The immediate effect of the better-than-expected jobs report was to drop bond prices and increase yields in anticipation that the Federal Reserve will not cut interest rates as soon as many had anticipated. But as the market digested the report, market sentiment was discrepant. A firmer direction may be found next Thursday when December’s Consumer Price Index (CPI) is released.

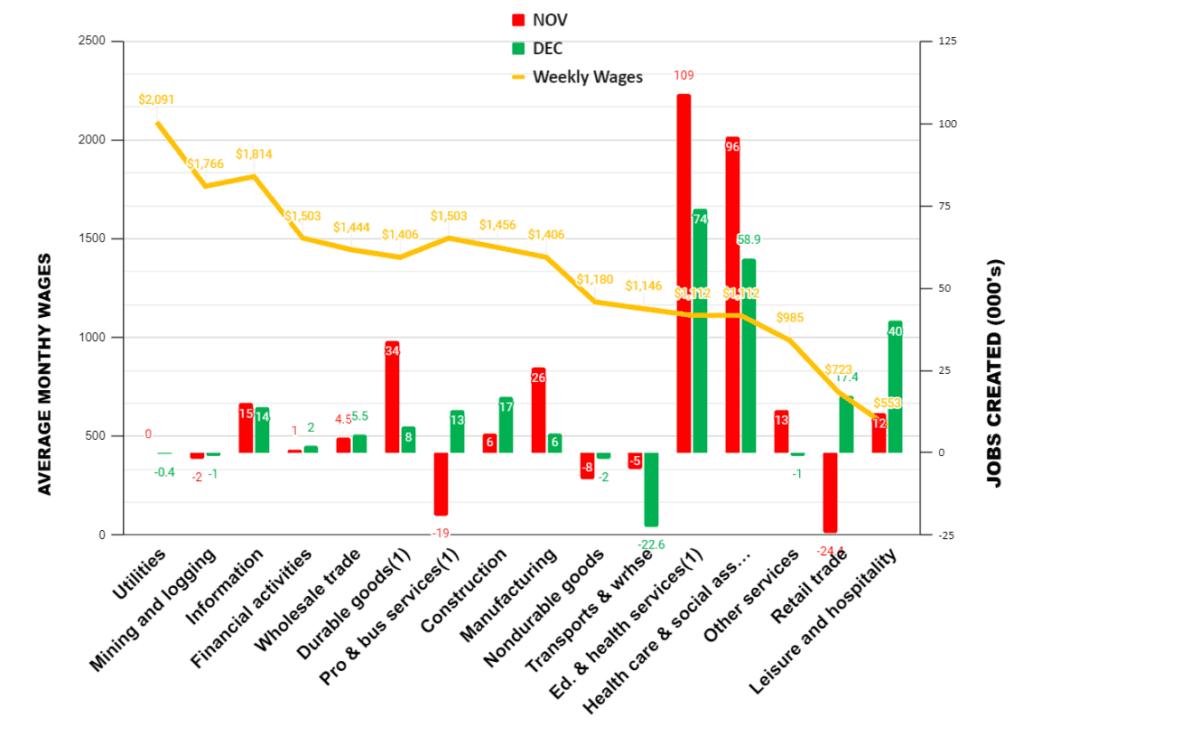

Let’s look at our exclusive schedule of jobs creation by average weekly wages:

As we have seen a good deal of late, most of the jobs created are in the largely government-supported education and health services, which includes health care and social assistance. The next highest was in the low-wage leisure and hospitality sector. Notably, too, although not evident in the schedule, is that temporary help services, an element of professional and business services, cut some 33,000 jobs. Temporary workers are almost always the first to lose their jobs when the economy slows. (We do not show government jobs in our schedule.)

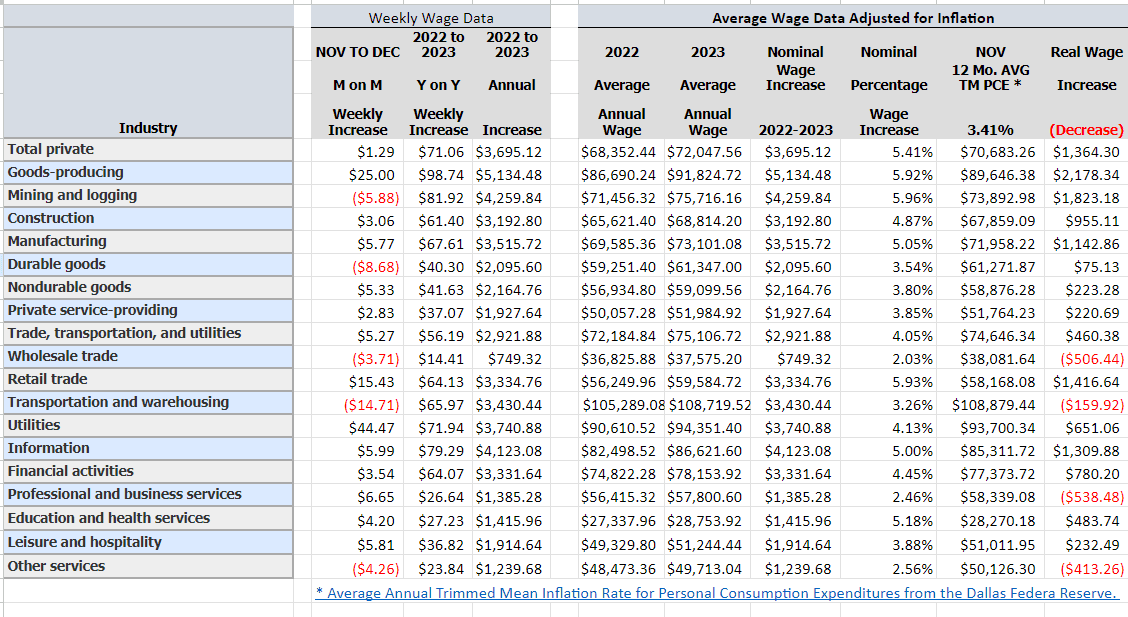

As per our usual practice, we include our quarterly summary of nominal and real wages for the fourth quarter:

Opinion and Analysis

Today’s jobs numbers likely disabuse many that the Fed will cut rates, at least in the first half of 2024. That’s a good thing. By rights, the Fed should be boosting rates and tightening the amount of money in the economy. But this is an election year. Silicon Valley Bank, early last year, was the prototype of what can happen when the Fed escalates rates. And—by the way—the Fed governors are none too fond of Donald Trump, as a former governor made explicit in 2019.We just passed the $34 trillion mark of the U.S. economy. We could add another trillion to debt by March. The debt is over 120 percent of our GDP. Our interest payments alone are approaching $1 trillion a year, and are—already—the largest single line item of the budget.

Imagine, for a moment, that your household debt, excluding your mortgage, was 120 percent of your annual income. And that your spending every year exceed your income by over 7 percent, as it is for the United States.

If we assume the average U.S. wage is around $60,000 a year, that would mean your total debt would be $72,000, and, at even around 5 percent, your interest payments alone, without principal, would be 6 percent of your gross income, $3,600 a year. Now, assume you’re accumulating debt, over and above interest, every year at $4,200 a year—the same as the percentage rate of U.S. deficit spending right now. You would need another job just to meet your debt obligations. And you'd probably opt for bankruptcy.

When governments have excessive debt, they have three choices: cut spending, raise taxes, or debase the currency. It’s fairly clear Washington can’t muster the political courage to do the first two options. And we saw with the Fed’s failure to raise rates even a quarter point in its last few meetings that it will enable the fiscal dereliction, especially going into an election year, when the Fed board of governors clearly have a preferred candidate in the 2024 election.

Back in August 2019, William Dudley, former president of the Federal Reserve Bank of New York, went so far as to urge his former colleagues to not cut rates as, in Mr. Dudley’s view, it would “enable the Trump administration.” He wrote in Bloomberg, “Fed officials’ desire to remain apolitical” is “untenable.”

I suspect the Fed will stand pat (or even reduce) rates in anticipation of the November elections. I suspect that Congress will adopt another continuing resolution to continue spending before its prior one expires on Jan. 19. I don’t see Washington unwilling to make serious budget cuts or to raise taxes. So, the remaining course of action is inflation: debasing the currency. They’ve managed to do that by 17–20 percent in the last three years.

As I wrote, our trading partners are seeing it and moving to de-dollarize their economies because they are, perhaps, more aware of American fiscal hubris and irresponsibility that Americans are.

December Other Data Points

The Institute for Supply Management Manufacturing Purchasing Managers Index (PMI) for December showed the industrial economy is contracting more slowly than last month, at 47.4 (A reading below 50 signals contraction.) It is the fourteenth consecutive month of contraction.On the other hand, the ISM Services Index for November showed the service economy expanding, slightly more quickly, in a 11-month trend.

The Job Openings and Labor Turnover Survey for November, released Jan. 3, declined, with 62,000 fewer jobs openings in October than in September. Total separations decreased by 292,000.

Building permits in November, released Dec. 19, a seasonally adjusted annual rate of 1,460,000. This is 2.5 percent below the revised October rate of 1,498,000, but is 4.1 percent above the November 2022 rate of 1,402,000.

Privately owned housing starts in November were at a seasonally adjusted annual rate of 1,560,000. This is 14.8 percent above the revised October estimate of 1,359,000 and is 9.3 percent above the November 2022 rate of 1,427,000.

For November, personal income and outlays, released Dec. 22, showed disposable personal income up 0.4 percent in current dollars and the same amount in chained 2017 dollars. (“Chained dollars” is a measure of inflation that takes into account changes in consumer behavior in response to changes in prices.) Personal income in current dollars was also up 0.4 percent.

The November Personal Consumption Expenditures (PCE) Index from a year ago, excluding food and energy, released the same day, and reported to be the Federal Reserve’s preferred measure of inflation, printed at 3.2 percent. PCE inflation, also called “headline inflation,” printed at 2.6 percent.

The RCM/TIPP Economic Optimism Index (previously the IBD/TIPP Economic Optimism Index) fell 12.3 percent in December, to 34.3. Half of the survey’s respondents believe we are already in a recession, according to TIPP CEO and pollster Raghavan Mayur.