This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

The November jobs report showed that the economy added 263,000 new jobs, considerably better than the consensus estimate of 200,000 jobs. This morning’s print is 21,000 fewer jobs than were created in October 2022 and 384,000 fewer jobs than were created in the COVID recovery period of 2021. Net revisions for August and September added another 29,000 net new jobs. (It is generally believed that 200,000–250,000 jobs are required to accommodate population growth.)

The jobs print, 30 percent-plus more than were expected, very likely sets up continued rate hikes from the Federal Open Market Committee, the policy-making arm of the Federal Reserve, until there is a tipping point that indicates inflation is on a clear glide path toward the Fed’s preferred target of 2 percent.

The unemployment rate was 3.7 percent, unchanged from October. The labor force participation rate was 62.1 percent, down from 62.2 percent that printed in October.

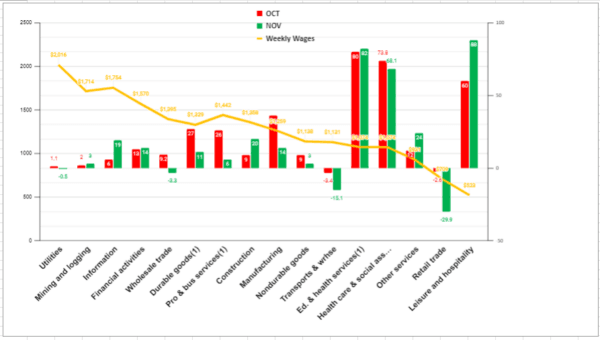

November and October jobs creation by average weekly wages from the the Bureau of Labor Statistics, Establishment Data. Copyright, the Stuyvesant Square Consultancy

The principal jobs creation was in lower-wage leisure and hospitality (waitstaff, bar tenders, and hotel maids, e.g.) and in education and health services that are heavily subsidized by government.

Surprisingly, retail workers are declining in November in the run-up to the holiday shopping season. This does not bode well for the overall economy, particularly given poor “Black Friday” sales.

Other Data

Federal Reserve Policy

Federal Reserve Chair Jerome Powell, in a speech Wednesday, said

... it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting.

As a consequence of the chairman’s comments, markets are widely expecting the December rate increase to drop down to 0.50 percent, though that may not be the case.

It does seem, however, that there is a modicum of disinflation, but it cannot be assured from a single data point. The October Personal Consumption Expenditure price index printed at 6 percent. That’s down from 6.3 percent.

Markets

While Congress has passed, and the president is expected to sign, legislation forcing railroad workers to work, it is not all that simple. Railroad crews can engage in a rule-book slowdown, by which crews strictly follow all the rules that govern rail transport. This will slow rail service considerably. Neither the government or the railroads can do anything about it as the railroad crews are only doing things “by the book.”

There are going to be supply-chain disruptions coming out of China because of the country’s draconian lockdowns and protests. This will affect Apple in particular, and some others, so that earnings in the fourth quarter and first quarter of 2023 will be less than anticipated.

The jobs market is still exceedingly tight, and worse than we have seen in more than 20 years. The Beveridge Curve—which charts the job openings rate along the horizontal axis versus the unemployment rate along the horizontal axis, and in which the unemployment rate traditionally exceeds job openings—is printing at an extremely high rate because the job opening rate is virtually double the unemployment rate. That is unlikely to change anytime soon, absent the Fed creating a significant slowdown. Consequently, wages—and inflation—will continue due to cost-push inflation.

Privately owned housing units authorized by building permits in October were at a seasonally adjusted annual rate of 1,526,000.

This is 2.4 percent below the revised September rate of 1,564,000 and is 10.1 percent below the October 2021 rate of 1,698,000.

The jobs print and increase in nominal wages will likely cause the Fed to continue at the rate-hike pace of 75 basis points, notwithstanding Chairman Powell’s comments earlier this week. However, as I wrote recently, there are some in the Fed who may be willing to accept a higher target rate of inflation. We'll know how much influence they have when the FOMC meets later this month. In the lead-up to a presidential election year in 2024, and with multiple competitive Senate seats up, and the entire House, it seems politics will enter into the Fed’s decision.

We think fourth-quarter GDP will print in the neighborhood of 1.5 percent.

____________________________________________

DISCLOSURE: The views expressed, including the outcome of future events, are the opinions of The Stuyvesant Square Consultancy and its management only as of December 2, 2022, and will not be revised for events after this document is submitted to The Epoch Times editors for publication. Statements herein do not represent, and should not be considered to be, investment advice. You should not use this article for that purpose. This article includes forward looking statements as to future events that may or may not develop as the writer opines. Before making any investment decision you should consult your own investment, business, legal, tax, and financial advisers. We associate with principals of TechnoMetrica on survey work in some elements of our business.

Note: Our economic and business commentaries most often tend to be event-driven. They are mostly written from a public policy, economic, or political/geopolitical perspective. Some are written from a management consulting perspective for companies that we believe to be under-performing and include strategies that we would recommend were the companies our clients.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

J.G. Collins is managing director of the Stuyvesant Square Consultancy, a strategic advisory, market survey, and consulting firm in New York. His writings on economics, trade, politics, and public policy have appeared in Forbes, the New York Post, Crain’s New York Business, The Hill, The American Conservative, and other publications.