But on Friday, Secretary of the Treasury Janet Yellen shocked the markets by writing congressional leaders to advise them that the debt ceiling would be reached by Jan. 19.

Wow.

Yellen will, presumably, cobble together ongoing revenue streams from taxes, fees, and tariffs to pay interest on the debt and other critical expenses. That would likely push off a default date—when the government actually becomes insolvent and misses payments—into the summer sometime, when Washington traditionally empties out as members of Congress return to their districts and states. So the pressure will be on to resolve the debt ceiling issue as soon as possible.

But the debt ceiling—and, more important, the underlying issue of spending—simply must be addressed and as urgently as possible.

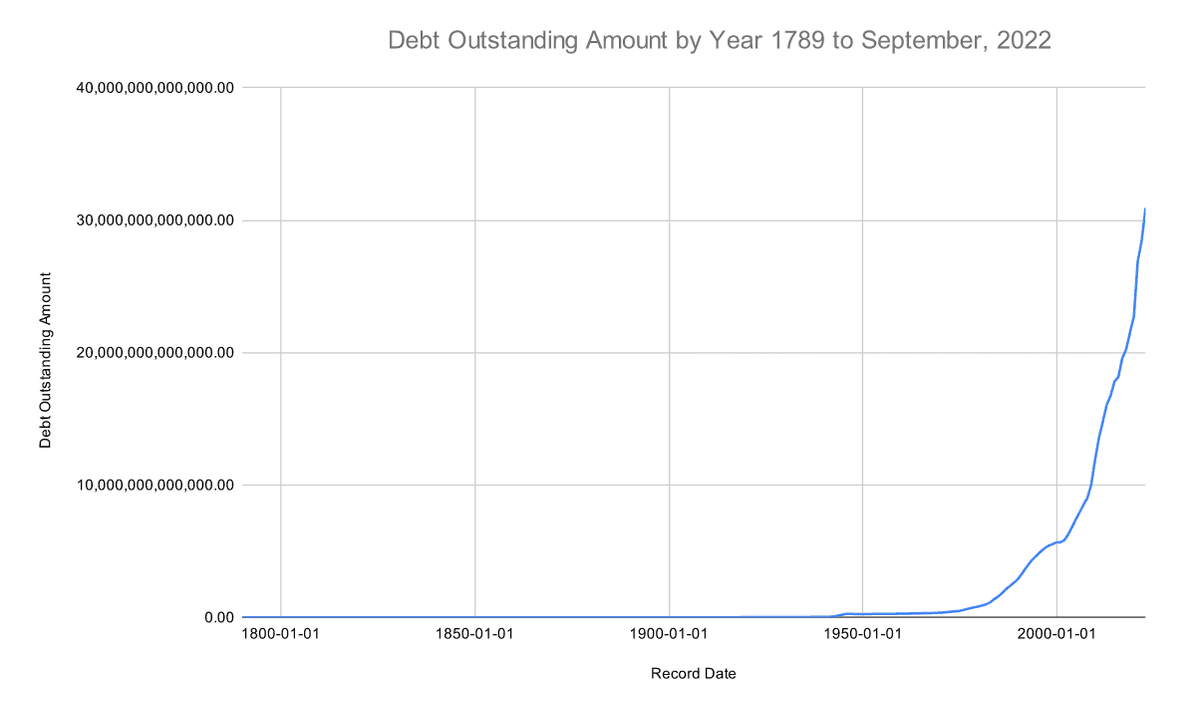

Keep in mind that since the turn of the last century (i.e., 1901), large deficits, in pure dollar terms, were a relative rarity. But debt started to grow in the 1940s, for the war, as illustrated below. It took us from the beginning of the republic to about 1981 to reach a trillion dollars in debt. But 40 years later, we have grown that debt by more than 30 times that amount. Our debt has, simultaneously, gone from about 30 percent of gross domestic product (GDP) to more than 120 percent of GDP, or nearly $94,000 for every man, woman, and child in the United States. In other words, a family of four has debt of nearly $400,000.

Like someone who has gorged themselves on junk food, our spending has made us grotesquely obese, in a fiscal sense, and limited our national fitness to carry on the activities of a world power and to provide for the well-being of our people.

Our Debt Is Debilitating

It’s no coincidence that the salad days of the republic all happened in the last century. Those were the fiscally fit days, when America could save Europe from its wars—not once, but twice—finance its postwar reconstruction, as well as Japan’s, and emerge as the global protector of “democracy,” even as we welcomed global competitors to our own industries from our former enemies.But today things are different. We are no longer that country. Neither is the rest of the world the way it was. Europe and Asia are, by and large, fully developed first-world nations and competitive economies. The GDPs of the United Kingdom and European Union are, together, almost equal to that of the United States. And the combined populations of the United Kingdom and the European Union, at more than 500 million, exceeds that of the United States. America is no longer the Northern Hemisphere’s “Big Brother”; and it should not be treated as such by Europeans or our allies in Asia.

A Fiscal Fitness Plan for America

As I wrote before, “Sealing the ceiling deal will require some ‘adults in the room’ as we the address the twin looming catastrophes of a sovereign debt downgrade by the credit ratings agencies or a sovereign debt crisis in which the world loses confidence in the U.S. dollar." Freezing spending at 2022 levels is fine for an exigent Band-Aid for the debt ceiling debate, but America needs a comprehensive and forward-thinking solution, one that ensures the fiscal sovereignty and economic integrity of the United States well into the twenty-second century.- Foreign Policy

- Define vital American foreign interests and appropriate the amount of funds necessary to defend them, not vice-versa. Recognize what we “must do” militarily versus what we “would like to do.” “Discretionary” wars, such as nation-building in Afghanistan and Iraq, or the Vietnam quagmire, must be recognized—and avoided—for the mistakes they were and the consequences that resulted. Our defense missions should be as clearly defined as they are in Col. Harry Summers’ On Strategy, the seminal thesis of the critical lessons we learned from Vietnam and which were later popularized as “the Powell Doctrine”: first, assess whether a problem can even be resolved by military means; if so, define the mission, apply overwhelming military force, and carry it out. Then leave.

- Make clear that our allies must step up for their own defense. The United States spends 3.5 percent of its GDP on defense. But our NATO allies are only required to spend just 2 percent of their respective GDPs, and many have not even met that threshold. Every NATO member nation should have at least the same obligation to the alliance as the United States, both in funding as a percentage of GDP and in troops as a proportion to population. The “watch keepers” and “first responders” to European crises should be European NATO forces, not Americans. The United States should serve as a reserve force and a supplier of weapons, training, and intelligence. We should prepare for and enter a kinetic European war only as a last resort.

- Encourage Japan to re-arm. Nearly 80 years after its defeat, and with looming threats to Taiwan and American hegemony in the Western Pacific, the United States could use a capable, heavily-armed, democratic ally in the region. Japan’s Maritime Self-Defense Forces are superior seafarers which the United States should encourage to expand. Assisting the United States and our Pacific allies in defending Taiwan should be viewed by the Japanese people and government as an indirect defense of Japan itself so as to accommodate the Japanese constitutional prohibition against aggressive war.

- Broaden and strengthen our relationship with India, with both trade and defense. India is a natural ally as a democratic republic governed by the rule of law. Its enmity with communist China is deep and long-lived. For a budget-conscious United States, India has the potential to assist in containing China’s Peoples’ Liberation Army and Navy and to inhibit China’s desire for naval supremacy in the Indian Ocean, the Straits of Hormuz, the Gulf of Aden, and the South China Sea.

- Adopt a plan to extricate the United States from the World Trade Organization (WTO) and to separately negotiate bilateral trading terms with our major trading partners. As the world’s largest trading partner, the terms we could negotiate independent of the WTO could include the trade in services, an area where the United States leads, but that the WTO has been woefully neglectful to address.

- Fiscal Policy

- Adopt a tax code and regulatory regime that encourages entrepreneurship, investment, and employment by lowering rates and expanding the tax base, but allowing young people to accumulate wealth earlier and more rapidly so that they can raise families to ameliorate the demographic decline affecting all Western-style economies.

- Gradually eliminate the tax deduction for interest over 10 years to put equity and debt on the same plane for tax purposes. I say “gradually” only to avoid the market shock a sudden elimination of it would cause.

- Abandon the carried interest “loophole.” This is a prized ox of the American political contributor class that must be gored if the rest of the country is to endure it’s own financial sacrifices. Political favoritism owing to financial influence, or—worse±class, will sabotage the overall reform.

- Impose a Federal Insurance Contributions Act tax on all income, not just wages, to ensure Social Security and Medicare are solvent until the baby-boom and boomlet generations die out and the system is again self-sustaining. Recognize that the “entitlements” are a welfare program supported by taxes, the same as others. Raise the age to commence benefits to 70 and means-test benefits. When naysayers who get cut off because they exceed the income and wealth limits assert “but I paid into it my whole life,” have the political courage to reply that they paid into the defense budget “their whole lives,” too, and that, hopefully, they will never need to use it, either.

- Make interest on federal obligations tax free, as it was during World War I, to increase demand, drive down rates, and keep interest payments lower.

- General Government

- Adopt zero base budgeting, which has been used by American corporations and governments for more than 40 years to cut costs, boost efficiencies, and prioritize and reallocate resources. This was promised by former president Jimmy Carter, who had used it successfully in Georgia, but never came to be. With a budget hemorrhaging a trillion dollars or more per year, now is the time.

- Evaluate, consolidate, and eliminate cabinet departments. As we face massive deficits, the cabinet departments that were created to appease or coddle political constituencies, or to provide sinecures to political allies, are luxuries the government can no longer afford. It’s absurd that we have a secretaries of Agriculture, Labor, Housing and Urban Development, Education, Transportation, and Energy. They should be consolidated as they all relate to how the country does business—and would likely operate more efficiently—under the Department of Commerce instead of being kept in separate silos. Likewise, the Environmental Protection Agency should be rolled into the Department of the Interior. Homeland Security and Veterans Affairs should be rolled into the Department of Defense. There are other opportunities as well.

Financial luminaries such as Pete Peterson and William Simon have been warning of America’s massive debt for nearly all of my adult life. In that time, I’ve witnessed the decline in the American standard of living because we have been living off America’s past wealth and influence.

It’s time to face reality, come down to earn, and take the harsh steps to restore the fiscal health of America.