Commentary

A reader who had read my column, “The Day the Dollar Dies?” back in January wrote me and asked me to write a column on the relationship between fiscal deficits and trade deficits. I generally don’t take requests, but I think this one is important.

In the next few days, Congress will likely vote to continue to fund the government with a continuing resolution. I had rather hoped House Republicans would vote to shut down the government over spending and policy differences with the Biden White House. As I wrote in January, somehow, some way, we simply must get some reins around our humongous and out-of-control deficits and debt.

We have not been on the gold standard since 1971. The U.S. dollar fluctuates relative to the euro, the British pound, the Japanese yen, and assorted other currencies. That fluctuation is a function of the demand for U.S. goods, securities, and investments, including real estate and land, and U.S. demand for their foreign counterparts. Unlike the currencies of the free market economies, the Chinese yuan is pegged against a basket of different currencies as part of the Chinese Communist Party’s mercantilist trade policy.

First, let’s review how international trade works. And so that it’s clear, let me do my best to explain it (in the words of Denzel Washington’s character in the movie Philadelphia) as though my readers were third graders, because that’s the way I like things explained to me.

1. When Americans buy goods or invest abroad, we pay the seller in their own currency; so, we create demand for, say, the yen when we buy goods from Japan. When a foreigner buys goods from here or invests here, they pay in U.S. dollars.

2. If we buy lots of goods from Japan and they buy fewer goods from the United States, we say the United States has a balance-of-payments deficit and Japan has a balance-of-payments surplus.

3. Ultimately, in the grand scheme of international trade, these deficits and surpluses must cancel each other out in the long term and net to zero. That simply means that every country must pay for everything it purchases from another country.

4. For these surpluses and deficits to net to zero, all the U.S. dollars Japan has earned must be returned to the United States and all the yen the United States has earned must be returned to Japan.

In this very simplified example, we assume that Japan and the United States are the only two countries in the world. In reality, there are infinite combinations of surpluses and deficits among nations. But let’s keep it simple.

If Japan has a trade surplus, it has earned more U.S. dollars than Japan can spend in the United States. So, Japan must find some way to “recycle” the excess dollars it has earned back to the United States and receive something of worth in exchange.

An excellent real-world example was Sony’s spectacular success in the 1980s when it sold tens of millions of Walkman personal stereo units in the United States and collected dollars. The balance-of-payments surplus—billions of dollars—enabled Sony to acquire Columbia Pictures from Coca-Cola using dollars.

If that’s all clear, we can move on to how trade deficits affect fiscal deficits.

The United States runs—and has run—chronic trade deficits for decades.

Remember that a balance-of-payment surplus—having more of another country’s currency than you need—requires the holder of the foreign currency to recycle it to its native country in exchange for something of value. That could be merchandise and commodities, stocks, land and buildings, companies, or stocks and securities. (See the above example of Sony and Columbia Pictures, or China’s purchase of Smithfield, the pork producer.)

It’s the securities where the interplay between the fiscal deficit and the trade deficit is most evident.

The U.S. Treasury sells bonds to all comers. And the U.S. dollar, as the world’s reserve currency, is coveted as a store of value. So, those dollars held overseas can be recycled back to the United States as the purchase of U.S. Treasurys.

That demand for Treasurys from foreign exporters helps enable the Congress to spend well beyond U.S. tax revenues—to consume more than it takes in—and to finance the deficit with Treasurys. If one thinks of Congress as a free-spending alcoholic, our trade deficit isn’t buying the alcoholic a drink, but it’s lending him the cash he needs to buy his next drink. (I can remember one of the purported “conservative” think-tanks actually lauding this situation several years ago, effectively thinking the United States was paying for valuable goods and services in what amounted to, effectively, counterfeit!)

Ameliorating the Trade Deficit

There are a number of ways we could ameliorate this cancerous chronic trade deficit.One way would be to reduce the value of the dollar, something we’ve done in the past, even the recent past, with so-called quantitative easing (QE). That would make U.S. goods cheaper abroad, but also would make imported goods more expensive here. And while increasing the number of dollars in the economy, as occurred with QE, tends to make them cheaper in foreign markets, it tends to be inflationary at home.

Another way is to impose tariffs on imported goods, but foreign countries can retaliate with their own round of tariff increases, and we can go round for round with tariff increases until trade becomes almost impossible. (Many believe a similar round of tit-for-tat tariff increases exacerbated the Great Depression.)

But the best way to alleviate our trade deficits is to increase U.S. exports. That will strengthen the U.S. dollar, as demand for U.S. dollar will increase, and, because imports will be cheaper, will reduce the cost of living in the United States. It is, of course, easier said than done. But government policy can work to make American goods and services better and cheaper by boosting U.S. productivity and efficiency. For example, government can reduce regulations and use tax and fiscal policy to incentivize investments in worker training and equipment. It can ease the way for far more small and medium-sized businesses to export their goods and services. And congressional and state leaders can, with the State Department, step up the pace of foreign trade missions of U.S. consulates abroad and routinely include small and medium-sized enterprises.

Simultaneously, the U.S. trade representative and the secretary of state must insist that our trading partners remove non-tariff barriers in the trade in goods and services. Non-tariff barriers are regulations or laws that tend to favor domestic industries or professional services practices. They can include things as diverse as local work rules, restrictions on visas for foreign workers, domestic ownership requirements for certain businesses, and licensing requirements for professional practices.

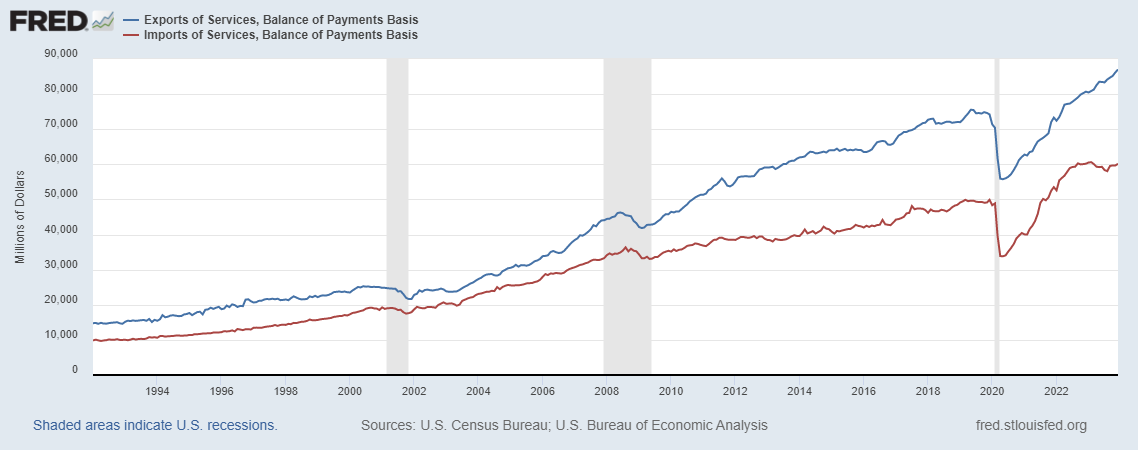

Licensing requirements, and their effect on the trade in services, is interesting because U.S. services are highly lucrative and we actually have a surplus in the trade in services, as illustrated in the chart:

The State Department and the U.S. trade representative should capitalize on the United States’s comparative advantage in services by pushing for more countries to adopt reciprocal licensing agreements for professions such as architecture, accountancy, and civil engineering. Groups such as the National Council of Architectural Registration Boards and the American Institute of Certified Public Accountants have worked on these efforts, but they have largely been piecemeal and mostly bilateral, with reciprocal licensing privileges granted between (or among) the counterparties. But they have had limited success. The next administration should seize on this objective as a central theme of its trade policy.

Summary

In the end, the value of a fiat currency to a foreigner is the value of the products and services that the foreigner can obtain from the country that issues the currency. That’s it; without those goods and services, foreign currency has all the worth of Monopoly money. Central bank monetary policy, governmental fiscal policy, and institutions such as the International Monetary Fund can affect that value, but cannot create it or substitute for it. If the United States wishes its dollar to continue as the world’s reserve currency—to maintain it’s “exorbitant privilege,” in the words of former French finance minister (and later French president) Valéry Giscard d'Estaing—it will control its deficits, boost its productivity, and promote its export trade.The next administration should pursue those objectives aggressively.