This morning’s jobs numbers fed the bond bulls, printing at 150,000 new jobs, significantly below the consensus market expectations of 180,000. Revisions, once again, were revised down by a net 101,000 jobs, largely offsetting the net 139,000 more jobs that were claimed for July and August in last month’s jobs report. Government added another 51,000 jobs, included in the 150,000 number. (Oddly, it is the third month in a row that government has added that same number of jobs.)

The unemployment rate printed at 3.9 percent, up slightly from last month. But the labor force rate declined slightly to 62.7 percent. The Household Survey, which is a poll to estimate the number of people employed, as opposed to the number of jobs created, estimated the number of people employed had fallen by 348,000.

This morning’s release triggered what we believe to be a sanguine view of the economy, and particularly of Federal Reserve policy, with markets expecting a continuing pause of Fed rate hikes or even a rate cut within some reasonably short time frame. As rates on the 10-year Treasury and other rates declined, equities rose, with the Dow Jones Industrial Average up 300 points at this writing.

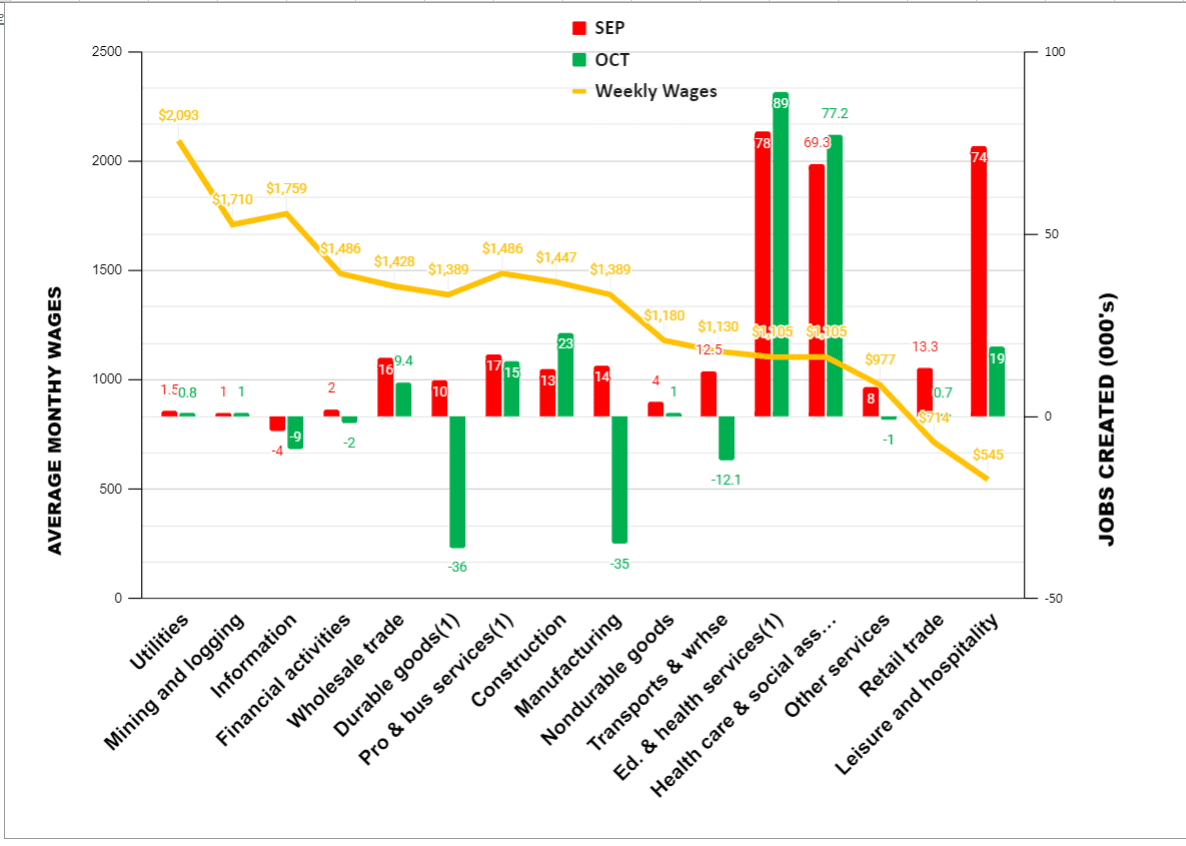

Let’s turn to our exclusive analysis of the October jobs by average weekly wages (as depicted in the chart below).

Slower job growth occurred in all areas, save for construction and education and health services (which includes health care and social assistance), which derives much of its support from government, indicates a slowing of the economy, despite the stunning third-quarter GDP of 4.9 percent.

The job losses in manufacturing comport with other data from the Institute for Supply Management’s Manufacturing Survey, discussed further below. Note that it includes more than 33,000 jobs lost in auto manufacturing, presumably from the recently settled United Auto Workers strikes.

- While “headline inflation” is down, relative to prior measures, inflation in those items that make up the daily cost of living are considerably above the “headline” number. Limited service food away from home, the kind of “grab ‘n go” food of office workers, sales people, and construction workers is up 6.4 percent. Rent is up over 7 percent. Transportation services, which includes things like auto repairs, is up over 9 percent. All those expenses, to say nothing of the cumulative effect of inflation over the last few years, will all add to wage pressure and, hence, continued inflation pressure.

- The just concluded UAW strike resulted in generous wage concessions that are likely to be sought by other union workers, particularly in service sector unions and civil service unions.

- The pandemic relief for childcare expenses expired at the end of September, so we believe that women, the traditional participants in childcare benefits, will requre a higher wage to participate in the labor force to make up for the loss of the pandemic benefits.

Prognostications

We believe headline inflation will continue in the 3–4 percent range until at least the third quarter of 2024, partly because of the elections in the fourth quarter of that year. Once that is settled, we believe rates will resume their upward trajectory, unless the Fed surrenders to those calling for a higher than 2 percent inflation target. In the interim, we anticipate tepid growth, with GDP in this quarter (fourth quarter 2023) to print at around 1.5 percent and the first quarter of next year to print at 1 percent. Again, we anticipate that the tepid economy will continue with higher inflation, so we will have a period of “stagflation”—the portmanteau for economic stagnation with inflation.Much of the continued inflation will be the consequence of having to refinance maturing federal debt at much higher rates. It’s estimated that about one-third of government debt will mature over the next year, and at the higher rates the Fed has imposed over the last year or so. That will, itself, cause higher inflation.

GDP has been very difficult to assess, largely, we believe, because consumer spending has exceeded expectations in large part from the wealth effect, whereby people with greater wealth tend to consume more. Pandemic social and economic policy tended to benefit upper-income and wealthy households more than middle-income and poor families.