Members of the Federal Reserve board and presidents of the Fed’s regional banks collectively let the world know on Sept. 16 that they think overnight interest rates in the United States will stay at a range of zero to 0.25 percent for at least through 2023.

In response, interest rate and bond markets were basically unchanged, digital currencies are up about 3 percent versus the U.S. dollar, gold prices are also up slightly, and the S&P 500 index of large-capitalization stocks initially rallied about 0.75 percent in just 40 minutes, only to lose steam and sell off later in the day.

Furthermore, the Fed announced after its last meeting before the November election that it plans to continue buying mortgages from other financial institutions as well as U.S. Treasuries from the open market “at least at the current pace, to sustain smooth market functioning and help foster accommodative financial conditions, thereby supporting the flow of credit to households and businesses.”

In other words, it wants to keep overall interest rates low (and thus will keep buying Treasury bonds) and also mortgage rates low (and thus will keep buying securities related to U.S. mortgages, or mortgage-backed securities).

This should be seen as providing a major tailwind to the U.S. housing market for the foreseeable future.

Of course, while jets with a tailwind go faster, turbulence can still occur.

Turbulence in the financial sector, in the real economy, or in the housing sector can come in the form of a resurgence in COVID-19 cases causing another wave of shelter-in-place orders, a disruptive geopolitical event, or a surprise in the U.S. elections.

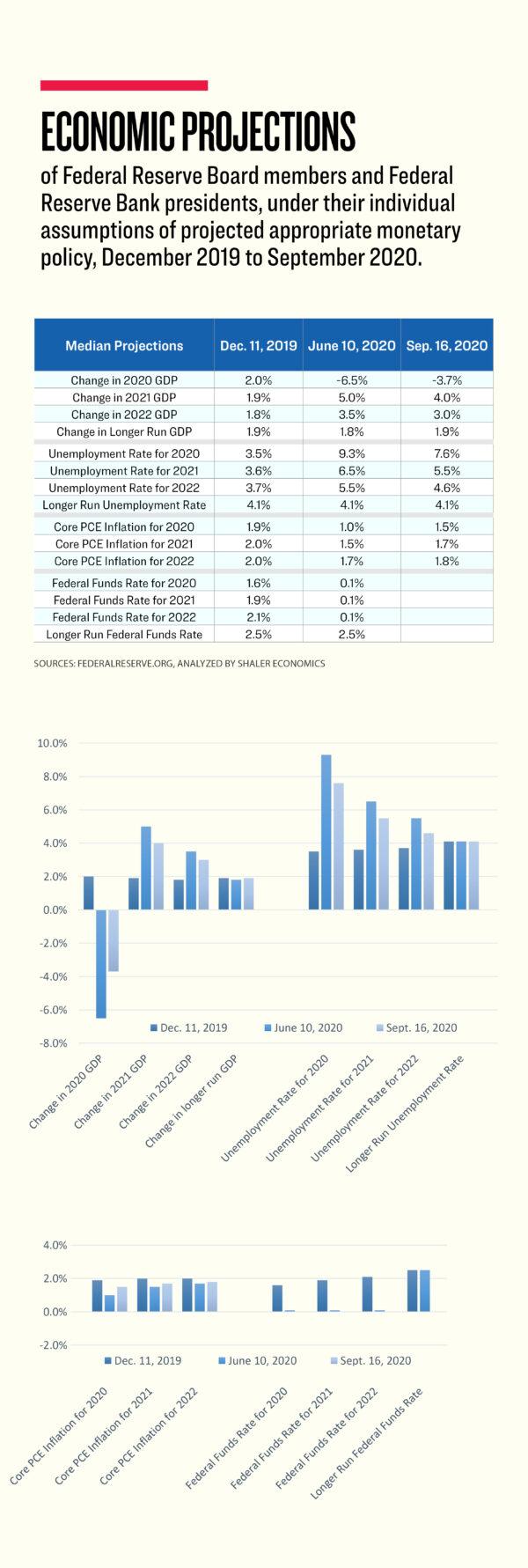

Fed Officials’ Changing Assessments

The accompanying table shows the Fed board members’ and regional presidents’ changing assessments from before the pandemic (December 2019), during the third month of the pandemic (June 10), and Sept. 16.

It shows those officials’ shifting assessments regarding the change in gross domestic product (GDP), the unemployment rate, their favorite measure of inflation, and the interest rate that their institution most directly influences—the rate that banks charge each other for overnight loans to each other, called the fed funds rate because of the central bank’s actions to manipulate that rate directly.

Perhaps most interesting from the data after their assessment that overnight rates are going to remain steady near zero for at least the next three years is that the Fed officials surveyed now think the U.S. economy (GDP) will shrink by 3.7 percent this year, a rosier outlook than the 6.5 percent contraction projected in June.

Perhaps third most interesting is their new median (midpoint) projections for inflation in 2020-2022: They are now expected to be only slightly higher than the median projection of three months ago and still lower than the projections of six months ago—even as trillions of new dollars are being being pumped into the global economy from the Fed and other central banks globally.

Price Signals Today

We can’t survey market participants about why they are buying or selling. But we can observe through price action whether they are buying or selling. If there are more buyers than sellers at a given price level, prices will keep going up until the number of buyers and sellers are about equal, or “the market” reaches “equilibrium.”So, from the price signals we can observe, we can look for clues as to why.

It seems the bond markets weren’t surprised by the announcements. Markets for interest-rate-related instruments are generally all unchanged. The interest rate on the 10-year U.S. Treasury bond was unchanged at about 0.68 percent and the market assessment for forward inflation over the next 10 years remains at about 1.7 percent.

There had been a risk that the market would reassess its long-term inflation expectation and that interest rates would have to go up to reflect that changed assessment. However, interest-rate markets are unchanged, an indication that bond markets didn’t see anything they weren’t expecting.

Investors in U.S. stocks are likely happy that the Fed plans its very accommodative interest rate policy going forward and the market was up slightly in response.

Gold investors seem to be more concerned about future inflation than other investors. Gold prices are up today as more gold buyers are entering the market for gold than there are sellers leaving the market for gold.

Going Forward: The Fed’s New Inflation Target

Buried within the monetary policy statement was the much-anticipated new statement regarding inflation:“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With inflation running persistently below this longer-run goal, the Committee will aim to achieve inflation moderately above 2 percent for some time, so that inflation averages 2 percent over time and longer-term inflation expectations remain well anchored at 2 percent.”

Putting together all the data we received, Fed officials believe inflation will remain below 2 percent in 2020, 2021, and 2022, finally get to 2 percent in 2023 and then hope to keep inflation “moderately above 2 percent” for a few years thereafter so that, over this six- or seven- or eight-year period, the long-term inflation rate will have averaged 2 percent. As 2024 approaches, markets will then be assessing whether the Fed is likely to achieve this new policy goal and what it means for interest rates, stock prices, gold prices, digital currencies, and real estate prices.