Tens of millions of Americans will start receiving their monthly federal student loan bills again, the first time in three years, as the pause on loan payments and collections expired on Oct. 1.

The pause first went into effect in March 2020 as part of the Trump administration’s effort to ease the financial burden on Americans as the government enacted stay-at-home orders during the COVID-19 pandemic. The repayment pause was extended numerous times under the Trump and Biden administrations but ended on Oct. 1 after a debt-ceiling deal prohibited President Joe Biden from extending it further.

For most borrowers, the first payment will be due in October, but not everyone will have the same due date.

Borrowers will receive a bill at least 21 days before payment is due, noting the payment amount and due date, according to the Department of Education (DOE), which oversees a federal student loan portfolio totaling more than $1.6 trillion, owed by about 43 million people.

Those who graduate in the spring don’t have to make payments until their grace period expires, which is typically six to nine months after they leave school.

Borrowers can expect the monthly repayment to be the same as it was before the pause—unless they made optional repayments or changes to their account, such as consolidating loans—as their repayment amounts were essentially frozen.

Repayment Plans

Typically, borrowers will pay back their loans through income-driven repayment (IDR) plans, in which the monthly repayment amount is primarily based on the borrower’s income, and any remaining balance will be discharged at the end of the 20- or 25-year repayment term.The DOE currently offers four different IDR plans. Its newest, “most affordable” IDR plan, dubbed Saving on A Valuable Education (SAVE), is replacing the widely used Revised Pay As You Earn plan, known as REPAYE. The department is also limiting new enrollments in other older repayment plans.

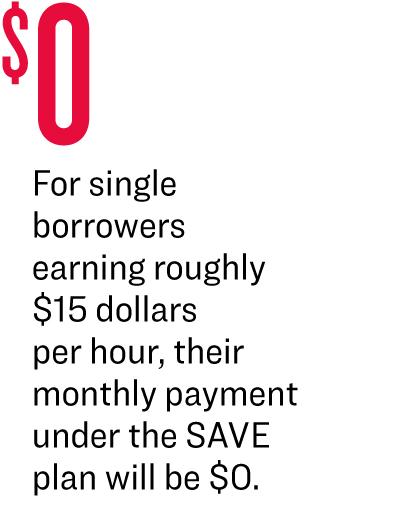

The plan places the threshold for discretionary income at 225 percent of the federal poverty guideline, meaning that for single borrowers earning less than $32,800 per year, or roughly $15 dollars per hour, their monthly payment will be $0. Borrowers who make less than $67,500 for a family of four would also see $0 monthly bills.

Starting next summer, most other borrowers on the SAVE plan will have their repayments on undergraduate loans cut by at least half. Borrowers who have undergraduate and graduate loans will pay a weighted average of 5 to 10 percent of their income based on the original principal balance of their loan.

Students who borrow less than $12,000 will see their remaining balances wiped out after making 10 years of repayments instead of 20 to 25 years.

For those who make monthly repayments, their loan balances won’t grow due to unpaid interest. For example, if $50 in interest accumulates each month and the borrower makes a $30 repayment, the remaining $20 won’t be charged.

Delaying Payments for a Year

The impact of the resumed repayments will be more profoundly felt by younger borrowers who left college and exhausted their six-month payment grace period during the three-year freeze. They might have rented a pricier apartment, signed onto a more expensive car loan, or taken on other debt with the assumption that they could afford those bills without having to worry about student loans any time soon.

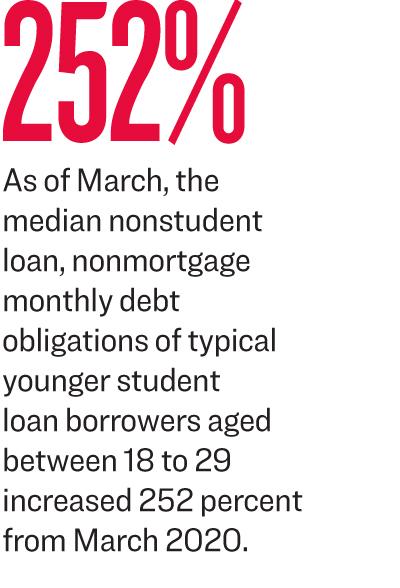

Many young people have done that, according to an analysis by the Consumer Financial Protection Bureau, an agency within the Federal Reserve. As of this March, the median nonstudent loan, nonmortgage monthly debt obligations on typical younger student loan borrowers aged between 18 and 29 was at $229, a 252 percent increase from about $65 in March 2020.

For borrowers who worry that they won’t be able to resume repayments this fall, the Biden administration is offering a year-long “on-ramp” repayment period.

Borrowers don’t need to enroll in or sign up for the on-ramp, according to the DOE. If they simply don’t pay, they'll be automatically eligible.

During the on-ramp period, spanning from Oct. 1, 2023, until Sept. 30, 2024, the DOE won’t report borrowers to debt collection agencies or credit bureaus for late, missed, or partial payments, nor will it place loans in default or delinquency.

However, interest will still add up during the period, meaning that the overall balance will balloon if the borrower doesn’t make monthly payments to at least cover the interest.

On top of that, missed payments will still be due after the on-ramp expires, and they won’t be counted toward loan forgiveness under IDR plans or Public Service Loan Forgiveness.

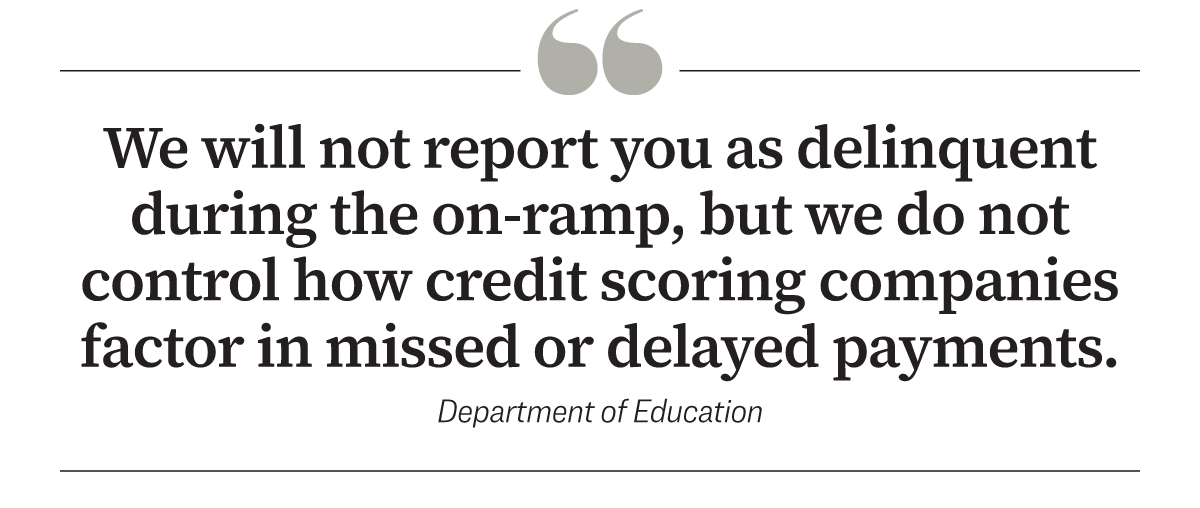

“We will not report you as delinquent during the on-ramp, but we do not control how credit scoring companies factor in missed or delayed payments,” the DOE stated.

“Your servicer will still provide you with billing statements showing you are delinquent on your payments. Not making a payment will result in you owing more on your student loans and could also impact your credit score.

“As interest builds up, your servicer may also be required to increase your monthly payment to ensure you pay off your loans on time. If so, your servicer will send you a notice of the changed monthly payment amount.”

In June, when announcing the creation of the student loan on-ramp, President Biden told borrowers that it’s meant to act as a safety net and that just because borrowers can miss payments for a year without negative credit consequences doesn’t mean that they should.

“During this period, if you can pay your monthly bills, you should,” he said.

A New ‘Forgiveness’ Program?

So far, the Biden administration has discharged $127 billion of student loan debt for nearly 3.6 million Americans.In addition, the Biden administration has reintroduced its plan to “forgive” hundreds of billions of dollars of federal student loan debt, by using the Higher Education Act (HEA), which proponents of student loan cancellation argue allows the government to “compromise, waive, or release” student loans.

Relying on the HEA to advance the plan, the Biden administration will turn to a typically lengthy, complicated process called “negotiated rule-making.” The Act is expected to first undergo many rounds of public hearings and months-long comment periods that require an extensive amount of public input before any changes can come into effect.

In an update released on Sept. 29, the DOE stated that it has received more than 26,000 public comments on how to tailor this relief and will soon be discussing the initial set of policies with the newly established Student Loan Relief Committee.

“The debt relief issue paper will be discussed at the first meeting of the Student Loan Relief Committee, which is scheduled to take place October 10 and 11,” the department stated.

“The committee will be comprised of non-federal negotiators from 14 affected constituency groups, as well as a negotiator from the Department. During the session, the non-federal negotiators will provide input on the policy considerations and questions outlined by the Department, as well as identify any new proposals they may have. Members of the public will also have an opportunity to provide comments at the end of each day.”

The committee is also scheduled to meet in November and December. The public will have an opportunity to submit written comments on the draft rules when they’re published next year.

A federal agency must propose rules by Nov. 1 for them to go into effect by the following July. The DOE doesn’t have nearly enough time to finalize its rule before Nov. 1, so it'll instead need to announce final rules on student loan forgiveness before Nov. 1, 2024, days before the presidential election.

A change in presidency would likely halt or even undo the final rules’ implementation. In 2019, then-Education Secretary Betsy DeVos tossed a “gainful employment” rule regulating the federal funding for career programs that had been passed under the Obama administration.

In the meantime, the DOE advises borrowers to continue paying off their loans while they wait for a possible new debt relief program.

“This [negotiated rule-making] process will take time, and you will be required to make payments in the meantime,” the agency stated. “When designing a new debt relief program, we will consider ways to ensure that borrowers making payments maintain their eligibility for debt relief.”

President Biden’s original plan, which would have canceled up to $10,000 in student loan debt per person for those earning less than $125,000 and another $10,000 for Pell Grant recipients who meet the income limit, was grounded in the Higher Education Relief Opportunities for Students (HEROES) Act of 2003, a law passed in the aftermath of the Sept. 11 terrorist attacks.

Although the Biden administration argued that the HEROES Act would allow the education secretary to cancel student loans in response to the COVID-19 public health emergency, the U.S. Supreme Court disagreed.

“The HEROES Act ... does not allow the Secretary to rewrite that statute to the extent of canceling $430 billion of student loan principal,” Chief Justice John Roberts wrote for the high court’s 6–3 majority, noting that what was outlined in the president’s plan “created a novel and fundamentally different loan forgiveness program” that “expanded forgiveness to nearly every borrower in the country.”

Republican Alternatives

Prior to the Supreme Court ruling that struck down the president’s plan, a group of House Republicans introduced their own plan, which they say will ensure “a smooth transition back into repayment” while still providing relief to those most in need.The proposal, formally called the Federal Assistance to Initiate Repayment (FAIR) Act, is sponsored by Rep. Virginia Foxx (R-N.C.), who chairs the House Education Committee, along with Reps. Burgess Owens (R-Utah) and Lisa McClain (R-Mich.).

Specifically, the bill would condense the four existing IDR plans into one “predictable and affordable” plan, require borrowers enrolled in the new IDR plan to recertify their income before repayments resume, and make sure repayment assistance phases out as borrowers’ incomes increase.

As for debt relief, the bill would eliminate the time-based discharge of remaining loan balances and instead waive borrowers’ remaining balances if they “already paid back more than they originally owed taxpayers in principal and interest.”

The bill would also give defaulted borrowers a second chance to reenroll in a repayment plan, removing the black mark of default from their credit report as long as they make their required monthly repayments.

“The FAIR Act is a fiscally responsible, targeted response to the chaos caused by Biden’s student loan scam,” the bill’s sponsors said in a joint statement. “This Republican solution takes important steps to fix the broken student loan system, provide borrowers with clear guidance on repayment, and protect taxpayers from the economic fallout caused by the administration’s radical free college agenda.”

In the Senate, Republicans have proposed the Lowering Education Costs and Debt Act, a five-bill package aimed at providing students and families with better information before taking out a loan, in the hope that they understand and carefully consider their options.

This collection of bills, according to primary sponsor Sen. Bill Cassidy (R-La.), would streamline repayment options, require some loan counseling, improve transparency about college programs, standardize student aid offers, limit graduate school borrowing, and prevent new loans from going into undergraduate and graduate programs where former students can’t earn more than a high school graduate or a bachelor’s degree, respectively.

The DOE is the country’s biggest consumer lender, surpassing financial giants such as Bank of America, JPMorgan Chase, and Capital One.