In the wake of the failures of several regional banks, Americans across the board are finding it harder to get credit.

Because smaller banks are so critical to small-business and consumer lending, many analysts predict the fallout from the Fed’s campaign to tame inflation will have dire consequences for the economy.

“Bank lending peaked in May of 2020 at 11 percent year-over-year growth,” Steve Hanke, professor of Applied Economics at Johns Hopkins University, told the Epoch Times. “Today, that number has slowed to 5.5 percent per year.

“Following the failures of Silicon Valley Bank, Silvergate Bank, and First Republic Bank, I anticipate that bank lending will continue to decelerate as the credit market tightens up,” said Hanke, who served on President Reagan’s Council of Economic Advisors.

Although the failed banks accounted for just 1 percent of total lending, many other banks have similar problems today. Measured as a share of total lending, banks with a high loan-to-deposit ratio provide 20 percent of all loans, banks with a low share of FDIC-insured deposits provide 7 percent, and banks with concentrated deposits provide 4 percent.

Smaller banks, below $250 billion in assets, comprise about half of all business lending, 60 percent of residential real estate lending, 80 percent of commercial real estate lending, and 45 percent of consumer lending, Goldman reports.

“We are heading towards a credit crunch,” Hanke said. “We know that a recession is baked in the cake because the money supply (M2) has been sharply contracting, falling by 2.9 percent since March 2022.”

M2 represents cash and short-term bank deposits; this measure is seen as a key indicator of inflation if it outpaces GDP, or recession if it lags.

“Unfortunately, the Fed doesn’t pay any attention to the growth rate in the money supply,” Hanke said. “As a result, it has dramatically increased the Fed funds rate and engaged in [quantitative tightening].

“This deadly cocktail has plunged the money supply (M2) by 2.9 percent since March 2022,” he said. “At present, the year-over-year growth rate of the M2 is -2.4 percent, whereas the golden growth rate, as I calculate it which is consistent with hitting a 2 percent inflation target, is around 5.5 percent. This spells trouble for the credit market.”

“Only about 20 percent of lending is going through the banking system, and only a fraction of the banks are small and regional banks,” he said. “I just don’t think it is big enough by itself to send the U.S. economy into recession.”

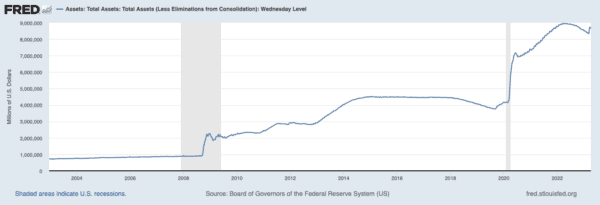

The Fed policy of quantitative tightening (QT) follows a decade of quantitative easing (QE), in which the Fed accumulated nearly $9 trillion in bonds between the 2008 mortgage crisis and the 2020 COVID lockdowns.

Through an experimental strategy, it accumulated treasury bonds and mortgage-backed securities in unprecedented quantities, flooding the market with dollars to drive longer term rates down, while keeping short-term rates near zero—all in an ongoing effort to stimulate the economy and prop up asset values.

Now that the Fed is beginning to shift into reverse to combat inflation, it is embarking on an equally experimental policy of downsizing its balance sheet. The consequences of QT on the banking system and the economy are effectively a guessing game.

According to some economists, the Fed should focus on the money supply as the key driver of inflation and not get distracted by other factors.

“The Fed should be paying attention to the Quantity Theory of Money, and should stop its obsession with data-dependency and chasing what are a thousand irrelevant rabbits at the same time,” Hanke said. “In short, the Fed is paying attention to the noise and missing the signal.”