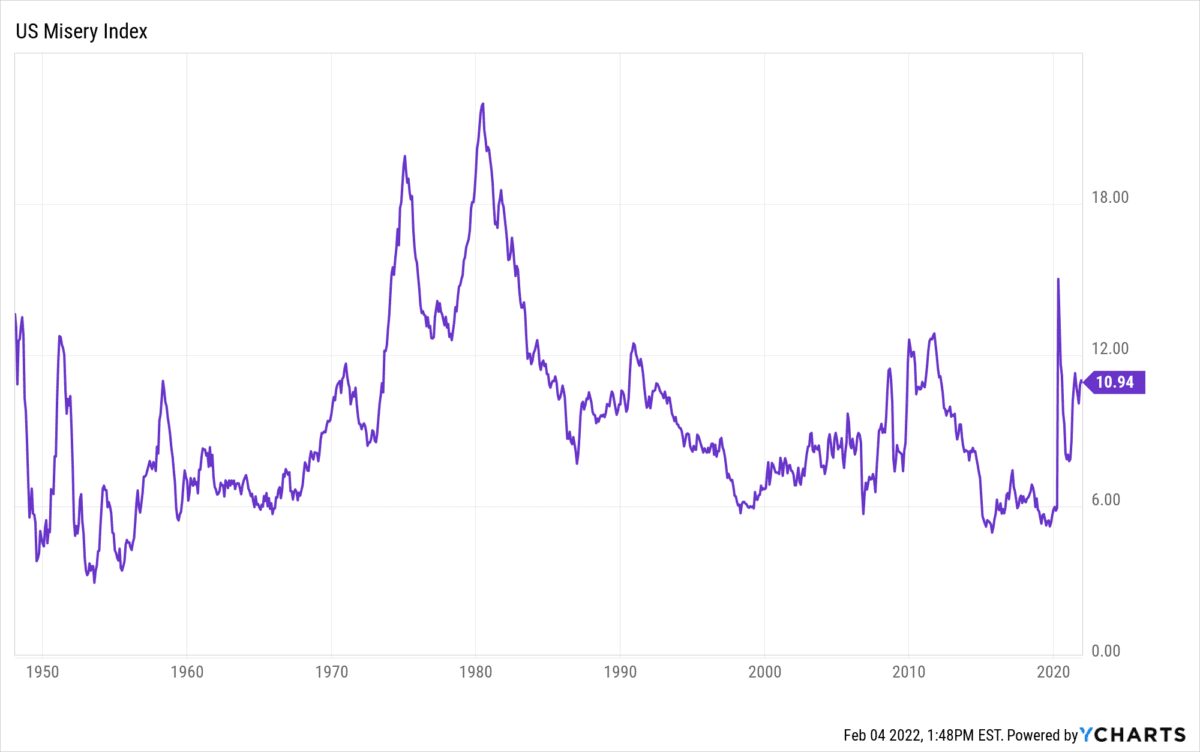

Investors of a certain age will remember the economic difficulties in the United States in the late 1970s. The malaise of the time led to the use of the term stagflation used to characterize weak or negative economic growth combined with high inflation or high unemployment. In turn, this led to the use of the statistic called the “misery index” defined as the unemployment rate plus the inflation rate.

A high misery index leads to problems for two key reasons. First, having a large number of people unemployed at a time of rising prices pretty much defines the term miserable for an economy. Second, the Federal Reserve responds to inflation by raising interest rates which tends to have a cooling effect on the economy. This can raise the unemployment rate. So, during stagflation, the Fed is left with the choice of making the cost of living more expensive for everyone, or addressing the inflation problem at the expense of more people being unemployed. Both paths have negative effects.

Looking at the misery index, we can see the spikes when President Nixon took us off of the gold standard and larger one at the end of the Carter years. There was another jump associated with the 2008 financial crisis, and also a big spike when the COVID-19 lockdowns forced the unemployment rate to temporarily high levels. The recent increase is related to inflation.

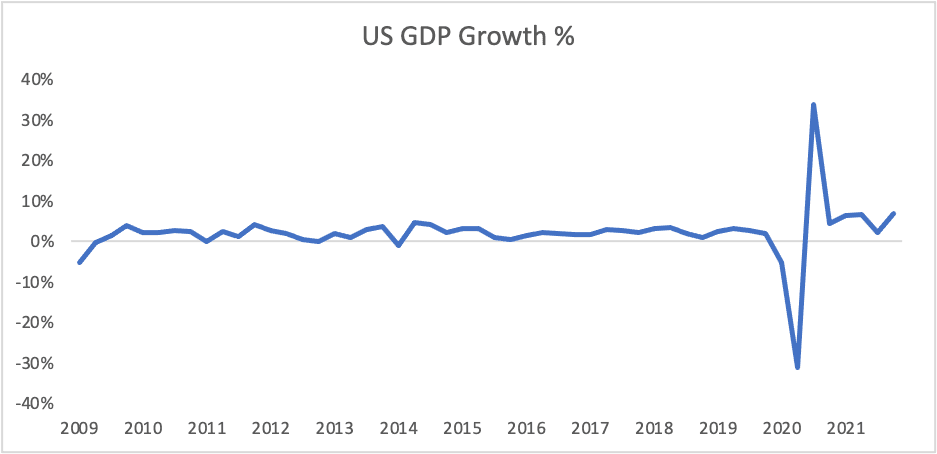

We’re also concerned that Gross Domestic Product (GDP), the standard measure of economic growth is also overstated.

In addition, GDP numbers are inflation-adjusted. There’s a good reason for this. Take the example of a baker who bakes and sells a loaf of bread for $1. If there’s price inflation and the same baker sells the same loaf of bread the following year for $2, that doesn’t represent a doubling of economic activity. It’s merely the same economic activity combined with inflation. Shedlock points out that the adjustment for Gross Domestic Purchases (essentially, the inflation adjustment) was 3.9 percent for 2021. I add that the adjustment was 6.9 percent for the fourth quarter. It’s clear from our work on inflation (cited above) and from the volume of comments from Epoch Times readers regarding their rising cost of living that these figures are understated.

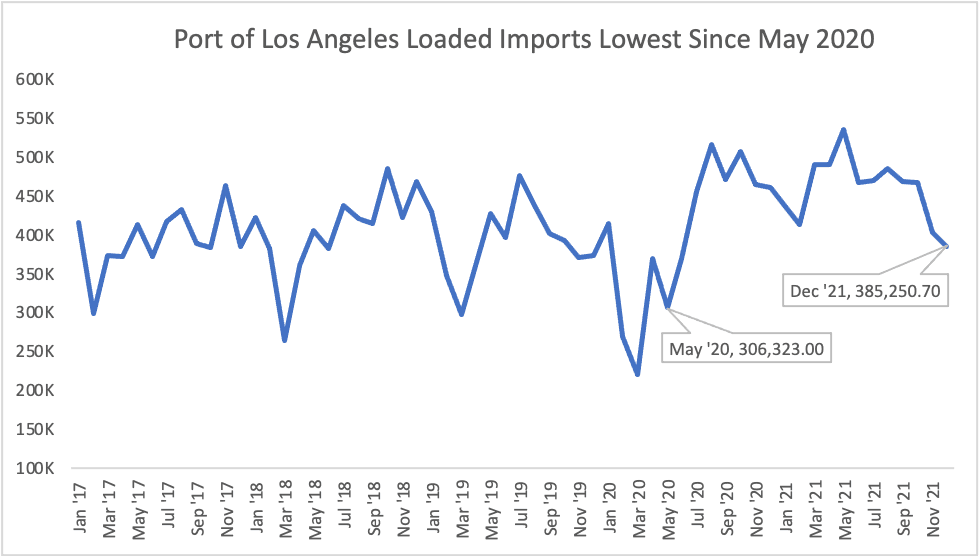

In October, the White House announced a plan to fix the port congestion by running the two ports 24 hours a day and by fining companies that didn’t pick up containers fast enough. Here’s what happened:

Import volume went from down 7.8 percent in October to down 13.2 percent in November to down 16.4 percent in December. Clearly, the White House and the Transportation Department did not fix the problem. The reason that this matters is because net imports are subtracted from GDP. While it’s true that due to port congestion, exports (which are added to GDP) also fell, because the United States imports more goods than it exports, the net effect of the ports moving fewer goods is a temporary addition to GDP figures. Adjusted for something closer to a free-trade ideal and the “excellent” recent GDP number is even further negative.