In the full panoply of the Biden administration’s foreign policy errors and gaffes, perhaps none was so stupid as its failed attempt to weaponize the dollar—the world’s reserve currency—against Russia for its invasion of Ukraine.

It’s telling that during World War II, neither the United States nor the UK—when the British pound sterling was the world’s reserve currency—ever considered weaponizing their currencies against Germany, Japan, or Italy. But wiser heads were running the allied nations then.

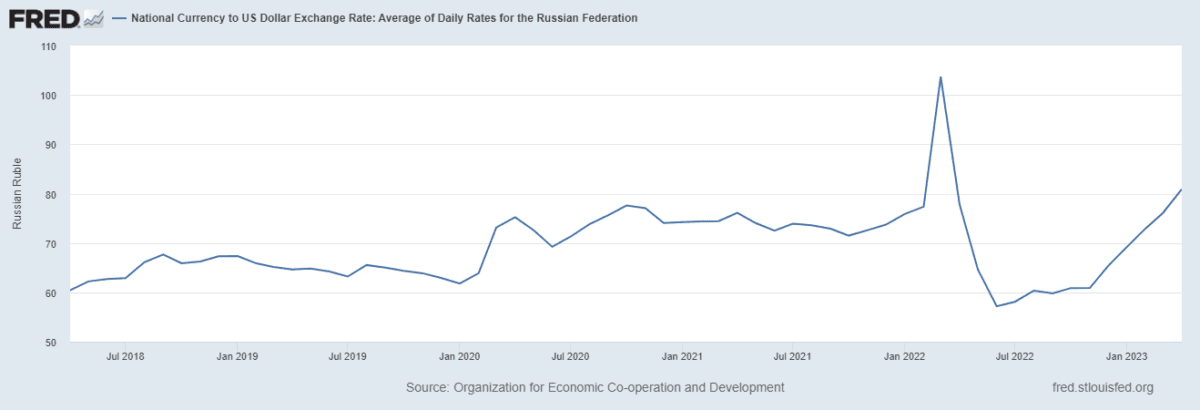

But President Joe Biden and Secretary of State Antony Blinken, along with Treasury Secretary Janet Yellen, did exactly that. And they lost. In the immediate aftermath of the Russian invasion, the ruble fell, as expected. But then for much of last year, the ruble actually gained strength relative to the dollar—stronger than it had been before the invasion!

It has only declined again since the winter, after Russian battlefield setbacks in the Donbas and the mutiny of the Russian mercenary Wagner Group.

Hitting the USA Like a Ton of BRICS

In August, the BRICS countries—Brazil, Russia, India, China, and South Africa—will meet in Johannesburg, and “de-dollarizing” the global economy is on the summit agenda. While nobody expects the dollar to be displaced anytime soon, the rise of digital currencies—and particularly central bank digital currencies (CBDC)—will make it much easier to bypass U.S. Treasury and SWIFT (Society for Worldwide Interbank Financial Telecommunication sanctions, the incumbent means of transferring funds globally) sanctions. At least one study states that this could be achieved, given CBDCs and other blockchain alternatives:

2 Ways: ‘Gradually, Then Suddenly’

Ernest Hemingway’s quote about how one goes bankrupt—“gradually, then suddenly”—seems apt given the rapidity with which de-dollarization has been occurring since the Biden administration imposed its dollar sanctions on Russia.While there was talk of de-dollarizing for years, geopolitical and U.S. domestic factors over the past nine months have exacerbated it.

First, obviously, sanctioning Russia last year using the dollar and SWIFT has led countries that are less closely aligned with the United States to consider alternatives to the dollar. Then, in October 2022, Brazil’s left-wing president, Luiz Inácio Lula da Silva, who has sought closer ties to China, won a narrow victory (by less than 2 percentage points) over conservative incumbent President Jair Messias Bolsonaro. Then, in November 2022, U.S. elections delivered a Congress narrowly divided between the two major parties. Finally, in January, the failure of the U.S. House of Representatives to promptly elect a House speaker showed how divided America is not only between the two major parties but even within the majority House Republican party.

Given the circumstances, several transactions were announced in the first half of 2023 that sought to de-dollarize several bilateral and regional trading arrangements that have traditionally been conducted in dollars:

To Lead the World, Lead the World

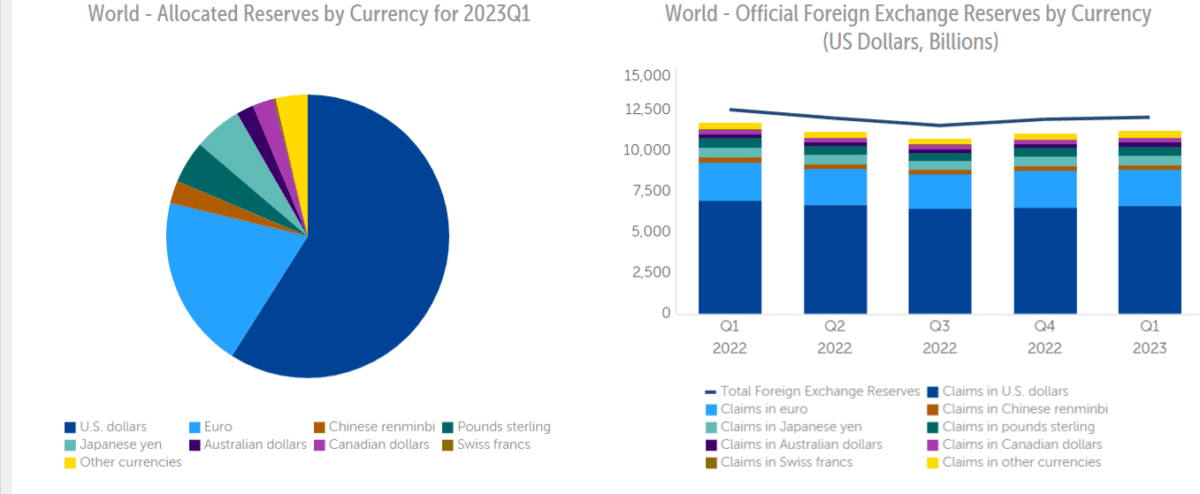

It’s unlikely that China, local and bilateral agreements, or even a new currency will supersede the dollar as the world’s reserve currency anytime soon. Global reserves are denominated overwhelmingly in dollars for the time being. That’s because our markets are far larger and better regulated than virtually anywhere else in the world. The dollar is seen as “safe,” relative to other currencies.

Moreover, our per capita gross domestic product is far greater than almost any other major economy, although China’s economy is expected to eclipse the United States in pure dollar terms because of its larger population.

Summary

We’ve been reckless in our money printing and deficit spending, and our leaders have also failed to create a single, unified set of budgetary priorities to which both parties can more readily agree. All that makes the dollar, over the long term, a riskier bet for other nations to hold as a reserve. So “de-dollarizing” their transactions can serve their interests.Cartoonist Walt Kelly, creator of the long-running “Pogo” comic strip, wrote, “We have met the enemy, and he is us.” Kelly was talking about climate risk on the first Earth Day. But his comments are equally applicable to the U.S. fiscal and monetary situation. Our deep political divisions, our chronic inability to live within our means, and our reckless tendencies to write checks and make commitments overseas that we can’t cover and can’t meet are the biggest enemy of the dollar’s fiscal integrity and its utility as the world’s reserve currency.

But Americans need to do more than that.

Just as we’ve sworn off the use of poison gas and biological weapons on the battlefield, we must also forever foreswear “weaponizing” the dollar against our enemies and our adversaries. We can certainly embargo critical materials, as we did with oil with Japan when it invaded Indochina in 1941. We can certainly freeze U.S.-based foreign assets of offending nations, as we did with Iran after it seized the U.S. embassy in Tehran in 1979.

However, the “unprecedented and expansive” currency and banking sanctions the Biden administration proudly imposed on Russia over Ukraine created a greater threat to the world’s confidence in the dollar as a reliable reserve currency than an impediment to the Russian war machine.

We should never repeat doing so again, absent total war with an enemy.