It gets stated that “bears are like a ‘broken clock,’ they are right twice a day.” While it may seem true during a rising bull market, the reality is that the “broken clock syndrome” owns both “bulls” and “bears.”

The statement exposes the ignorance, or bias, of those making such a claim. If you invert the logic, this becomes clear.

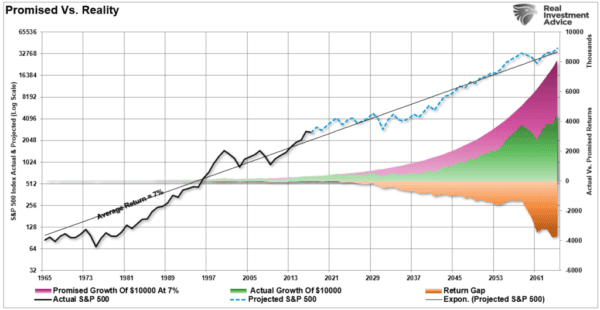

“There is a massive difference between AVERAGE and ACTUAL returns on invested capital. Thus, in any given year, the impact of losses destroys the annualized ‘compounding’ effect of money.”

Bull market cycles are only one-half of the “full market” cycle throughout history. Such is because, during every “bull market” cycle, the markets and economy build up excesses that are then “reverted” during the following “bear market.” In other words, as Sir Issac Newton once stated:

“What goes up must come down.”

Bulls Are Wrong at the Worst Time

Recently, Nick Maggiulli penned an interesting article on “the broken clock.” He noted that Robert Kiyosaki, author of “Rich Dad, Poor Dad,” had predicted a giant stock market crash. Kiyosaki had made incorrect predictions in the past, Nick said:“But the real tragedy here is that he will be right one day. One day a crash will come, and Kiyosaki will take a victory lap for all to see.

“Will his prior incorrect calls matter? Not at all. You can try to point out his poor track record, but it won’t make a difference. Most people aren’t going to see your reply. But what they will see is his tweet. They will feel the pain from the crash after it happens, and then they will think, ‘Kiyosaki knew it all along.’

We give Nick a pass because he is young and has not lived through an actual bear market. Anyone who has will tell you that it is not an adventure they care to repeat.

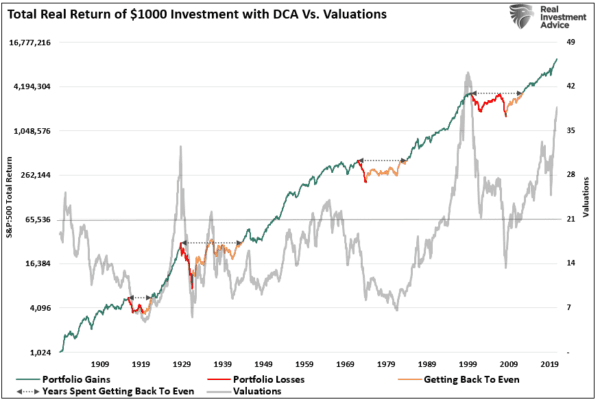

The problem with being “bullish all the time” is that when you are eventually wrong, it comes at the worst possible cost; the destruction of investment capital. While being “bearish all the time” also has a cost, it comes only at the expense of underperforming markets during a bullish phase. A lack of performance is quickly recovered; a loss of capital is not.

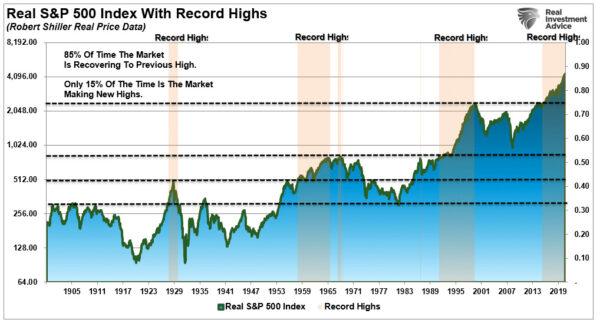

While the “bulls” seem to have their way during rising markets, there is a problem overlooked by the consistently bullish media. Over the past 120-years, the market has indeed grown. However, the markets spent 85 percent of that time making up previous losses. The markets spent only 15 percent of the time making new highs.

The importance of this point should not be overlooked. For most investors, their investing “time horizon” only covers one cycle of the market. Suppose you are starting at or near all-time highs. There is a relatively significant possibility you may wind up spending a considerable chunk of your time horizon “getting back to even.”

The Fallacy of the ‘Broken Clock’

I previously quoted John Hussman, who made an excellent point on the importance of understanding the “full market cycle”:“Put simply, most apparent ‘opportunities’ to obtain investment returns above zero in conventional assets over the coming decade are based on a misunderstanding of valuations, total returns, and historical yield relationships. At current valuations, virtually everything is priced for a decade of zero. The unwinding of these speculative extremes is likely to be chaotic and will likely occur over a shorter horizon than investors imagine. That chaos, driven not by central bank tightening but by an emerging default cycle, will usher in fresh investment opportunities in conventional assets, where presently there are none.

Yes, the markets have corrected somewhat this year, but the majority of the mean-reverting event needed to clear the system has yet to occur.

As I have often stated, I am not bullish or bearish. While my discussions of “risk management,” market conditions, and valuations are often perceived as bearish, with many assuming we are all in cash, such is never the case.

My job as a portfolio manager is simple; invest money in a manner that creates returns on a short-term basis but reduces the possibility of catastrophic losses that wipe out years of growth.

In our view, you should not be “bullish” or “bearish.” While being “right” during the first half of the cycle is important, it is far more critical not to be “wrong” during the second half.

We aren’t sure the second half of the cycle has begun. But if it has, it isn’t too late to make adjustments and consider the consequences of ignoring the potential for a “reversion to the mean.”