There is a simple, but often overlooked, truth about market bubbles.

Market bubbles have NOTHING to do with valuations or fundamentals.

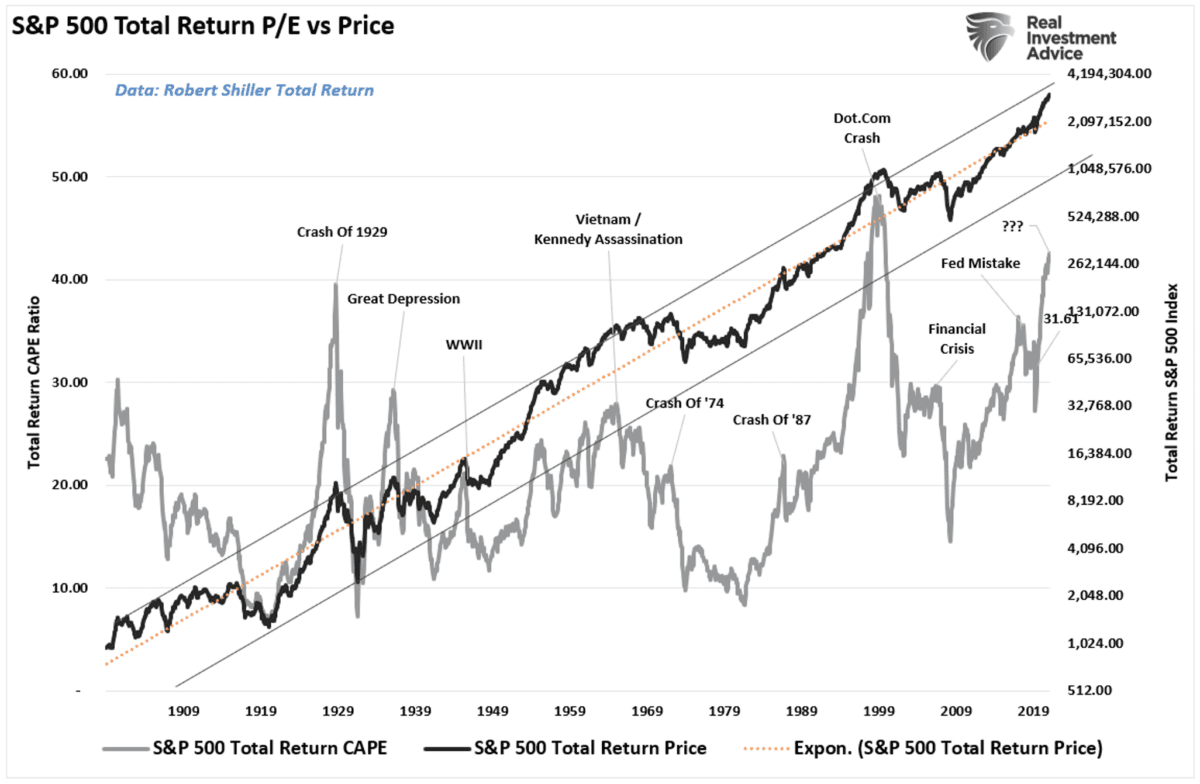

Yes, currently valuations are at levels only seen at the peak of previous bull markets. As shown, the S&P 500 currently trades in the upper 90 percent of its historical valuation levels.

However, since stock market “bubbles” reflect speculation, greed, emotional biases, valuations are the reflection of those psychological tendencies. As such, price becomes more reflective of psychology.

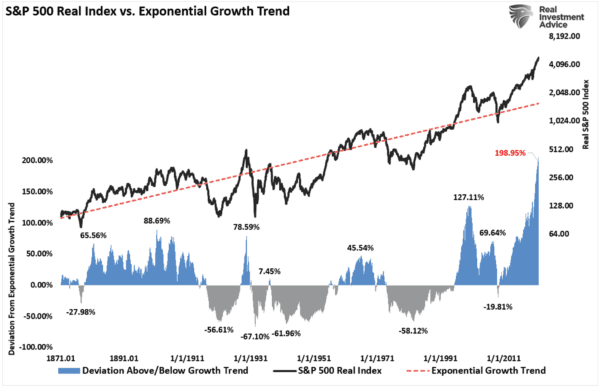

From a “price perspective,” the level of “greed” is on full display. Currently, the S&P 500 trades at the greatest deviation on record from its long-term exponential trend. (Such is hard to reconcile given a 35 percent correction in 2020.)

No Bubble Is Ever the Same

Historically, all market crashes have been the result of things unrelated to valuation levels. Issues such as liquidity, government actions, monetary policy mistakes, recessions, or inflationary spikes are the culprits that trigger the reversion in sentiment.Importantly, the bubbles and busts are never the same.

“It can be most reasonably assumed that markets are efficient enough that every bubble is significantly different than the previous one. A new bubble will always be different from the previous one(s). Such is since investors will only bid prices to extreme overvaluation levels if they are sure it is not repeating what led to the previous bubbles.

“As an analogy, no matter how thoroughly a fatal car crash is studied, there will still be other fatal car crashes. Such is true even if we avoid all previous accident-causing mistakes,” said Bob Bronson via Advisor Perspectives.

The current market cycle is not like 1995, 1999, or 2007? Valuations, economics, drivers, etc. are all different from one cycle to the next.

Most importantly, however, the financial markets adapt to the cause of the previous fatal crashes.

George Soros and the Theory of Reflexivity

With this background, we can better understand Soros’ “theory of reflexivity.” Such is a theory discussed by legendary billionaire investor, George Soros.“Financial markets, far from accurately reflecting all the available knowledge, always provide a distorted view of reality. The degree of distortion may vary from time to time. Sometimes it’s quite insignificant, at other times, it is quite pronounced. When there is a significant divergence between market prices and the underlying reality, there is a lack of equilibrium conditions.

“Every bubble has two components: an underlying trend that prevails in reality and a misconception relating to that trend. When a positive feedback develops between the trend and the misconception, it sets a boom-bust process in motion. The process is liable to be tested by negative feedback along the way. If it is strong enough to survive these tests, it reinforces both the trend and the misconception,” said Soros.

Eventually, market expectations become so far removed from reality if forces people to recognize that a misconception is involved. A twilight period ensues during which doubts grow. More and more people lose faith, but the inertia sustains the prevailing trend.

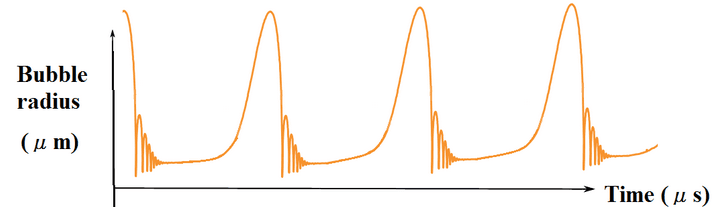

Typically bubbles have an asymmetric shape. The boom is long and slow to start. It accelerates gradually until it flattens out again during the twilight period. The bust is short and steep because it involves the forced liquidation of unsound positions.”

The chart below is an example of asymmetric bubbles.

Soros’s view on the pattern of bubbles is interesting because it changes the argument from a fundamental view to a technical view. Prices reflect the psychology of the market, creating a feedback loop between the markets and fundamentals. As Soros stated:

“Financial markets do not play a purely passive role; they can also affect the so-called fundamentals they are supposed to reflect. These two functions that financial markets perform, work in opposite directions. In the passive or cognitive function, the fundamentals are supposed to determine market prices. In the active or manipulative function market, prices find ways of influencing the fundamentals. When both functions operate at the same time, they interfere with each other. The supposedly independent variable of one function is the dependent variable, so neither function has a truly independent variable. As a result, neither market prices nor the underlying reality is fully determined. Both suffer from an element of uncertainty that cannot be quantified.”

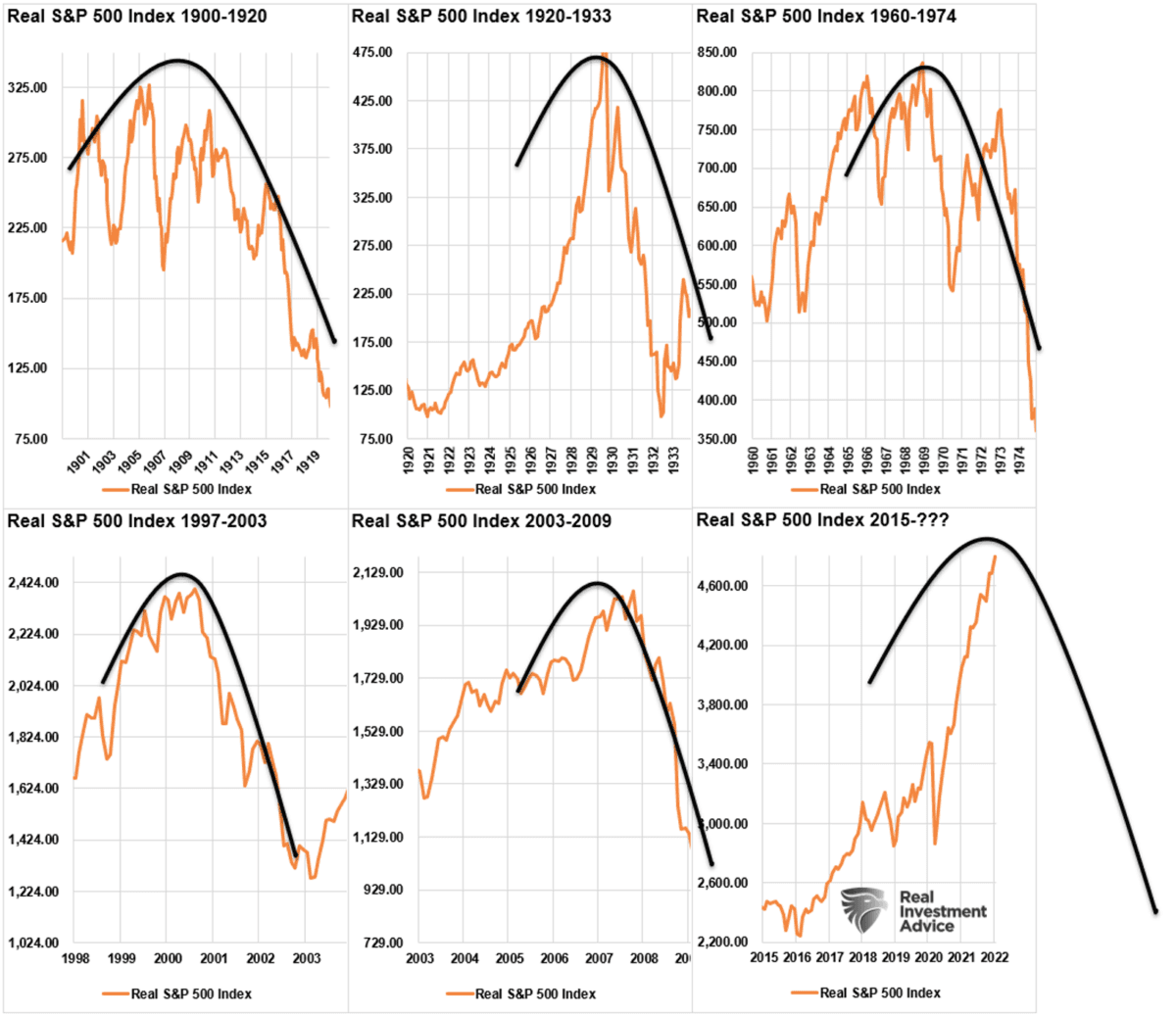

The chart below utilizes Dr. Robert Shiller’s stock market data going back to 1900 on an inflation-adjusted basis. I then overlaid Soros’ asymmetrical bubble shape.

Conclusion

There is currently much debate about the health of financial markets. Can prices remain detached from the fundamentals long enough for the economic/earnings recession to catch up with prices?Maybe. It has just never happened.

Furthermore, investors have become “trained” by the markets to “stay invested” for “fear of missing out.”

The increase in speculative risks, combined with excess leverage, leave the markets vulnerable to a sizable correction. The only missing ingredient for such a correction currently is the catalyst that starts the panic for the exit.

It is reminiscent of the market peak of 1929 when Dr. Irving Fisher uttered his now-famous words: “Stocks have now reached a permanently high plateau.”