Aanalysis

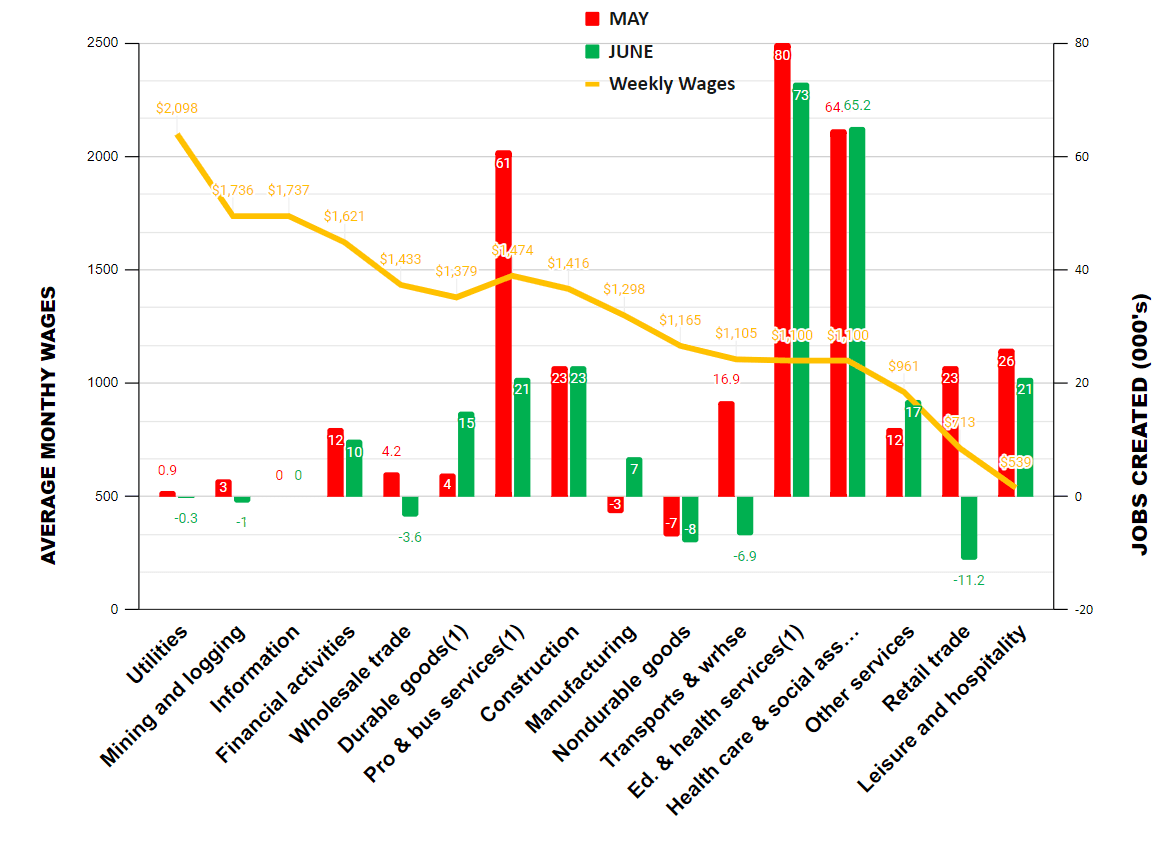

Let’s look at our exclusive schedule of Jobs Creation by Average Weekly Wages:

We saw significant month-over-month declines in jobs creation in some of the moderate wage positions, like professional and business services. That’s coupled with job losses in retail, transports, and warehousing, among other sectors. As in other recent months, government-supplemented private-sector industries like education and health services and health care and social assistance maintained robust jobs creation.

As with every quarter, we report nominal wage increases (or decreases) and how they compare to “real” wages—that is, after accounting for inflation. As with the first quarter, the second quarter showed real wages had declined in most sectors, as shown here:

![(Source: The Stuyvesant Square Consultancy, from Bureau of Labor statistics; second-quarter data comparison of nominal vs. real annual wage increases [decreases])](/_next/image?url=https%3A%2F%2Fimg.theepochtimes.com%2Fassets%2Fuploads%2F2023%2F07%2F07%2Fid5381011-Screenshot-50.png&w=1200&q=75)

Other Data Points

The Institute for Supply Management’s Purchasing Managers Index for June showed the economy contracting faster. On the other hand, the ISveM Services report showed the economy expanding faster; however, the service sectors growing fastest are in low-wage sectors like accommodation and food services, arts, entertainment, and recreation. High-wage sectors, like agriculture, forestry, fishing and hunting, mining, and information, declined.The Job Openings and Labor Turnover Survey (JOLTS) showed 496,000 fewer job openings in May than in April and 211,000 more separations.

Building permits in May, released June 20, were at a seasonally adjusted annual rate of 1,491,000. This is 5.2 percent above the revised April rate of 1,417,000, but is 12.7 percent below the May 2022 rate of 1,708,000.

Privately owned housing starts in May were at a seasonally adjusted annual rate of 1,631,000. This is 21.7 percent above the revised April estimate of 1,340,000 and is 5.7 percent above the May 2022 rate of 1,543,000.

For May, personal income and outlays, released June 30, showed disposable personal income up 0.4 percent in current dollars and 0.3 percent in chained 2012 dollars. (“Chained dollars” is a measure of inflation that takes into account changes in consumer behavior in response to changes in prices.) Personal income in current dollars was up 0.4 percent.

The Personal Consumption Expenditures (PCE) Index, excluding food and energy, reported to be the Federal Reserve’s preferred measure of inflation, printed at 4.6 percent, down slightly from April. PCE inflation, also called “headline inflation,” printed at 3.8 percent, down from April’s 4.3 percent.

Opinion

Federal Reserve Policy

The Federal Reserve’s rate pause at the policy-making Federal Open Market Committee’s June meeting was exposed as a “split decision” by the Fed minutes that were released Wednesday, notwithstanding the ultimately unanimous vote:“Some participants indicated that they favored raising the target range for the federal funds rate 25 basis points at this meeting or that they could have supported such a proposal. The participants favoring a 25 basis-point increase noted that the labor market remained very tight, momentum in economic activity had been stronger than earlier anticipated, and there were few clear signs that inflation was on a path to return to the committee’s 2 percent objective over time.”The bond market took a beating Thursday when the ADP jobs report showed 497,000 new jobs in June, versus expectations of 228,000. Anticipating another rate hike from the Fed, bonds fell and yields rose. From the Friday before the Independence Day holiday to yesterday, the yield on the 10-year jumped nearly 20 basis points (i.e., 20/100ths of a percent). That was reversed after today’s jobs numbers as shorter-term bond yields fell as their prices increased.

Today’s jobs report was disppointing and puts the Fed pause into fresh perspective. Overall, this was a disappointing jobs report and fell below market expectations, particularly after yesterday’s ADP report. The effect could be seen in the bond market where investors stepped back from their prior expectations that a Fed rate hike in July was a veritable certainty as mid-term and long-term bonds hiked and yields fell.

We'll know more when the inflation data prints next week, but it seems the economy is slowing.

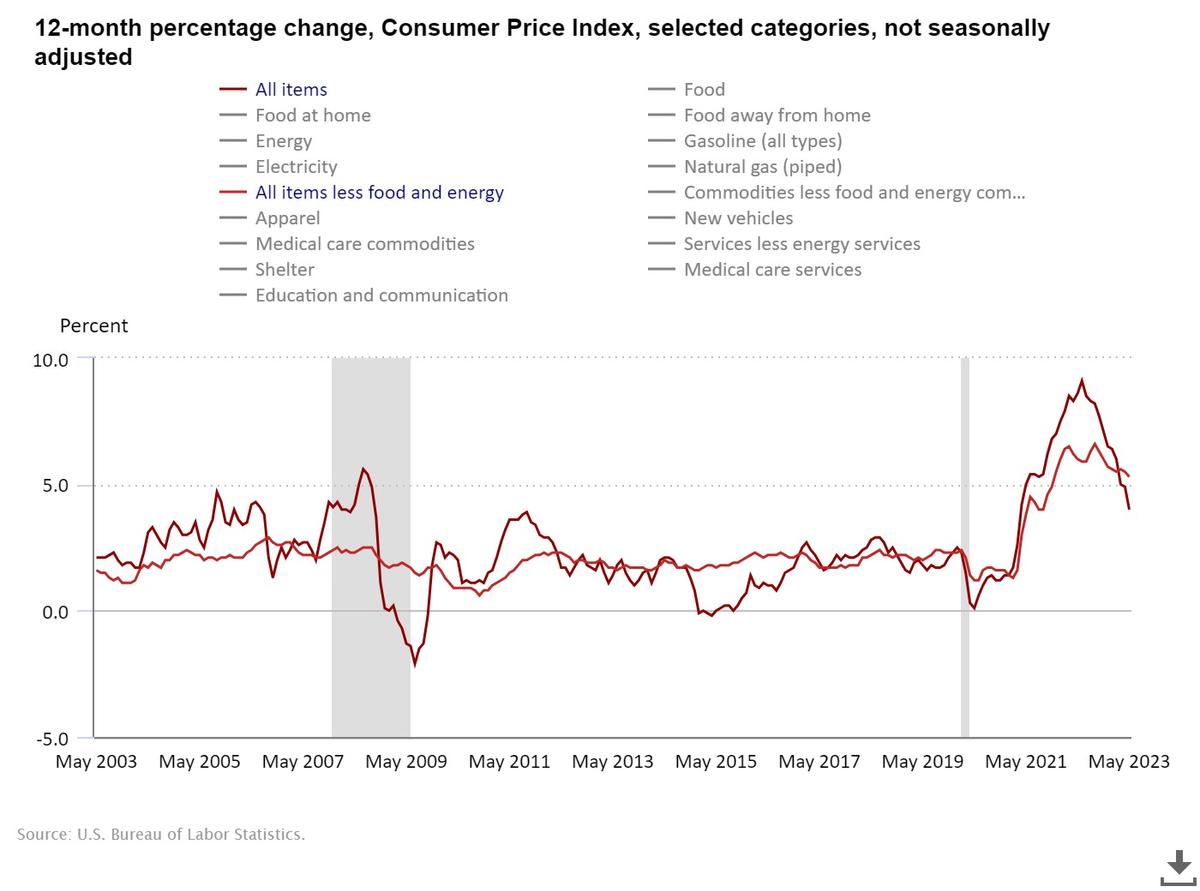

While headline inflation has moved lower since the Fed tightening, Core inflation (the lighter red line shown below) is where it was roughly 18 months ago, in December 2021, as shown in this chart:

Core inflation (which excludes food and energy prices), the Fed’s preferred measure of inflation (the lighter red line), is still running at around 5.3 percent in May that nearly mirrors the 5.5 percent rate in December 2021, 18 months ago. Fed policy has been largely ineffective in the larger economy. And while targeting a 2 percent inflation rate in the “headline” number, but preferring the “core” rate as a policy measure, may seem contradictory, but it’s actually not. Core inflation measures the broader economy and is less prone to volatility, so it speaks to the Fed’s broad-based dual mandates to provide “stable prices” and “full employment.”

Barring some unexpected change in the next inflation release next Wednesday, we expect another divided Fed will likely stand pat in its July meeting later this month and await further data. But we expect rates will hike a quarter to one-half percent when the Fed meets again in September because we don’t see core inflation declining much by then. That will make it tougher on small and medium-sized businesses that are already seeing tougher credit and lending standards. As we have said since this bout of inflation started, we expect the terminal rate to top out closer to 6 percent.

We continue to prefer a sharper reduction in the Fed balance sheet, which is, today, roughly where it was in February. (It expanded, briefly, after the Silicon Valley Bank fiasco that was, in its own right, caused by Fed rates hikes and grossly mismanagement and inept oversight by, respectively, SVB and the reglators from the Federal Reserve Bank of San Francisco.)