Testifying before the Senate Banking Committee on March 7, Federal Reserve chairman Jerome Powell said he is prepared to accelerate interest rate hikes as economic growth and labor shortages continue to fuel inflation.

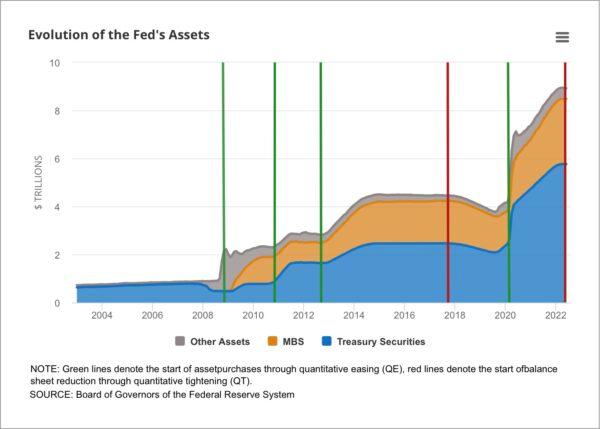

Meanwhile, the Fed is still sitting atop a massive $8.4 trillion portfolio of bonds it bought through economic stimulus programs. This portfolio now needs to be liquidated as the Fed shifts from stimulus to a more restrictive monetary policy to fight inflation.

“The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated,” Powell told Senators, signaling that the Fed may return to 50-basis-point rate hikes this year.

Alongside the Fed’s interest rate actions is the hangover of its unprecedented bond-buying spree that started during the 2008 mortgage crisis and then accelerated during the covid pandemic.

The Fed’s balance sheet ballooned from less than $1 trillion in August 2008 to a record $9 trillion in April 2022.

This effort to prop up a reeling economy by buying bonds and injecting cash into the economy is called quantitative easing (QE).

“With its return during the pandemic, QE seems to have become a more routine part of the Fed’s crisis toolkit.”

The Fed engaged in quantitative easing as an experiment when its other tool to stimulate the economy, reducing short-term interest rates via the banking system, hit its limit; short-term rates in 2008 approached zero.

The central bank embarked on the bond-buying spree to try to drive down longer-term interest rates in bond markets as well.

Reversing Bond Buying

Now that policy goals have turned to fighting inflation, the Fed has shifted its bond purchase program into reverse.Still, it has a long way to go as it has only unloaded 5 percent of what it acquired.

What this balance sheet reduction means is that there is a second dynamic at play, which has only just started and that will add to the interest rate hikes the Fed is conducting to cool down America’s economy.

Removing the Fed, which had been the dominant buyer of bonds in its stimulus days, from bond markets will reduce demand, driving bond prices down and pushing interest rates up.

How much and how fast this will slow economic growth remains uncertain for two reasons. First, the Fed has never had such a large accumulation of assets to unload; secondly, it is getting rid of them in a variable way.

According to the Fed report, “There is still debate among economists over how and how well [QE] works. And when it comes to the reverse process of shrinking the Fed’s balance sheet, typically referred to as quantitative tightening [QT], economists know even less.”

Rather than simply sell off assets, the Fed has been allowing them to mature with caps on how much they will roll over, William Luther, director of the American Institute for Economic Research’s Sound Money Project, told The Epoch Times.

‘Volatility For Bond Markets’

“Because it has this roll-off scheme when a lot of treasuries or mortgage-backed securities mature in that month, you get a big reduction in the balance sheet and correspondingly, a big reduction in the demand for those assets on the open market, because the Fed is a big player in these markets,” Luther said.“So that’s a source of volatility for bond markets that we don’t usually have.”

At the same time, despite the Fed steadily increasing short-term rates, the real interest rates, calculated as interest rates minus inflation, just recently crossed into positive territory, meaning that they are above inflation.

According to the Fed, the real interest rate as of February is 1.58 percent.

This is some marginal good news for savers as, for the first time since 2009, with rare exceptions, they can earn a small positive return on their savings over what they lose to inflation. This has brought fixed-income investments back into vogue as investors once again see positive returns from low-risk securities like U.S. treasury bonds.

“It’s always tempting in situations like this to say, ‘Well there is this silver lining,’” Luther said. “But if it would have been possible to avoid this inflation fiasco and the higher interest rates that bringing down inflation requires, certainly we would have preferred that.

“We’re worse off as Americans, on average, having gone through this high inflation and disinflation period than we would have been if inflation had just been stable and predictable.”