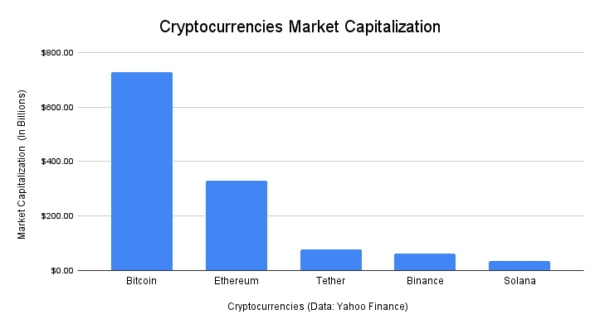

A graph showing the cryptocurrency's growing market share. Chad Hagan/Source Data: Yahoo Finance

Chadwick Hagan

Author

Chad is a financier, author, and columnist. He has managed businesses and investments in global markets for over two decades. He is the host of the podcast “Deep Dive Inside,” which discusses Western society. His latest book is “The Myth of California: How Big Government Destroyed The Golden State” (2024).