The Organization of the Petroleum Exporting Countries (OPEC) reached a much-anticipated deal to curb oil supply. However, the cartel’s attempt to boost the price of oil may be challenged by weak global demand, rising U.S. shale production, and President-elect Donald Trump’s energy policies.

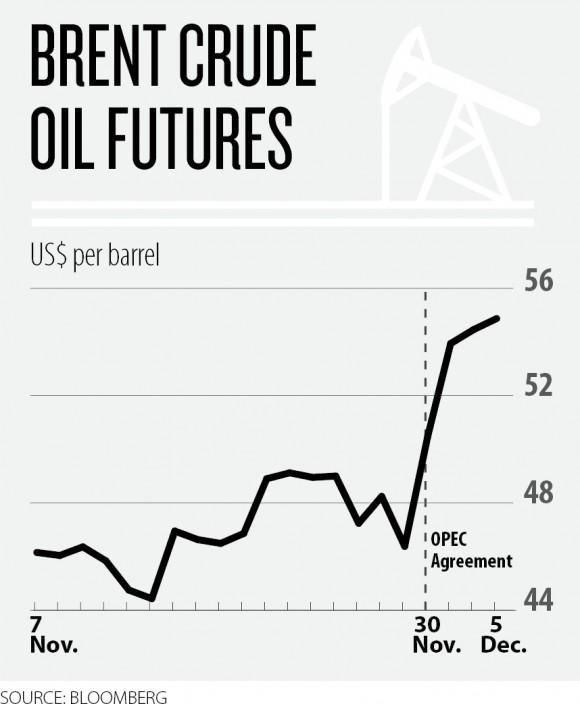

OPEC agreed to cut production for the first time since 2008. Oil price has jumped more than 15 percent in the days following the announcement of the deal on Nov. 30. The S&P 500 energy index gained 6 percent.

“I think there is a short-term effect we’re already seeing in the market, but it does not imply a long-term price recovery,” said Hillard Huntington, executive director at Stanford University’s Energy Modeling Forum.

“I don’t think oil prices will come back up strongly until we start seeing some increased demand for oil—a much stronger world economy than we have now.”

After months of negotiation, OPEC agreed to cut the production by 3.5 percent, to 32.5 million barrels a day. The production cut will start in January next year and last for six months.

US Response

While it is not clear whether OPEC members will comply with the agreement, U.S. shale companies may respond to the cut. If there is a sustained increase in prices, U.S. companies may ramp up oil production, which would, in turn, push down the prices again.

The U.S. response, however, will not be as fast as most people predict, according to Phil Flynn, senior market analyst at Price Futures Group in Chicago.

“This production cut will give a boost to shale, but it will take at least a year for the U.S. oil production to get back to where it was a year ago,” Flynn wrote in a report.

U.S. oil production stands at 8.7 million barrels a day—still almost a million barrels less than at last year’s peak.

In the past, OPEC, led by Saudi Arabia, had largely dictated the oil price. The rise of U.S. shale production, however, recently changed the dynamics in the oil market.

U.S. oil production nearly doubled from 2012 to 2015 thanks to the shale revolution, which started with the development of new technologies in oil extraction.

This caused a global supply glut and a sharp drop in oil prices since 2014. As a result, about one-third of the shale companies went bankrupt or became financially distressed.

“OPEC members sold oil at a loss just to drive down prices and put shale players out of business,” Flynn stated.

However, despite the low prices, shale producers remained resilient by cutting costs.

“U.S. shale producers have learned to cut costs, but many of them are still deep in debt,” Flynn wrote. Hence he does not expect a major spike in U.S. output right away.

“The U.S. producers might be reluctant to do a lot of investment at these price levels, as they will not cover the investment costs,” said Huntington.

Depending on the degree of compliance by OPEC members and an additional cut by non-OPEC countries including Russia, Goldman Sachs predicts the Brent oil price will range between $56.50 and $62.50 in the first half of 2017.

But what really matters for the oil industry and economic activity in the United States is oil price stability, according to Huntington.

Sharp movements in the price, either up or down, create a lot of economic dislocation. This creates uncertainty, which U.S. businesses don’t like, he said.

Energy Independence and the Price Reality

President-elect Trump envisions a nationalist energy policy based on making America energy independent and a net energy exporter. He wants to reduce oil imports, increase domestic production, and eliminate OPEC’s influence on oil prices in the United States. He wants to unleash America’s untapped shale and oil reserves, leading to the creation of millions of new jobs in the energy sector.

“Intentions are one thing; actually writing and passing policy is another,” Alan Krupnick, a senior fellow and co-director at the think tank Resources for the Future, stated in a report.

The economic reality, including oil prices, will frustrate the Trump administration, says Krupnick.

“If prices are too low, production will not increase without subsidies of one sort of another, and it is hard to see how this type of policy will be favored by the Republican Congress,” he wrote.

In addition to subsidies, another tool for increasing domestic production and creating jobs is to consume more oil, according to Huntington. However, it’s hard for the government to create additional demand for oil in the United States, he said, as most demand comes from the private sector.

“The United States can potentially be energy independent. However, I’m not expecting that to happen at today’s oil prices,” said Huntington.