The Fed is meeting and will make their policy pronouncement this week. In the meantime, European Central Bank (ECB) officials are hinting that more ECB interest rate cuts are coming, and the Bank of Canada should also be cutting key interest rates at its next meeting. This will put more pressure on the Fed to cut rates. The wild card in the global interest rate collapse is China, since currency devaluation rumors persist there, as China’s rates have collapsed and can’t go much lower.

Kevin Warsh, a former Federal Reserve governor who is emerging as the leading candidate to replace Fed Chair Jerome Powell in 2026, continues to criticize the Fed. Recently, Warsh said central banks: (1) talk too much, (2) get too involved in social issues, and (3) let lawmakers run up excessive deficits. Warsh said, “Fed leaders would be well served to skip opportunities to share their latest musings,” adding that Fed officials shouldn’t reveal their economic forecasts because they “become prisoners of their own words.” Warsh counsels a major reset: “A strategic reset is necessary to mitigate losses of credibility.”

Treasury Secretary Scott Bessent has joined President Trump in calling for a Fed rate cut. Specifically, Secretary Bessent points out that two-year Treasury yields are substantially below the Federal funds rate, so he said on Fox Business that seeing two-year rates below Fed funds rates is “a market signal” that bond traders “think the Fed should be cutting.” The Fed governors, however, hinted that Friday’s healthy jobs report makes a rate cut this week less likely. I argue that the details of that report are not so bullish, and other economic indicators cry out for a rate cut.

Here are the most important market news items and what this news means:

- The truth of the matter is that after a 41.3% surge in imports in the first quarter, goods have been “dumped” in America that now have to be discounted to move bloated inventories. The other interesting development is that the halt in shipments is now thawing. As an example, Jaguar Land Rover has resumed shipments of vehicles to the U.S. after pausing them in early April. In an official statement, Jaguar Land Rover said, “The USA is an important market for JLR’s luxury brands and 25% tariffs on autos remain in place.” He added, “As we work to address the new U.S. trading terms with our business partners, we are enacting our planned short-term actions.” What Jaguar Land Rover did not say is that their inventories were bloated, and they had to divert some of their inventories to the U.S.

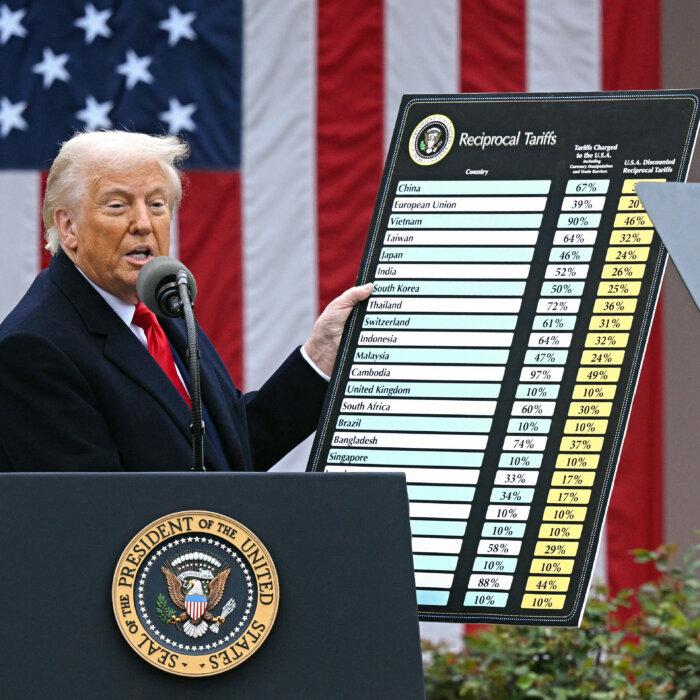

- The irony is that most reciprocal tariffs are not expected to be enacted, since most countries will be lowering their respective trade barriers and promising to buy U.S. goods. The primary reciprocal tariffs are against China, which recently exempted 131 U.S. goods from tariffs that account for approximately $40 billion in trade. So, the good news is that there is apparently a “thaw” in the trade dispute between China and the U.S.

- Warren Buffett, who is 94 years old, recently announced that he will be retiring as the head of Berkshire Hathaway. The private businesses that Berkshire Hathaway owns, like Borsheims (jewelry store), Nebraska Furniture Mart, See’s Candies, as well as its real estate business, may be a bit inflated compared to if they were spun off. Essentially, these private businesses are commanding a “Buffett valuation premium,” so it will be interesting if Berkshire Hathaway’s valuation suffers long-term from Warren Buffett’s well-deserved retirement. Near-term, the anticipated decline in interest rates should help Berkshire Hathaway, since insurance companies have massive bond portfolios.

- The Institute of Supply Management’s (ISM) non-manufacturing, service index rose to 51.6 in April, up from 50.8 in March. I was encouraged that the new order component rose to 52.3 in April, up from 50.4 in March. However, the business activity component slowed to 53.7 in April, down from 55.9 in March. Only 11 of the 17 service industries surveyed report growth in April, down from 14 industries that expanded in March. Overall, the ISM service index was better than economists expected, despite some confusing details.

- The Commerce Department on Tuesday announced that the March trade deficit rose 14.5% to $140.5 billion, which was substantially higher than economists’ consensus estimate of $136 million. So far, year to date, the trade deficit has doubled compared to the same period a year ago, even with a 23.3% increase in exports, so the dumping of goods to beat tariffs persists. In March, imports rose 4.4% to $419 billion, while exports increased slightly by 0.2% to $278.5 billion. Due to the larger-than-expected March trade deficit, first-quarter GDP may be revised lower.

In summary, this week is all about the Fed. The Federal Open Market Committee (FOMC) has to decide if they want to defy (1) President Trump, (2) Treasury Secretary Bessent, (3) deflationary forces, (4) surging new unemployment claims, (5) lower Treasury yields and (6) collapsing global interest rates by holding key interest rates steady. Trump and Bessent’s calls for a key interest rate cut are based merely on the fact that Treasury rates have fallen well below the Federal Funds rate. Furthermore, now that homebuilders have to discount homes to sell them, deflation is spreading fast, which can only be counteracted by falling interest rates.