This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

Printing Supervisor Donavan Elliott inspects newly printed sheets of one dollar bills at the Bureau of Engraving and Printing in Washington on March 24, 2015. Mark Wilson/Getty Images

As the Senate passed its own version of the “One Big Beautiful” budget bill, the effect of tax and spending cuts in the House version has led the Congressional Budget Office to project a $2.4 trillion increase in the federal deficit by 2034.

While there is debate among economists regarding these figures and whether tax cuts could increase government revenue by sparking higher growth, some have suggested that the apparent indifference toward deficits in pending budget legislation is reminiscent of modern monetary theory (MMT), which argues that deficits are not inherently a problem, and which found support with many Democrats in their efforts to spend trillions on climate and social justice programs.

“The [budget bill] may resemble MMT in practice—massive deficit spending without serious regard for fiscal sustainability—but that’s not by design,” Romina Boccia, director of budget policy at the Cato Institute, told The Epoch Times.

“The real problem is that both parties are acting as if deficits don’t matter—whether they believe in MMT or not,” she said. “Such behavior is dangerous because it normalizes borrowing to finance everyday government operations, without leaving fiscal space for inevitable shocks or downturns.”

GOP representatives in the House Freedom Caucus have criticized the Senate’s version of the bill, stating on X that “the House budget framework was clear: no new deficit spending in the One Big Beautiful Bill.”

The Senate’s version, they stated, will add $651 billion to the deficit, before interest expenses.

“That’s not fiscal responsibility,” they wrote. “It’s not what we agreed to.”

However, even the House version is projected to increase the deficit due to revenue reduction of $3.7 trillion, compared to spending cuts of $1.3 trillion, over the 2025–2034 period, the CBO states.

Meanwhile, President Donald Trump has called for the federal debt ceiling to be eliminated.

“I am very pleased to announce that, after all of these years, I agree with Senator Elizabeth Warren on SOMETHING,” he posted on Truth Social on June 4. “The Debt Limit should be entirely scrapped to prevent an Economic catastrophe.”

Sen. Warren (D-Mass.) supported eliminating the debt limit, but said it shouldn’t be done to “fund more tax breaks for billionaires.”

Many on the left were comfortable with deficits that arise from new spending during the Biden administration, and many on the right now seem to find them acceptable if they arise from tax cuts. And between them are proponents of MMT, who say that despite the vehement objections of mainstream economists, deficits may not be a problem at all.

Spending by Printing Dollars

Modern monetary theory is based on the idea that government spending, in countries like the United States that issue their own fiat currencies, is not limited by what the government can tax or borrow because it can print as much money as it wants to.

One of the early advocates and developer of MMT, hedge fund manager Warren Mosler, stated that “the government doesn’t need your dollars to be able to spend.”

Statements from those who set America’s monetary policy appear to support this view.

As the government pumped trillions of dollars into the banking system in response to the mortgage crisis, then-Federal Reserve chair Ben Bernanke stated during a “60 Minutes” interview in 2009 that the government didn’t need to raise taxes to make those payments.

“We simply use the computer to mark up the size of the account that they [banks] have with the Fed,” Bernanke said.

Turning traditional economics on its head, Mosler argues that the government spends by creating dollars. And when the government collects taxes, it doesn’t spend those dollars; it eliminates them.

“According to MMT, all dollars are spent into existence by the federal government first, and taxed out of existence later,” a Georgetown University report by Alec Bowman states. “When the federal government taxes dollars, it does not collect them—it destroys them.”

The effective limit on government spending, therefore, is not how much the government can tax or borrow; it is the extent to which creating dollars causes inflation.

Far from being a problem, deficit spending is a good thing, according to MMT, because it creates a surplus of dollars in the private sector, which allows savings and investment throughout the economy. A deficit, they argue, means the government is putting more dollars into the economy than it takes out in taxes; a surplus means the government is taking dollars out of the economy.

Further, as Bard College economist Randall Wray stated in a 2025 position paper, the current $36 trillion in federal debt is not necessarily a problem either. Because governments like the United States, Japan, and the United Kingdom can spend by crediting bank accounts, issuing bonds is merely an alternative option, which takes excess cash out of circulation and allows holders of their currency to earn interest.

“The government could at any time stop issuing new sovereign debt and simply leave more excess [bank] reserves in the system,” Wray writes. “One can think of sovereign debt as nothing more complicated than reserves that pay a higher interest rate.”

Advocates of MMT point to Japan, whose government debt has steadily increased since the 1990s to about 200 percent of its GDP today, but where the inflation rate has remained low, often negative, for decades, though recently it has risen above 3 percent.

A ‘Reckless Fiscal Policy’

Many economists, however, have been highly critical of MMT, citing deficit spending as a key driver of accelerating inflation under the Biden administration.

“MMT is neither valid nor a coherent theory; it’s a dangerous justification for reckless fiscal policy,” Boccia said. “It ignores basic economic principles of scarcity and trade-offs and falsely assumes that inflation can be easily managed after the fact.

“History offers plenty of cautionary tales—from Argentina to Zimbabwe—about what happens when governments try to print their way out of budget constraints,” she said. “In reality, unchecked deficit spending leads to inflation, loss of investor confidence, and economic instability.”

The current level of government deficits will either result in inflation or an unsustainable debt burden, economists say, depending on how the government funds them.

“There are only two ways you can finance a deficit,” Steve Hanke, economics professor at Johns Hopkins University who served on President Ronald Reagan’s Council of Economic Advisers, told The Epoch Times. “One way is to sell bonds to the non-bank public.”

This method, in which the public finances the deficit, increases the government’s debt payments, but decreases the money supply by taking cash out of people’s checking accounts to buy the bonds. This was an approach the United States used during World War II, combined with tax increases, in order to keep demand and inflation down as the country’s production shifted from consumer to military goods.

The other way to finance America’s deficit is that the Fed buys the Treasury securities, which it did by the trillions following the 2008 mortgage crisis and the 2020 pandemic. In this case, the Fed credits bank accounts with dollars in exchange for the Treasurys, thereby increasing the money supply.

“The perfect example of that option was COVID,” Hanke said.

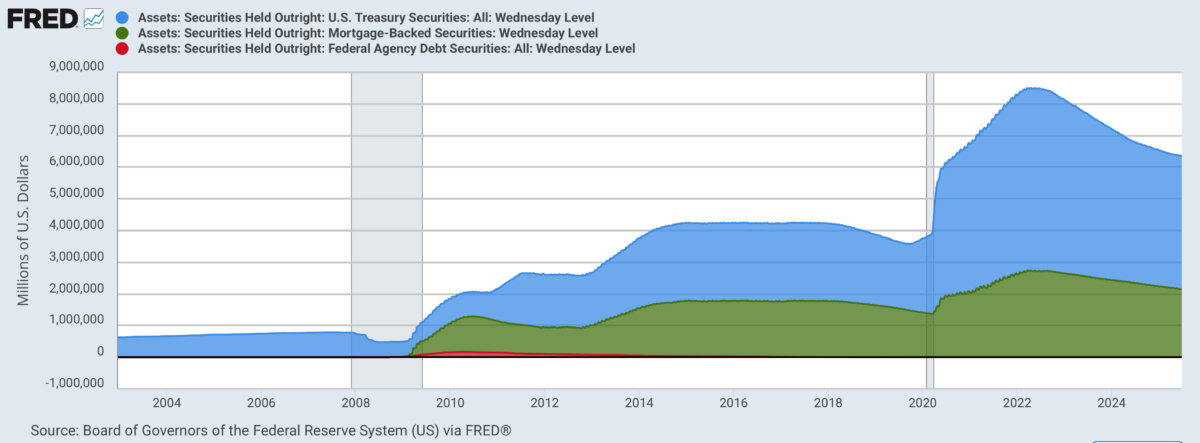

(Source: Federal Reserve)

In the wake of unprecedented government spending following the coronavirus pandemic, during which the Federal Reserve more than doubled its holdings of bonds, from about $4 trillion to $9 trillion, consumer prices in America accelerated to a rate of 9 percent in 2022, wiping out more than 20 percent of the dollar’s value by 2024. And while MMT advocates point to supply-chain disruptions as the cause of that inflation, other economists argue that even when supply chains returned to normal levels, prices did not come back down.

This experience has undermined many of the proponents of MMT, particularly those who argued that the risk of budget deficits should not limit America’s spending on programs like the Green New Deal and Medicare-for-all.

“They were riding very high for a while,” Hanke said. “They’ve kind of retreated into the shadows now, but they’re not gone.

“Their crackpot theories never hold water, but they remain around the fringes nevertheless,” he said.

The Fed Steps Back as Debt Increases

As the coronavirus crisis receded, the Fed began to reverse its dollar-printing policy, which it called “quantitative easing.” Over the past several years, the Fed has been shrinking its balance sheet, reducing its holdings of U.S. Treasury securities from a peak of $5.7 trillion in 2022 to approximately $4.2 trillion today.

Meanwhile, the federal debt has increased from less than $10 trillion in 2008 to more than $36 trillion today.

On May 16, credit-rating agency Moody’s joined peers Standard & Poor’s and Fitch in downgrading America’s debt from its highest rating of Aaa to Aa1, on the grounds that “successive U.S. administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs … persistent, large fiscal deficits will drive the government’s debt and interest burden higher.”

Of America’s outstanding debt, 20 percent is intra-governmental, held by public entities like the Social Security trust funds, according to the Peter G. Peterson Foundation. Of the debt that is classified as “debt held by the public” (DHBP), two-thirds is owned by Americans, with the largest single holder of Treasury securities being the Federal Reserve, which currently holds more than $4 trillion of them.

The largest foreign owner of DHBP is Japan, which owns more than $1 trillion in Treasury bonds and notes. China and the United Kingdom are the second largest, each owning about $700 billion.

There is no risk of the U.S. government defaulting on its debt, however, given its ability to print more dollars, Wray argues, unless it does so voluntarily through government shutdowns or Congress enforcing a debt limit on the Treasury Department. The rating agencies are simply wrong, he states.

But others say current deficit and debt levels are unsustainable.

“A $2 trillion annual deficit—particularly in a time of low unemployment and relative peace—is a flashing red warning sign,” Boccia said. “It’s the structural nature of the deficit that makes it so concerning.

“This isn’t temporary stimulus; it’s a baked-in mismatch between entitlement promises and government revenues,” she said. “Sustaining such large deficits year after year risks triggering a debt crisis, especially if interest rates rise or foreign demand for U.S. debt weakens.”

Interest payments on the federal debt are projected to be $665 billion in 2025, according to the Peter G. Peterson Foundation.

“Interest costs so far in fiscal year 2025 are the third-largest spending category for the federal government—outpacing outlays for all budget functions other than Social Security and Medicare,” the foundation states; and by the end of this year, interest payments will likely exceed Medicare.