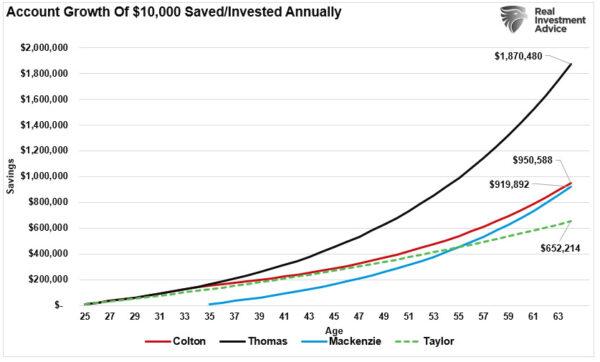

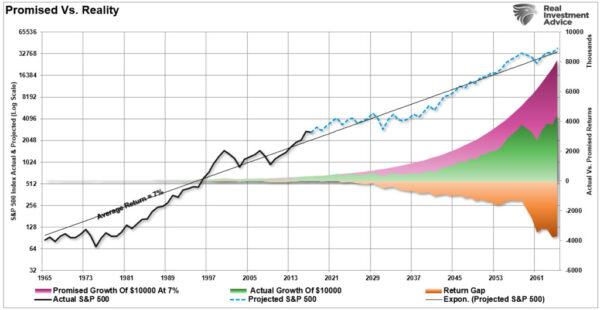

The younger generations should ignore the chart below that is often seen in a variety of forms in the financial media touting “how easy it is to become a millionaire.” There are two primary reasons millennials aren’t saving as they should. The first is the lack of money to save, and the second is that markets do not compound returns.

- Thomas invests for his entire working life, from 25 to 65.

- Mackenzie starts 10 years later, investing from 35 to 65.

- Colton puts money away for only 10 years at the start of his career, from 25 to 35.

- Taylor saves from 25 to 65, like Thomas, but instead of being moderately aggressive with her investments, she simply holds cash at a 2.25 percent annual return.

At first glance, it is apparent that starting a consistent saving and investing program early in life leads to the best financial outcomes. Of course, such is entirely logical.

The Saving Problem

The first problem is quite evident when looking at recent financial surveys of average Americans. For example, a recent Bankrate survey found:“Only about 4 in 10 Americans have enough savings to cover an unplanned expense of $1,000, meaning more than half would need to find other means to pay for an unexpected car repair or emergency room visit.”

Of course, with inflation surging in 2022, another more recent Bankrate study found that more than half of adults are uncomfortable with their level of emergency savings.

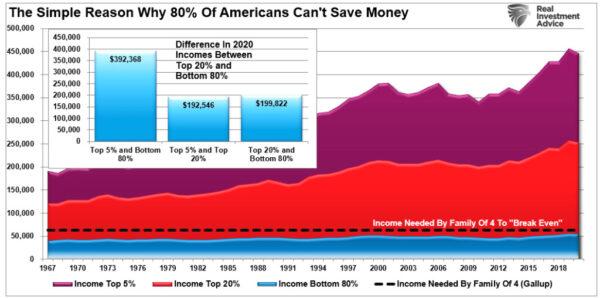

For most millennials, the idea of saving $10,000 a year sounds great; the problem is that the median income in the United States barely covers the cost of living, much less leaving excess savings. As shown, the median income in the United States for 80 percent of wage earners is $53,663 (via the Census Bureau, 2020 most recent data).

The problem is, of course, the generalized assumption that millennials are able to save roughly 25 percent of their annual aftertax incomes. This is not a realistic assumption, given that many of the millennial age group are struggling with student loan and credit card debts, car notes, apartment rent, etc.

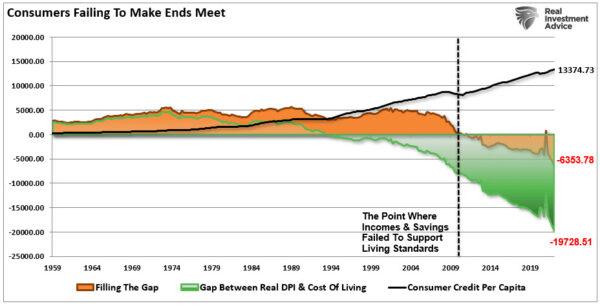

In fact, the current gap between savings/income and the cost of living is running at the highest annual deficit on record. It currently requires roughly $6,300 a year in additional debt to maintain the current standard of living. Either that or spending gets reduced, which is the likely outcome as a recession becomes more visible.

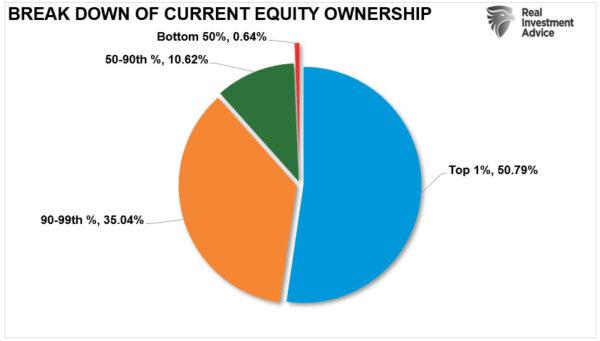

Of course, if you don’t have excess cash flow, it is really difficult to invest in the financial markets. That’s why those in the top 10 percent of income earnings own roughly 90 percent of the entire stock market.

Therefore, when it’s understood about the lack of financial stability in the vast majority of households, how are Thomas, Mackenzie, Colton, and Taylor supposed to save $10,000 a year? That’s a questionable proposition when Thomas works in customer service, Mackenzie is a nursing assistant, Taylor is a bartender, and Colton works retail. These are the jobs that have made up a bulk of the employment increases since 2009. They also are in the lower wage-paying scales, which makes the problem of savings difficult.

That’s why, according to the Pew Research Center, millennials are setting new records for living with their parents.

Stocks Do Not Deliver Compound Rates of Return

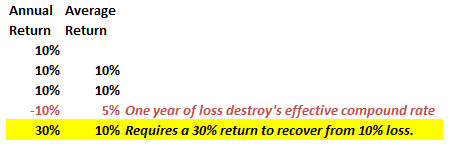

The second major problem with the analysis is the assumption that stocks deliver compounded returns over the long term. This is one of the biggest fallacies perpetrated by Wall Street on individuals in the effort to entice them to sink their money in fee-based investment strategies and forget about them.“While the average rate of return may have been 10 percent over the long term, the markets do not deliver 10 percent yearly. Let’s assume an investor wants to compound their returns by 10 percent a year over five years. We can do some basic math”:

“After three years of 10 percent returns, a drawdown of just 10 percent cuts the average annual compound growth rate by 50 percent. Furthermore, it then requires a 30 percent return to regain the average rate of return required.”

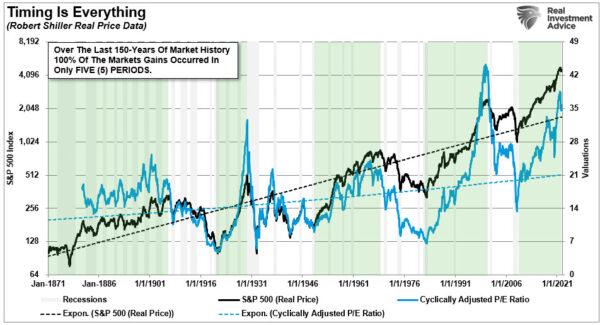

Timing Is Everything

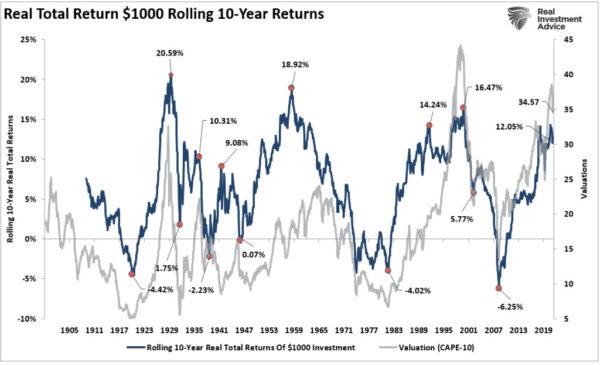

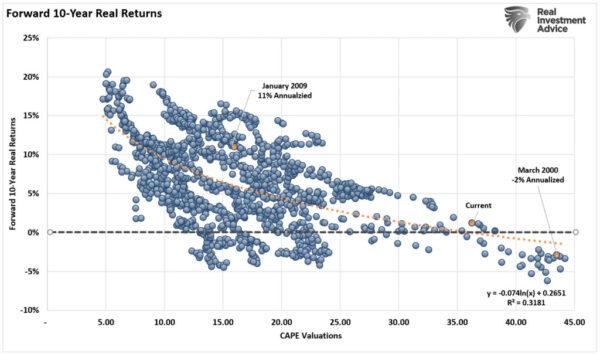

Last—and probably the most critical point—is the valuation level of the market when these individuals began the saving and investing program.

The return has everything with valuations and whether multiples are expanding or contracting. As shown in the chart above, real rates of return rise when valuations expand from low to high levels. But real rates of return fall sharply when valuations have historically exceeded 23 times trailing earnings and revert to their long-term mean.

Conclusion

While long-term and buy-and-hold investment strategies sound good at face value, the real-world outcomes fell short for three reasons:- Lack of savings;

- Inability to remain consistent; and

- Impact of negative returns on long-term goals.

It also should be somewhat evident that long-term and buy-and-hold strategies don’t work as promised when you consider the charts above. After three significant bull markets since 1980, the bottom 80–90 percent of Americans have little wealth to show for it.

This is due to a myriad of poor investment decisions, terrible advice from the financial media, and a predatory Wall Street taking advantage of unwitting investors.

Don’t misunderstand me. Should individuals invest in the financial markets? Absolutely. However, it should be done with a solid investment discipline that takes into account the importance of managing volatility and psychological investment risks. There are many great advisers that do exactly that; unfortunately, they generally aren’t found on the front pages of investment publications or in the financial media.

Of course, the problem to solve first is getting millennials out of their parents’ basements and back into the workforce. Having a job makes it easier to start investing, to begin with.