This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

Sarah Turner of West Maui fills containers with gasoline to power her emergency generators and help her neighbors who need fuel, on Aug. 16, 2023. Allan Stein/The Epoch Times

The August U.S. inflation numbers that were released on Sept. 13 should concern consumers as headline inflation continues to inch upward, printing at 3.7 percent, exceeding expectations, and defying the efforts of the Federal Reserve to contain it. Core inflation, which excludes the cost of food and fuel, dropped slightly but still printed at 4.3 percent.

Since inflation compounds, and is cumulative, Americans are now paying about 17 percent more than they did when the Biden administration first pronounced the most recent bout of inflation to be “transitory.”

We have long said that the principal cause of the current inflation is the enormous size of the Fed’s balance sheet, exacerbated by federal spending. As we look at a now $7 trillion federal budget and record $2 trillion deficits as far as the eye can see, it’s clear the Fed balance sheet won’t be shrinking sufficiently or rapidly enough to arrest the inflation we are suffering.

But it is likely to get worse.

Saudi Arabia and other OPEC+ countries (i.e., OPEC members and their allies) are determined to boost the price of oil and are restricting production. Saudi Arabia has cut its production by 1 million barrels per day and will continue to do so through the end of the year. Russia, an OPEC+ ally, has cut production by 300,000 barrels per day.

Accordingly, we can expect so-called “headline inflation,” which includes food and fuel, to print higher in the coming months.

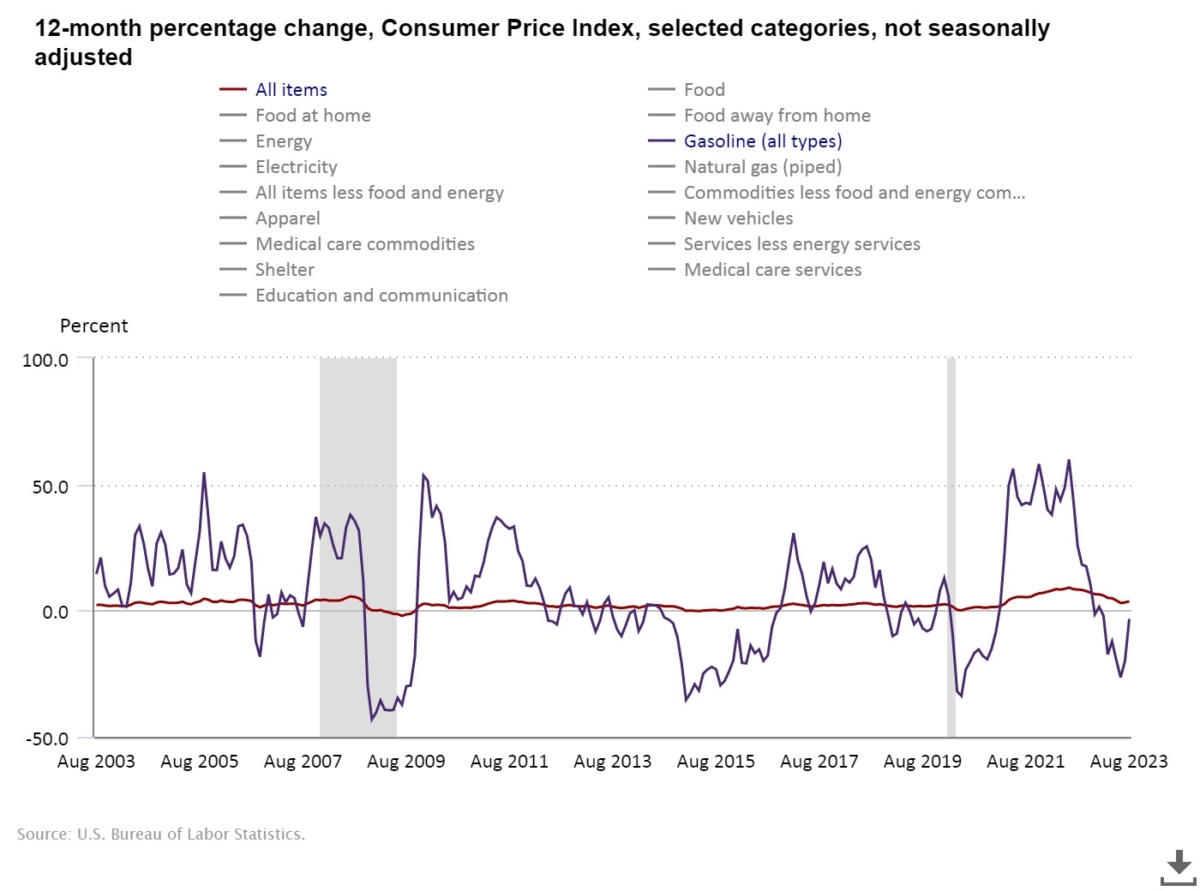

It should be noted, too, that while “core inflation” was reduced, much of it came largely from the reduction in the cost of gasoline, as shown in the purple line on this chart (the red line is “all items” inflation).

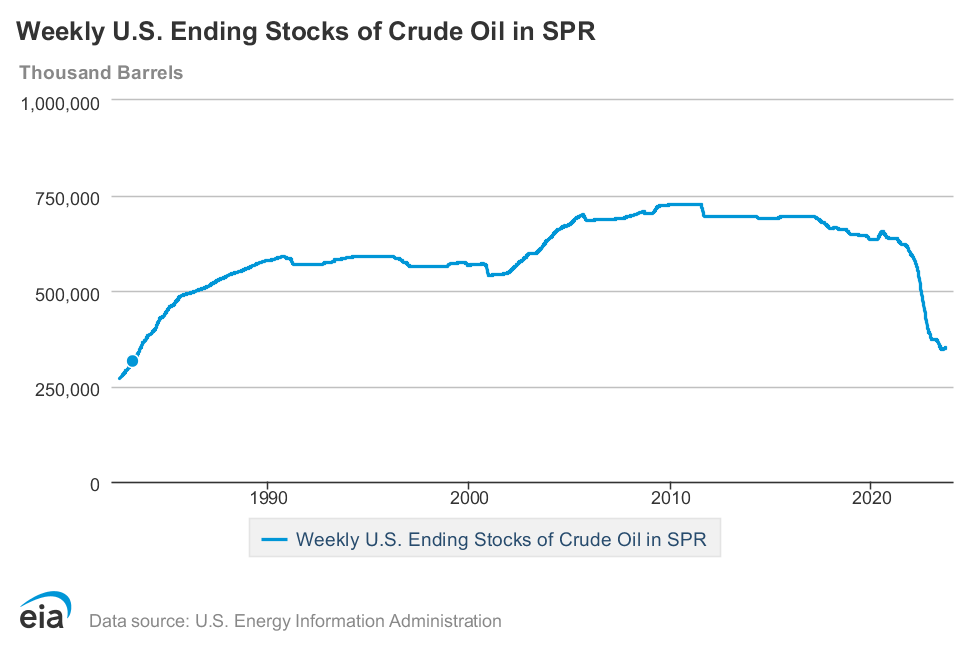

But much of that is attributable to tapping the Strategic Petroleum Reserve, which is now at its lowest point in 40 years, with an economy that is now three times the value it was then in real (i.e., 2012 dollars) terms.

Draining the SPR is a “one-shot” inflation strategy. It might be continued, but only at an increased cost for replenishing the SPR and at no small risk to national security, should some aggressor wage war against us or threaten our fuel supply lines. But, ultimately, it’s an inflation strategy with no exit strategy.

It’s notable that the most recent disposable income figures declined in real terms in July, the most recently available data point, and that real per capita disposable income has increased by less than $800 in the 42 months since February 2020, less than 2 percent since the pandemic commenced. But in the 42 months prior to the pandemic, real disposable personal income had increased over 9 percent, from $41,791 to $45,708.

The consumer, already struggling, is likely to face additional challenges, not only from inflation but from the renewal of student debt repayments. The Federal Reserve meeting next week could reasonably be expected to result in another quarter-point interest rate increase as well, further squeezing consumers and businesses.

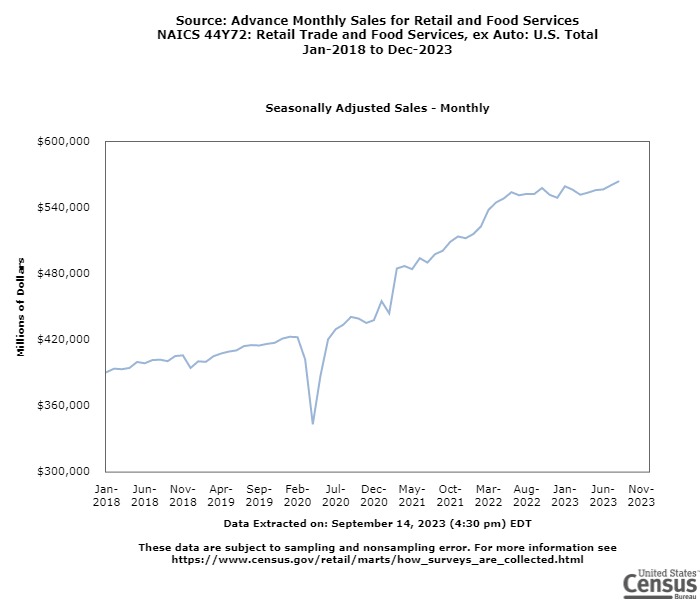

We see all this as creating, ultimately, a cascading negative effect on retail sales (excluding automobiles), which has already proven to be largely flat since last June, as illustrated here.

Summary

Absent the generous federal stimulus from the pandemic, Americans are now being squeezed and will continue to be, even more so, by rising energy costs, higher interest rates, and soon-to-resume student loan repayments. Consumers’ free cash, especially among the young people most inclined toward spending on consumer durables and housing, will doubtlessly slow retail sales further.

All of this spells a tough fourth quarter, especially for consumer discretionaries, and, likely, a recession going into the first quarter of 2024.

J.G. Collins is managing director of the Stuyvesant Square Consultancy, a strategic advisory, market survey, and consulting firm in New York. His writings on economics, trade, politics, and public policy have appeared in Forbes, the New York Post, Crain’s New York Business, The Hill, The American Conservative, and other publications.