As America marks its 250th anniversary, it also celebrates the foundations of its prosperity: a tradition of innovation and entrepreneurship, free-market capitalism, and institutions that have helped transform it into a global superpower.

Over two-and-a-half centuries, the country has achieved remarkable economic growth, evolving from a largely agrarian society into the world’s leading economy.

Its path, however, has not been easy. America’s political and economic systems faced severe tests from the Civil War to the Great Depression. Yet time and again, the country has defied predictions of decline and recovered strongly from each crisis.

Arthur Herman, historian and author of “Founder’s Fire: From 1776 to the Age of Trump,” argues that the defining characteristic of the American economy has been a culture of risk-taking that stretches back to the nation’s earliest settlements.

Americans tend to view risk as “an opportunity instead of a danger signal,” Herman told The Epoch Times, adding that this mindset has encouraged entrepreneurship and innovation for generations.

Although World War II marked the United States’ emergence as the world’s undisputed superpower, many historians note that its economic foundations were laid decades earlier.

It was in the years after the Civil War that a series of founders including John D. Rockefeller, Andrew Carnegie, Cornelius Vanderbilt, and James J. Hill “created a modern industrial economy,” Herman said.

One of the greatest economic drivers during that period was the railroad boom.

“The railroads were sort of the internet and AI combined in the 19th century,” Herman said.

America’s railroads transformed the nation’s economy by connecting distant markets and unlocking the continent’s vast natural resources. Many of the companies that became successful in the 19th century did so because of their connections to that new mode of transportation.

For much of the 19th century, Great Britain was the world’s dominant power due to the Industrial Revolution and the strength of the nation’s Royal Navy. Yet toward the end of the century, the United States emerged as Britain’s main economic rival.

America’s abundant natural resources and advances in transportation, steelmaking, electricity, and mass production turned the nation into an industrial powerhouse.

Unlike many countries in Europe and Asia, the United States also encouraged entrepreneurship by limiting government interference, giving innovators greater freedom to take risks, generate new ideas, and expand their businesses, Herman said.

“By the time we get to 1900, the turn of the century, the United States was already the dominant economic power on earth, far surpassing the productivity of the British Empire and that of Germany,” he said.

Roaring ‘20s

The momentum continued into the Roaring ‘20s, a decade of high economic growth and widespread optimism in the United States. Technologies that were once luxuries, such as cars, electricity, and radios, became affordable and accessible for many households.

Central to this boom was Henry Ford, whose revolutionary moving assembly line made it much cheaper to build cars, allowing them to become a regular part of American life.

Much of that development can be attributed to policy choices made in the 1920s that allowed American enterprise “to flourish and take hold,” said Matthew Denhart, president of the Coolidge Foundation.

President Calvin Coolidge, who served from 1923 to 1929, introduced sweeping tax cuts that some historians say encouraged business investment, thus fueling economic growth.

“The tax policy, and the disciplined budgeting that accompanied it from Coolidge, was very important to the economic success in the 1920s and America’s rise to be the world’s superpower,” Denhart said.

Better technology and higher productivity helped companies make more goods in less time. This allowed employers to reduce the standard workweek from six days to five, a practice begun by Ford in 1926 that remains the standard today.

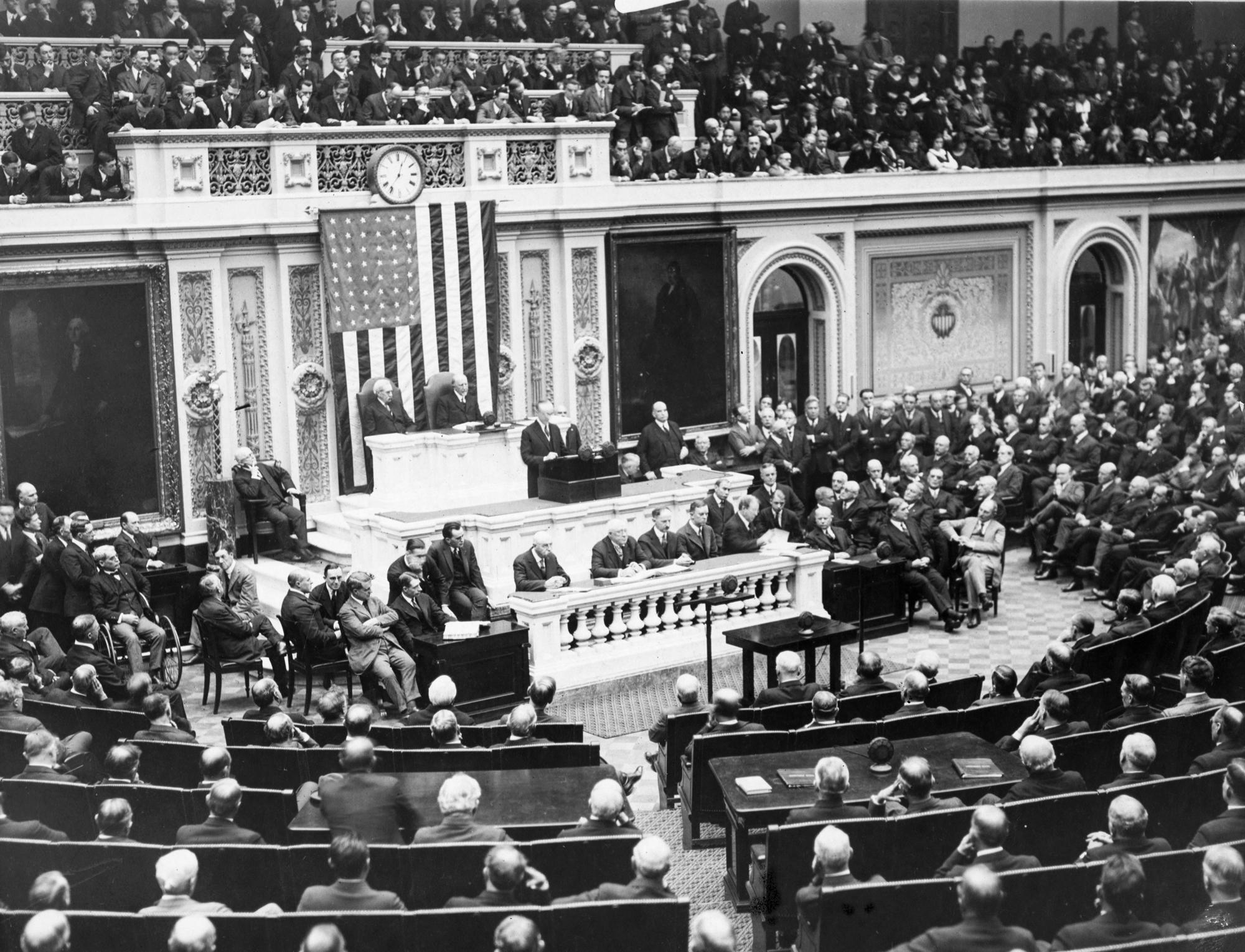

Following the 1929 stock market crash, however, the United States experienced the Great Depression, a decade-long economic downturn during which unemployment peaked at nearly 25 percent.

Historians continue to debate the causes of the Depression and the effectiveness of policy responses at the time. Some argue that President Franklin D. Roosevelt’s New Deal program helped restore confidence and revive economic activity, while others contend that his sweeping government interventions delayed the recovery.

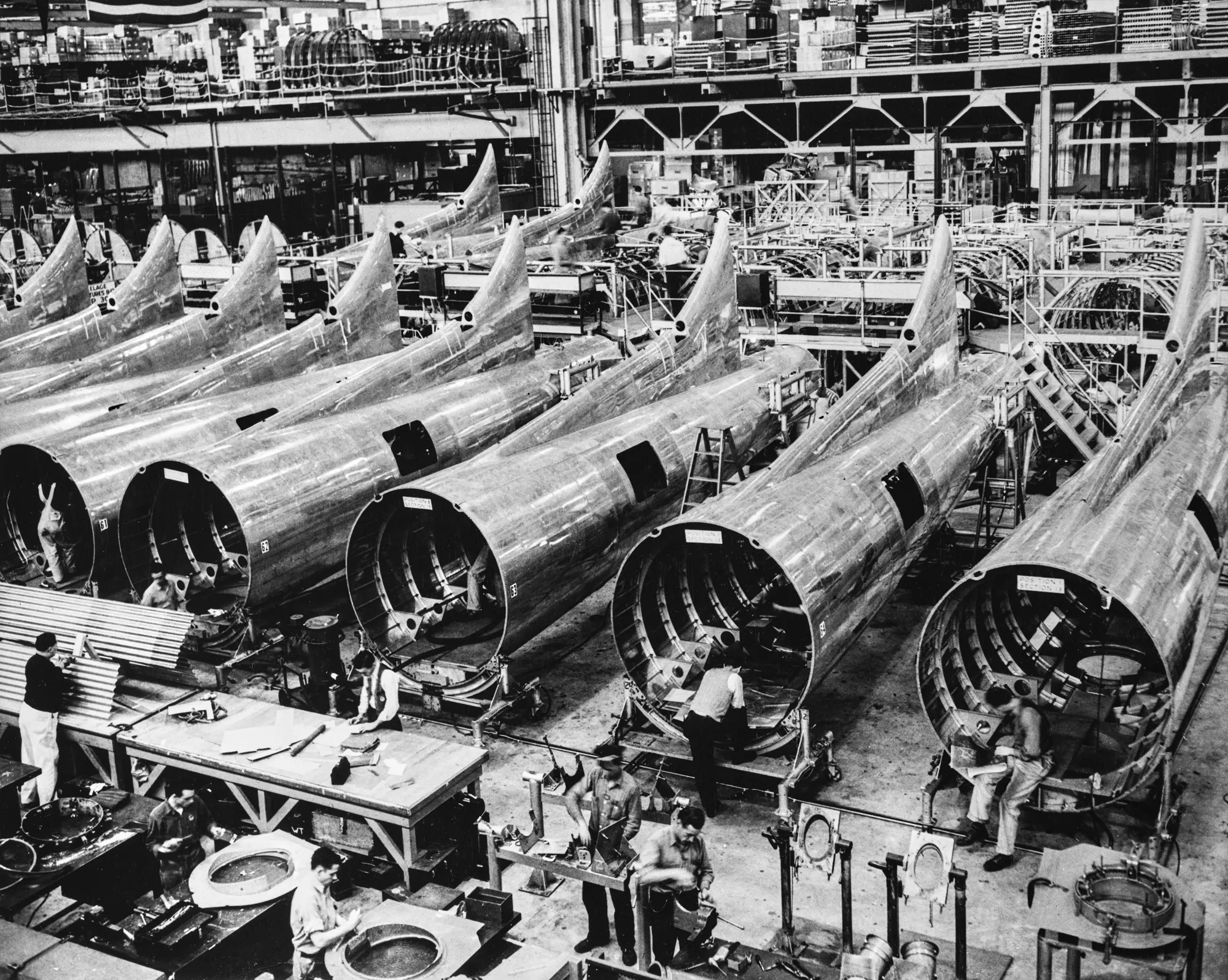

Then, the United States’ entry into World War II led to a dramatic expansion of government spending and industrial production. The wartime mobilization effort created millions of new jobs, bringing the nation’s economy back to its feet.

Rewarding Innovation

America’s culture of encouraging inventors, not just their inventions, played an important role in the country’s economic success.

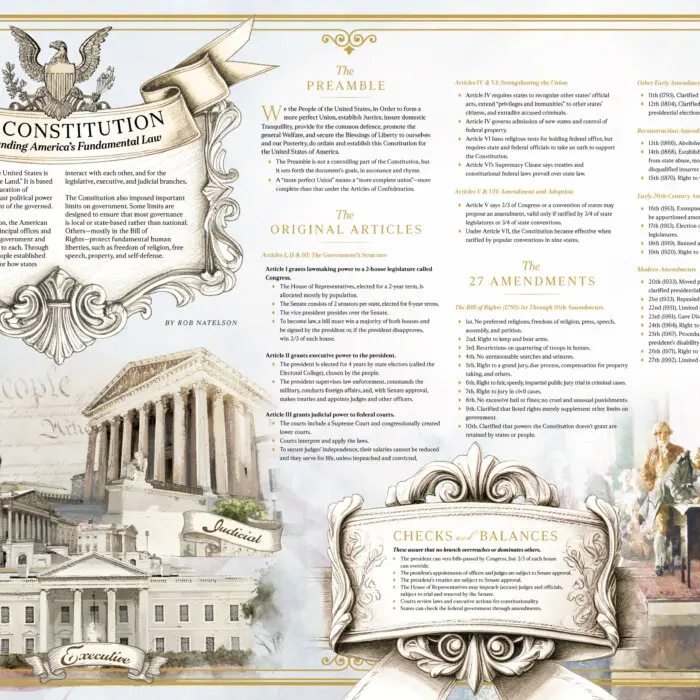

The Founding Fathers, particularly George Washington, fostered innovation by advocating for strong patent protections, said John Berlau, senior fellow and director of finance policy at the Competitive Enterprise Institute.

Berlau, who is the author of the book “George Washington, Entrepreneur: How Our Founding Father’s Private Business Pursuits Changed America and the World,” said the Constitution and the Patent Act of 1790 established intellectual property rights early in the nation’s history.

Inventors such as John Fitch and James Rumsey famously clashed over their competing steamboat designs in the late 18th century. Their rivalry played a key role in shaping early American patent law.

In the early 19th century, the United States also made entrepreneurship more accessible by allowing ordinary people to form limited liability corporations, rather than reserving corporate charters for political elites as Britain had done.

“State laws made it easy to form limited liability corporations,” Berlau told The Epoch Times, noting that entrepreneurs no longer had to risk all their personal assets to start a business.

By limiting personal financial risk and simplifying business formation, states created a flexible legal environment that encouraged more people to start businesses, he said.

‘Incredible Success’

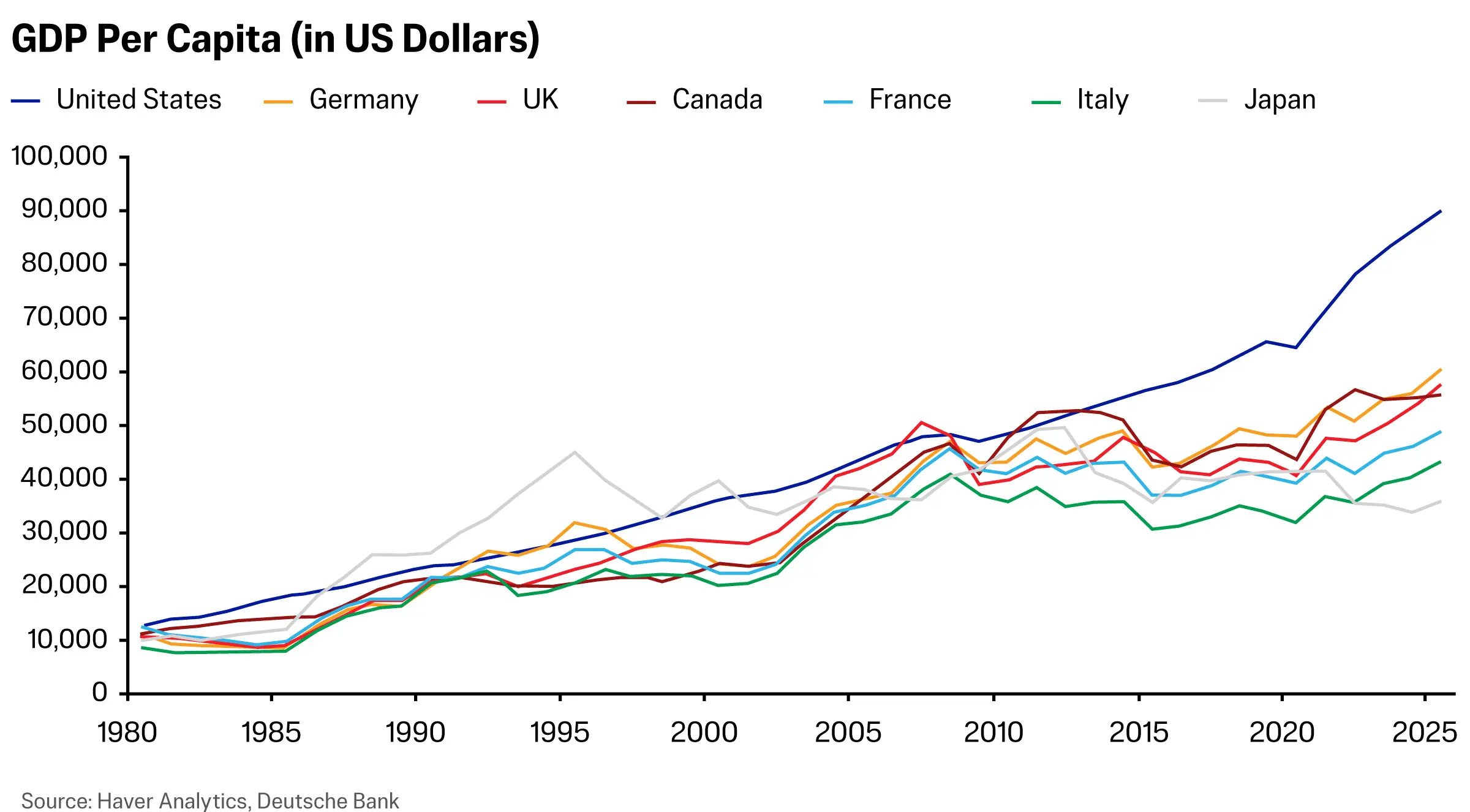

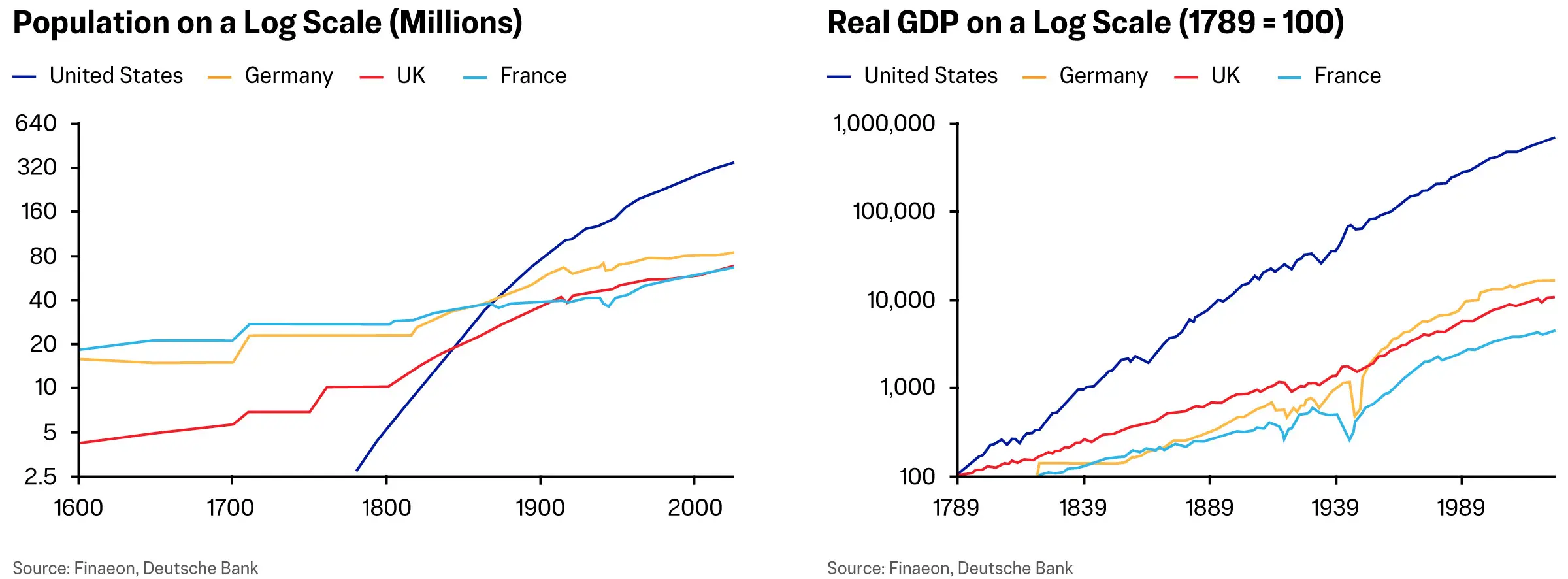

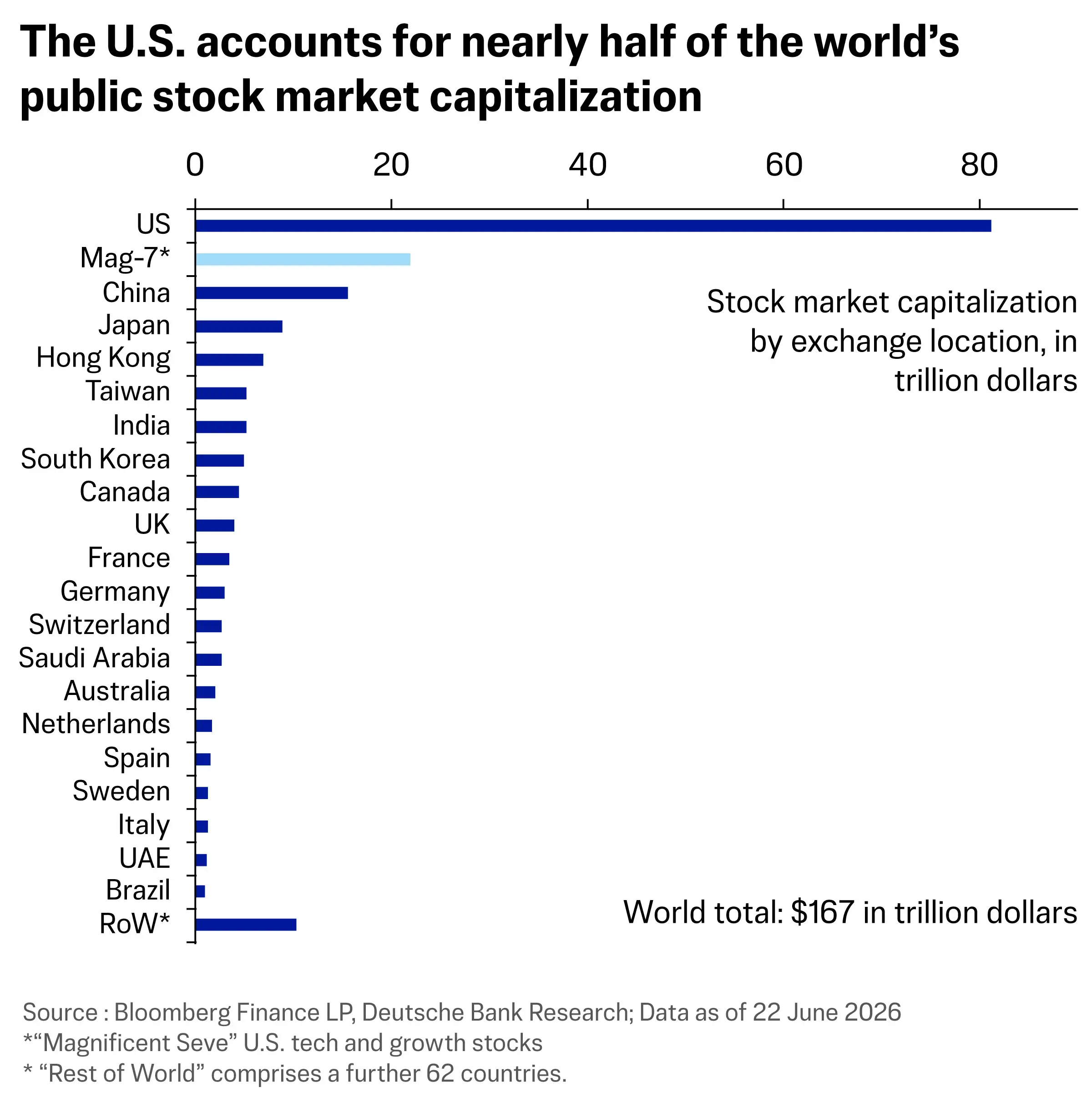

Since its founding, the United States has achieved significant economic success across a wide range of metrics. It has significantly outperformed the UK and Germany in economic growth and stock market returns.

A new report from Deutsche Bank economists examines the factors behind this “incredible success.”

“Although the U.S. has faced severe crises in the last 250 years, including a civil war, its system of government has been recognizably the same throughout that time,” the report reads.

“This relative stability and early development of property rights provided a fertile environment for long-term investments, which in turn has aided economic growth over the centuries.”

Another factor, according to Deutsche economists, is America’s geographic advantage. With relatively secure borders and no major neighboring rivals, the United States avoided the effects of the world wars that destroyed Europe.

The nation’s other advantages include abundant energy resources, a large domestic market, a deep financial system that gives entrepreneurs easy access to capital, and world-class universities and research institutions that attract top talent.

Many economists also point to the advantages of the U.S. dollar being the world’s trade and reserve currency.

“This has been dubbed the ‘exorbitant privilege’ and has been a major advantage in recent decades,” the Deutsche economists wrote. “This dollar demand matters because it lowers borrowing costs and raises demand for U.S. Treasuries.”

As a result, the United States can run larger budget deficits without facing a funding or debt crisis.

New Challenges

The United States has overcome numerous crises throughout its history. In the past 60 years alone, those have included the Vietnam War, the oil shocks of the 1970s, multiple recessions, the 9/11 terrorist attacks, the subsequent wars, the housing market crash, and the COVID-19 pandemic.

Today, economists warn that America faces a new set of challenges. These include growing competition from China, rising national debt, and increasing socialist sentiment within the United States, which some argue could undermine the country’s capitalist system.

“America has an entrepreneurial culture, and its governmental structure encourages creativity, imagination, and innovation in ways that a communist, top-down control society like China will never be able to emulate or surpass,” Herman said.

“The pattern is, the Americans create and the Chinese steal.”

According to Herman, socialist sentiment within the United States poses a greater challenge to the country’s future than its rivalry with China.

Other short-term risks include growing pressure on the U.S. dollar’s status as the world’s reserve currency and on the nation’s fiscal outlook.

“When and if international markets decide that the U.S. debt is riskier than it may seem today, that’s when a lot of these fiscal challenges will come to a head,” Denhart said.

Despite that danger, the Deutsche Bank economists wrote: “The challenges facing the U.S. are real, but the weight of evidence still suggests it will remain the world’s leading economy for the foreseeable future.

“Its collective structural advantages remain difficult to replicate.”