high-inflation we’ve been seeing in recent months has been excessive government spending by both parties combined with record-low interest rates. The State of the Union was used to try to gain support for trillions of dollars of additional spending. There was also language suggesting that businesses cut costs (but without cutting wages we presume), and that even more government spending would be used to lower the cost of living for Americans.

This is not even remotely sound economic policy. It’s not possible to solve a problem caused by too much spending with even more spending. Further, while it might seem like an appealing idea that the government can reduce prices for people, the only way to accomplish this is higher taxes and/or more currency printing, which is exactly how we ended up where we are. More of what created the problem will not fix the problem.

The war in Ukraine is going to increase inflation in the United States, and is also making the Federal Reserve more cautious about raising rates, which would be the policy prescription to deal with the issue. The only positive in this situation is that if we know what’s coming, we can prepare. Our basic guide to hedging your portfolio and your home from further inflation is available here.