A provision in an upcoming securities regulation for the financial services sector could bring changes to the way banks and asset managers do business and interact with clients.

That transformation agent is the Marketing in Financial Instruments Directive II (MiFID II), which goes into effect Jan. 3, 2018, in the European Union. The law seeks to offer more investor protections and greater transparency on products sold and marketed by banks and asset managers.

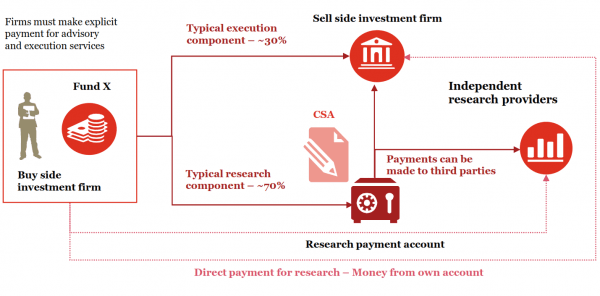

Among the voluminous requirements within MiFID II is a provision called “unbundling,” which requires banks and brokers to separate investment research—traditionally a “complimentary” product—from execution services. And this little-known rule could potentially disrupt the whole industry.

Traditionally, asset managers pay banks and broker-dealers for execution services—the purchase, settlement, reconciliation, and eventual sale of investments that banks carry out on behalf of asset manager clients. As part of paying for such execution services, asset managers receive investment research from banks for no additional charge.

But European regulators want this dynamic to change. Investors who give asset managers money to manage generally pay for trade execution—it’s an added cost, in addition to management fees. MiFID II demands asset managers break out, or unbundle, the cost of research from the cost of execution. The rules require that banks and brokers break out the cost of research from execution to clarify to their clients—the asset managers—what exact services they are paying for.

The regulations aren’t limited to the EU. Any financial institution trading European securities is affected.

This may sound reasonable and easy to implement, but the reality is not so simple. Currently, banks generate and provide far more investment research—often beyond the scope of client needs—than necessary, mainly to drum up business and encourage more trading activity (more revenue for banks). And since this was all provided for free as part of execution activities, and the research division was never a profit center for the bank, little thought was given to the value of this service or how to sell it independently.

By converting research into a new product of its own, MiFID II could drastically change the dynamic and relationship between banks, asset managers, and end-user investors.

Advantage: Large Asset Managers

Asset managers have two main options under the new rules. MiFID II allows them to either budget and pay for investment research themselves, or to pass the cost of research on to their investors by charging an additional research fee on top of execution fees.Most of the world’s biggest asset managers chose the first option: bearing the cost on investors’ behalf.

AXA Investment Managers, the French investment giant with 735 billion euros ($878 billion) in assets under management (AUM), said earlier this month that it would “fully absorb the costs associated with the external research we utilize on our clients’ behalf,” according to CEO Andrea Rossi.

Franklin Templeton Investments, which counts around $740 billion in AUM, also announced that it would pay for third-party investment research for client accounts under the MiFID II regulation.

Other large managers, including BlackRock, Deutsche Asset Management, Pimco, JPMorgan Asset Management, and Aviva Investors have all announced that they would cover the cost of investment research on behalf of their clients, according to Financial News London.

While absorbing the cost of research is a good business decision, the additional expenses could hurt the asset management industry as a whole. The bottom lines of active asset managers, who face challenges such as falling management fees and increasing preference for passive investing, were already under pressure before MiFID II. And that could cut into their profits and hurt shareholders.

“We believe that research unbundling requirements will add to AMs’ (asset managers) woes in this challenging environment,” according to a 2016 report by CRISIL, a unit of S&P. “Under our base-case scenario, operating profits of European active AMs would decline by 17 percent.”

The trend could also create a rift between the haves and have-nots of the asset management industry. With fees being such a big part of net returns to investors, the larger asset managers who have the budget to absorb more costs may have an advantage versus smaller players in the industry who may be forced to pass the costs onto clients.

Execution versus research fees. Source: PwC

No Consensus Among Banks

Unbundling requirements of MiFID II present different challenges for banks, most of which are large, publicly traded entities.Some banks have attached a price tag of $0 to research services. Dutch bank ING introduced a free research platform THINK, where “everyone will be able to freely access the best of ING’s economic and financial analysis.”

European banks such as BBVA, Credit Suisse, and NatWest have announced they will give away fixed income research for free under MiFID II.

But other banks, mainly in the United States, disagree. The group of banks opposed to giving away research “says that making research available for free could be risky and does not make commercial sense,” according to the Financial Times. They argue that explicitly assigning a price tag of zero to research—effectively achieving the same result as today—violates the spirit of MiFID II laws.

But among the banks choosing to charge clients, there is a great disparity in costs.

Barclays, the British bank, has set three levels of research service: bronze, silver, and gold. Clients of Barclays may have to pay up to 350,000 pounds ($472,000) to receive the gold tier of research from its equity analysts under the new rules, according to Bloomberg.

Swiss bank UBS plans to charge clients up to $40,000 annually to access the best equity research, said Bloomberg.

Credit Agricole, the French investment bank, proposed a 20,000 euros ($24,000) annual fee for all fixed income, commodities, and currency research, according to a presentation to prospective clients on Sept. 18.

Even if banks charge for research, there could be contraction in the industry.

“The buy side (asset managers) will pay broker-dealers for actionable research that adds investment value, but the demand will fall far short of the mountains of research that banks currently supply ‘for free,’” according to consultancy McKinsey & Co., in a study.

And as banks create separate profits and losses for their research department, along with the shareholder scrutiny that comes with being publicly traded entities, research analysts will increasingly need to eye profitability.

Christopher Leonard, a partner at law firm Akin Gump, told the International Finance Law Review earlier this year, “It’s almost inevitable that they will reduce the size of their research departments.”