This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

A house provides shelter, comfort, and security—and when lived in long enough, it can become a home.

And for most Americans, houses are also the most valuable asset they possess, according to a 2024 Federal Reserve report. Home equity provides a lasting source of wealth that they can pass on to their children.

But are houses a good investment?

A June 9 study by Bankrate suggests that they might not be as lucrative an investment as they are thought to be. Many people look at the difference between the purchase price of a house and its sale price as profit, but there is a lot more to the equation.

“There’s so much more that goes into it, and many homeowners are failing to look at the higher costs of homeownership, which is what we call the hidden costs,” Bankrate home lending expert Linda Bell, author of the report, told The Epoch Times. “It catches many homeowners off guard.”

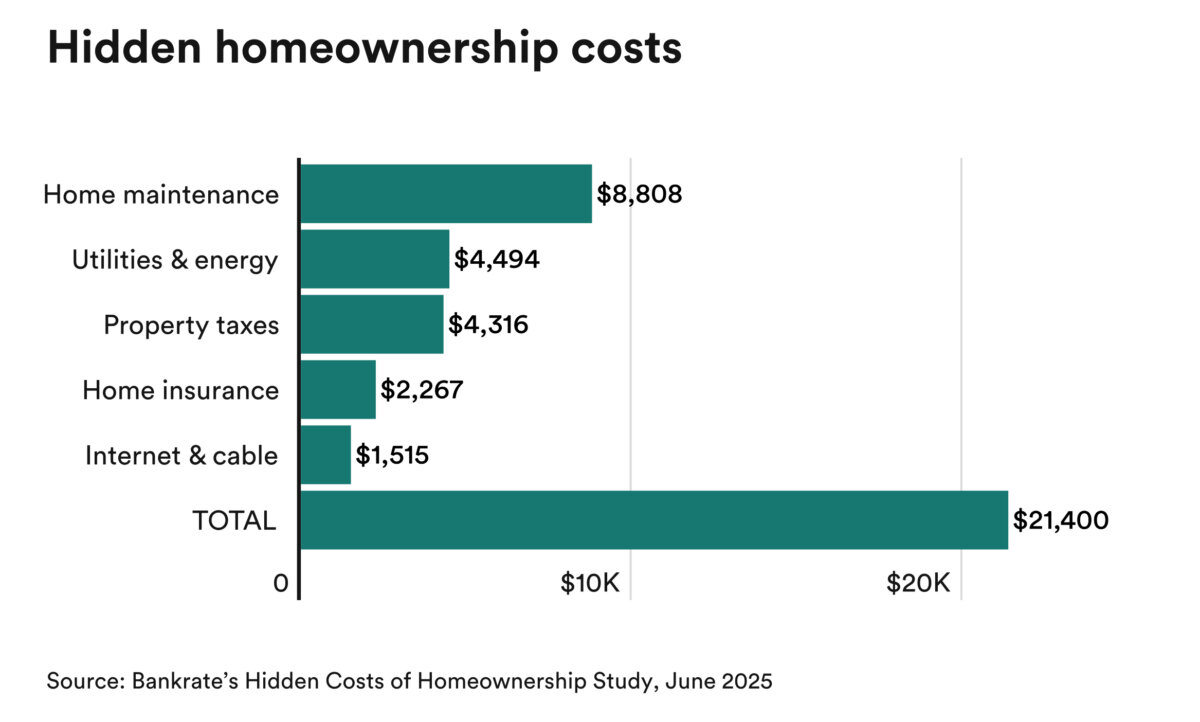

Bell calculated that the average American homeowner pays more than $21,000 a year, including property taxes, insurance, maintenance, repairs, and utilities. And while about $6,000 of this number is attributed to expenses such as water, heat, electricity, and internet service, which renters would also typically have to pay, the remaining $15,000 is the additional annual cost specific to homeownership.

The average annual costs include approximately $8,800 for property taxes, $4,300 for taxes, and $2,300 for homeowners’ insurance, though these costs vary significantly depending on location. The most expensive states for these expenses are Hawaii ($34,573), California ($32,262), New Jersey ($29,751), Massachusetts ($29,277), and Washington ($27,444). The lowest cost states for homeowners are West Virginia ($12,579), Mississippi ($14,810), Indiana ($14,903), Missouri ($15,349), and Arkansas ($15,362).

These costs are rising, both as measured in dollars and as a share of income.

Inflation in the cost of maintenance, repairs, materials, and labor costs, Bell said, “is here to stay, and it just keeps increasing.”

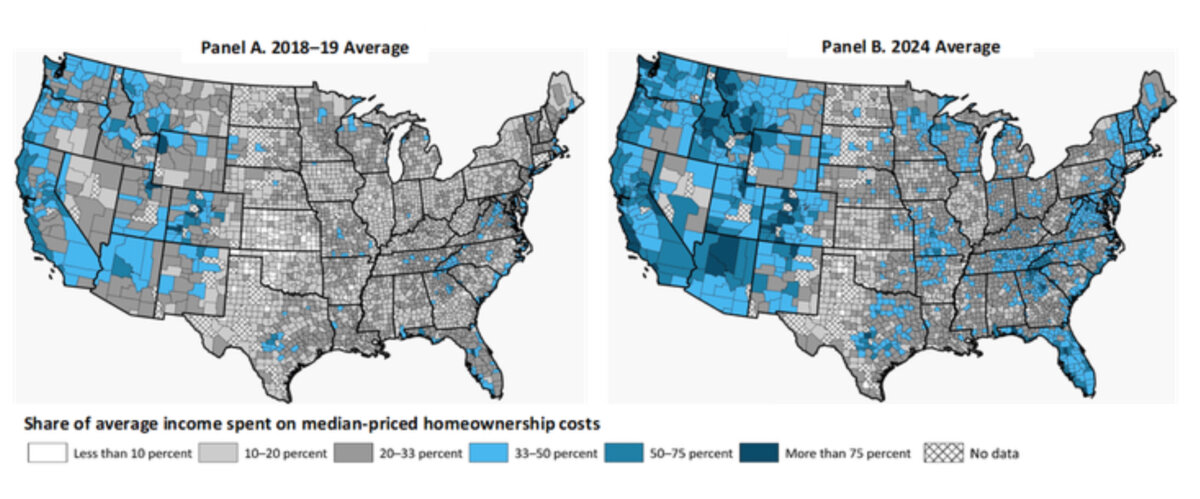

A January report by the Federal Reserve found that “new homeownership became less affordable across much of the United States over the last five years,” noting that the cost of owning a home, including taxes, maintenance, and repairs, now accounts for about one-third of the average American’s spending.

Between 2019 and 2024, the percentage of income needed to buy and maintain a median-priced home rose in most U.S. counties, the report states. This is indicated in the “drastic shift” from what had been affordable counties (white and gray) to unaffordable counties (blue and dark blue) during this period.

In these maps, gray regions indicate more affordable homeownership, taking all costs into account; blue regions are less affordable. (Source: Federal Reserve)“The decline in new home affordability for the average household was most pronounced in the western United States, coastal markets, and parts of the Southeast,” the Fed report states. “However, even counties in the central United States—for example, in Missouri, Texas, and Minnesota—experienced declines in affordability.”

The increasing cost of homeownership challenges long-held beliefs about the value of buying a house, compared to alternatives.

According to market data collected by New York University economist Aswath Damodaran, stocks in the S&P 500 Index returned an average of 9.94 percent between 1928 and 2024, which includes the stock market crash of 1929–31, compared with 4.23 percent for real estate. Over the past decade, the gap is even wider: 12.98 percent for stocks versus 6.89 percent for real estate.

This difference also corresponds with a growing gap between the bottom 90 percent of American households, for whom houses are the largest assets, compared to the top 10 percent, who have a greater share of their savings invested in stocks.

But this does not necessarily mean that buying a home is a bad investment. There are many benefits to owning the house you live in.

“Homeowners were wealthier than renters,” a 2022 “Wealth of Households” study by the Census Bureau stated. “Households that owned their home had a median wealth about 44 times larger than those that rented.”

Even excluding the value of home equity from total wealth, the study found that the median wealth of homeowner households was approximately 17 times more than that of the median renter household.

Buying a home, particularly when financed by a mortgage, can impose financial discipline on buyers, who must manage their income and spending to ensure they can make the monthly payment. It is a form of forced savings—at the risk of losing your home to foreclosure. By contrast to rent payments, a portion of each mortgage payment goes to build up equity in the home, and there are also tax deductions for the mortgage interest expense and tax breaks on profits when selling a house, if it is your primary residence.

For those who are considering buying a house, however, analysts caution that all potential costs should be taken into account, not just the purchase price and monthly mortgage payment.

“The first thing they need to do is crunch the numbers and make sure they can afford it, because I’ve written many articles about people ending up ‘house poor,’” Bell said. “There are a lot of aging homes out there, homes that are 40-plus years old, and they may need things like an HVAC system, a new roof, or just general routine maintenance.”

There is also the cost of replacing appliances—refrigerators, washing machines, washer/dryers, and stoves—and she recommends having an emergency fund set aside to cover the inevitable but often unexpected costs of maintenance and repairs.

“One to 4 percent of your home’s value is what you should be saving in that emergency fund,” Bell said. “And save that money in a high-yield savings account so your money is working better for you than your typical bank or savings account.”

For new homes or renovations, many builders will provide a home warranty that will cover things such as windows, heating, ventilation and air conditioning (HVAC), plumbing, and electrical systems, typically for the first one to two years, according to the Federal Trade Commission. For major structural defects, warranties can go out to 10 years.