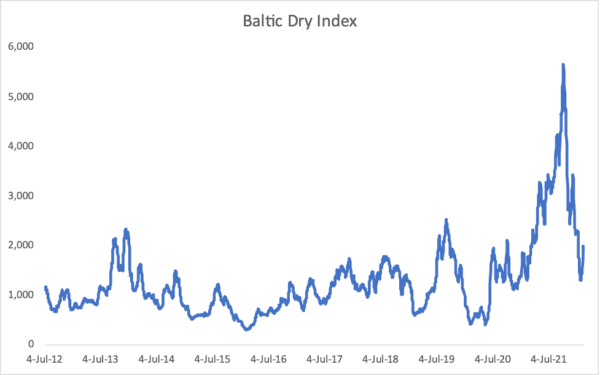

A big part of the argument against the concerns we’ve expressed is the belief that much of current inflation is due to supply problems. (While we acknowledge that the global supply chain is a mess at the moment, we believe that excessive money printing and negative real interest rates are the key culprits here.) They point to the recent reduction in shipping rates as proof that the global supply chain issues are easing, and that with more goods making their way to market, pricing issues will subside. The primary measure they look at is the Baltic Dry Index, and we agree that pricing has come down substantially.

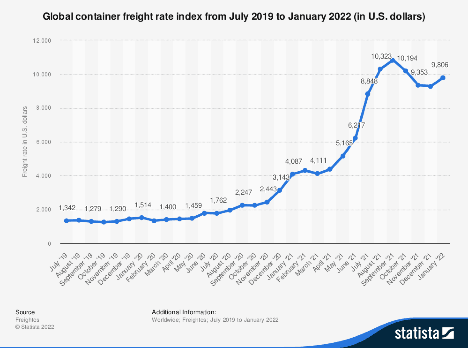

The Global container freight index is also down but by a much smaller amount.

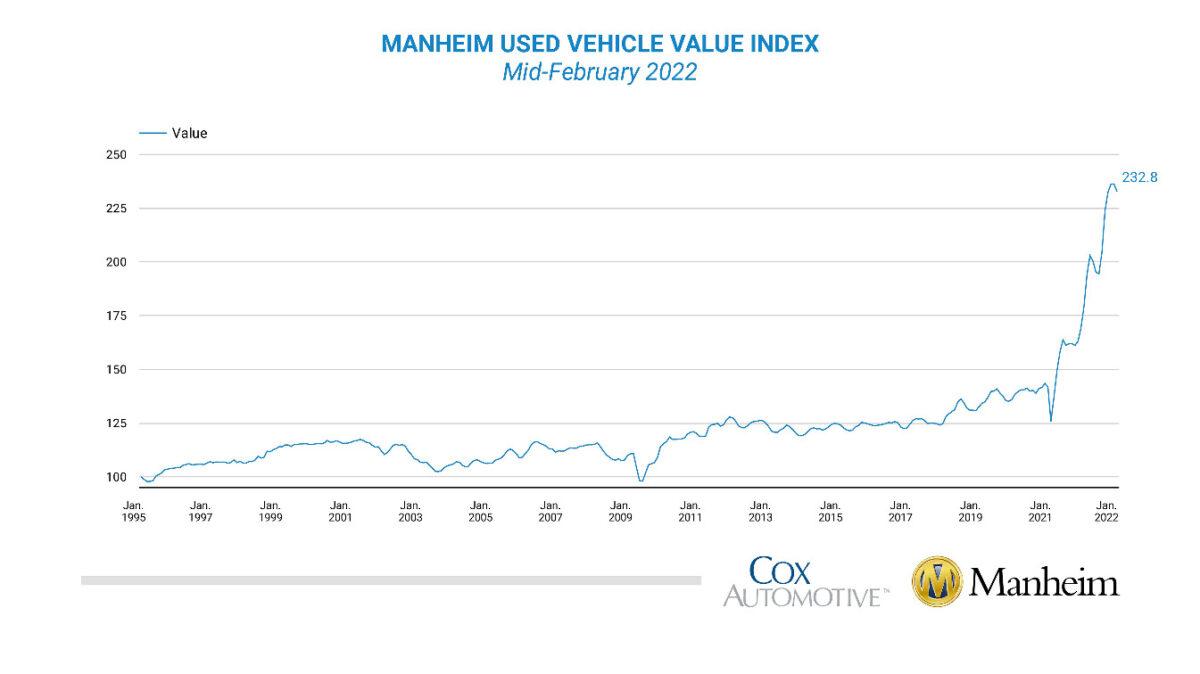

A second reason some think concerns about inflation are overdone is used car prices. According to the U.S. Bureau of Labor Statistics, used car prices have risen 40.5 percent in the last year. At just over 4 percent of the Consumer Price Index (CPI), that means that 22 percent of the recent huge increase in the CPI was due to used cars alone. While we’re less enthused than others about the first decrease in the Manheim Used Vehicle Value Index in a long time, we do think it’s reasonable to expect that used car prices won’t be up another 40 percent in 2022. Even if car prices stay flat this year (maintaining their already high level), it will remove a significant reason for the rise in inflation over the past year.

We also acknowledge that our last column in this newspaper gives a reason to believe that inflation could subside. While we have argued that the increase in the price of shelter (the term for housing at the Bureau of Labor Statistics) is undercounted in the CPI, the coming higher interest rates could reverse the trend. Higher interest rates mean higher mortgage rates which in turn require that home buyers pay lower prices to be able to afford the same home. Because shelter makes up about one-third of the CPI, any reversal of the upward trend in housing prices would lead to reduced inflation reporting. We do note that decreasing home prices due to lower affordability isn’t a great recipe for a better economy for U.S. citizens, but it would result in a lower CPI number.

One last factor to consider is reflexivity, or the tendency of economic systems to self-correct. Oil is an excellent example of this. As oil prices rise, producers have an incentive to add additional wells and pump more. At the same time, higher oil prices incentivize consumers to drive less, and turn the thermostat at home to a lower temperature in the winter reducing demand. So, high oil prices create conditions that both encourage more supply and less demand which lowers prices.

Consumer goods experience the same reflexivity with the added factor of expectations which influences results. When people believe that prices for goods are about to rise, they rush to buy now, and if they can afford it, will buy extra supplies for later. This can cause supply shortages and lead to higher prices. If the Federal Reserve can convince consumers that they have the situation under control, there will be less advance (or panic) buying, and less pressure on the supply chain. This would lead to a reduction in the inflationary pricing trend. Simply stated, expectations of inflation can lead to actual inflation while confidence in the central bank can create the opposite result. Finally, there is always the possibility that Federal Reserve interest rate increases could crash the economy. That would make the people unconcerned about inflation correct on that count, and us correct in our pessimistic outlook.

As of this writing, we continue to believe that inflation is worse than the official CPI statistics show and that Gross Domestic Product (GDP) is much lower than the official statistics. That’s a bad situation, and the comments in our articles are indicating that many Americans are seeing these effects in their personal lives and homes. However, in the interest of examining the issue from all perspectives, we can understand why others see the situation as transitory. We will continue to watch for the above-listed factors and evaluate whether our current view should be revised.