Markets are in a state of heightened anxiety as the Federal Reserve is shifting to a tightening stance with an abruptness not seen in decades. Since just last September, the Federal Funds rate expected to prevail in mid-2023 has increased by 1.25 percent according to futures markets.

While rapidly shifting its market guidance on the federal funds rate, the Fed has also announced an end to quantitative easing—the central bank’s program of buying Treasury securities—and has signaled a rapid pivot to quantitative tightening (QT), the sale of Treasury securities from the Fed’s bloated portfolio.

Markets are right to be unsettled by the Fed’s shift in interest rate policy, which has been effected with all the deftness of a dozing driver yanking the steering wheel, as he awakens to the expanding headlights of an 18-wheeler bearing down on him on a dark country road.

QE has three potential transmission channels:

- Forward guidance effects

- Asset side effects (suppressing Treasury yields)

- Liability-side effects (stuffing banks with reserves)

Forward Guidance Effects

Quantitative easing can really underscore the central bank’s intention to run a highly accommodative monetary policy. It gives market participants a guarantee that rates won’t be rising for some period of time and if the policy increases confidence in the central bank’s commitment to its inflation target, thereby raising inflation expectations, monetary conditions will be loosened. It’s a bit of a monetary parlor trick, but the well-documented “announcement effect” (long-term interest rates rising sharply) suggests that it works.Asset Side Effects

By “asset side” effects, we mean the Federal Reserve is adding to the asset side of their balance sheet by buying bonds, thereby removing interest rate risk from private markets. I am dismissive of the notion that this activity has a significant effect on long-term interest rates. That Fed purchases are offsetting a large proportion of Treasury new issuance is irrelevant. Their purchases must be viewed in relation to the total pool of outstanding securities—all $18T in private sector hands.If Fed purchases “manipulate rates” lower (pushing bond prices higher), any holder of a Treasury security is welcome to sell into that “Fed-manipulated” price at any moment. The fact is, that with the recent expansion of government debt, there is currently more Treasury interest-rate risk in private sector hands than ever before. The market is simply too big and liquid to push around, even for the Fed.

Liability Side Effects

By liability-side effect, we mean that the Fed pays for the bonds it buys by creating a liability on its balance sheet in the form of bank reserves. By stuffing banks with reserves that yield next-to-nothing (currently 0.15 percent), the Fed can motivate banks to create money by buying more assets or making more loans.The mechanism envisioned is a “hot potato effect.” If low-yielding bank reserves are inflicting a heavy opportunity cost on banks, they will endeavor to move them in favor of higher-yielding assets. The reserves get passed from one bank to another like “hot potatoes,” in exchange for assets (loans or securities), until the yields on available assets get bid down sufficiently to demotivate further reaching for yield, thereby “cooling the potatoes.”

But there’s a catch: the potato is only hot if the rate the Fed is paying banks to hold it is sufficiently below the market equilibrium interest rate. If, for example, the Fed is paying 0.25 percent interest on reserves (as it did from 2009 to 2015) but the market-equilibrium or “neutral” interest rate is negative (as it likely was then), you end up with cold potatoes. In that situation, banks are happy sitting on as many reserves as the central bank wants to create. The liability-creation is “pushing on a string.”

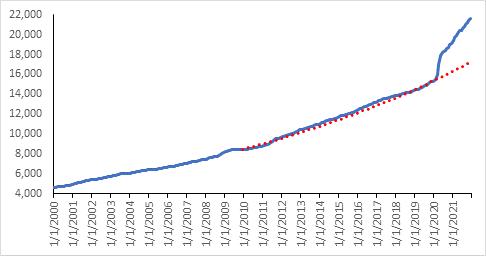

You can see the results in M2:

Monetarists are quite worried about this jump in money supply. Recall the equation of exchange, MV=PY or Money times velocity (or turnover) = the price level times real output (i.e., nominal GDP). Given the sharp rise in M2, it is an economic tautology that if velocity reverts to pre-pandemic levels, nominal GDP (and inflation) will rise sharply.

Of course, velocity need not return to pre-pandemic trend, so long as the Fed keeps the potatoes cool. The surplus M2 that’s been created can be “sterilized,” by increasing official interest rates up to the market equilibrium or “neutral” interest rate, thereby disincentivizing the use of these surplus funds in ways that might generate accelerating inflation.

The asymmetrical sequencing of the policy cycle renders QT considerably less potent than QE. A symmetrical policy cycle would proceed as follows: cut rates to zero, add liquidity via QE, withdraw liquidity via QT, then raise rates off zero. But that’s not the sequence they use.

Cold potatoes aren’t relevant for monetary policy, inflation, and markets.

This is not to say the Fed can’t do plenty of damage to markets and the economy with interest rate policy alone, particularly if they continue to operate the heavy machinery of monetary policy like a pillhead on prom night.

But the monetary action is all in the Funds rate. Quantitative tightening makes for exciting headlines but will have little influence over the direction of the economy, inflation, or financial markets in the coming year.