As the current banking crisis spreads, with First Republic Bank becoming the third major U.S. bank failure of 2023, many are now seeing echoes of what has come to be known as the “Great Financial Crisis” of 2008–09.

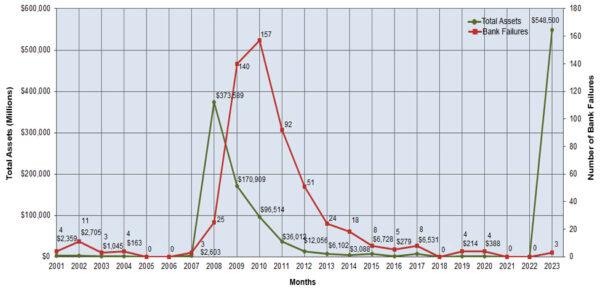

Some analysts have pointed out that, with the exception of Washington Mutual Bank, which had $432 billion in assets just prior to its collapse in 2008, all three of this year’s failed banks were larger than any of the banks that failed in 2008. First Republic Bank, SVB, and Signature Bank were America’s 14th, 16th, and 29th largest banks by assets, respectively.

The Current Crisis in Perspective

In 2008, some of America’s largest banks, such as Wachovia Corp., which was the fourth-largest U.S. bank at the time, technically didn’t “fail” but rather merged with other banks. In addition, many of the world’s largest investment banks (Lehman Brothers, Bear Stearns, Merrill Lynch), insurance companies (AIG), and hedge funds either collapsed, were acquired, or became wards of the state.“It was much more widespread in 2008,” Chris Cole, executive vice president and senior regulatory counsel for the Independent Community Bankers of America (ICBA), told The Epoch Times.

The 2008 crisis “affected banks, non-banks, mortgage companies; it affected the construction industry; just about all commercial loans were impacted by it,“ Cole said. ”And that’s why we ended up with almost 500 banks failing, and why we had a crisis among the large banks that had to eventually be bailed out.

“Here, we do not see that kind of pervasiveness going on,” he said. “I think this contagion has been largely contained.”

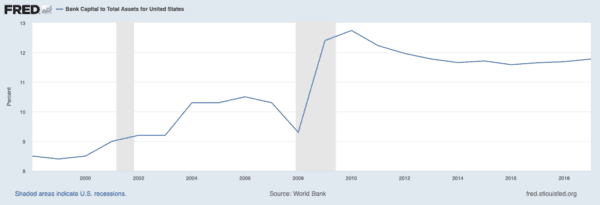

Banks, particularly those deemed “too big to fail,” are not only better capitalized today than they were prior to the 2008 crisis, but they also are subject to more strict liquidity coverage ratios, which measure their ability to pay obligations such as deposit withdrawals. This has allowed the big banks to step in and help support struggling regional banks today, rather than requiring government assistance themselves.

“The [big] banks are in great shape,” Ed Yardeni, economist and president of Yardeni Research, told The Epoch Times. “As we just saw, Jamie Dimon got himself a great bargain buying up what’s left of First Republic.”

The JPMorgan CEO’s role in propping up struggling banks today is reminiscent of the bank’s founder, James Pierpont Morgan, helping to bail out the banking system during a 1907 bank “panic,” he said.

Different Crises, Different Sources

In addition, the nature of today’s financial crisis is fundamentally different.“The U.S. banking system remains sound,” Yellen stated.

Insolvency occurs when a bank’s assets, or its loan portfolio, are worth less than its liabilities, which include its deposits. That’s a different scenario from a liquidity crisis, in which the bank is solvent but can’t pay depositors at a given moment because it has lent out the money for a longer term.

The Great Financial Crisis featured financial institutions across the entire economy taking enormous losses across their loan portfolios from credit defaults, first in their portfolios of mortgage loans and mortgage-backed derivatives, then in their consumer and commercial loans portfolios as the financial rot spread across the economy.

In the current crisis, several banks have suffered from market and liquidity problems, resulting from rapid interest-rate increases by the Federal Reserve, a sharp constriction of the money supply, and rapid deposit withdrawals—but widespread defaults haven’t yet been an issue.

“There have been a few banks that were insufficiently hedged against the interest-rate risks, but the vast majority of large banks are not among them,” William Luther, economist and director of the American Institute for Economic Research’s Sound Money Project, told The Epoch Times.

America’s largest banks “are largely insulated from the current issues we face, and so I would be very surprised if we were to see the kind of contagion that we saw in 2008,” he said.

“So far, it seems that the financial crisis is attributable to essentially three outliers, three banks that were highly exposed to interest-rate risk and to deposit runs,” Yardeni said. “We’re all crossing our fingers and hoping that’s the case and that the Fed and the FDIC [Federal Deposit Insurance Corp.] have managed to contain this problem, and that it won’t spread into an economy-wide credit crunch and recession.”

US Economy More Robust Today

“Given the data we have right now, I think [a credit crisis] is unlikely,” Luther said. “Household balance sheets remain strong, businesses are recovering and have largely recovered from the COVID-19 contraction.”“We’re just dealing with a very different economic shock,” he said. “In 2008, our primary problem was insufficient aggregate demand, whereas, in 2020 our problem was a negative productivity shock. And that negative productivity shock was temporary as we found ways of coping with COVID.”

While the current crisis hasn’t yet seen a high number of loans defaulting, analysts don’t discount the possibility that credit issues will begin to arise. The two main areas of concern are the Fed’s campaign to fight inflation through higher interest rates and tighter monetary policy, and the effects of the crisis to date on banks’ willingness to lend.

As the U.S. banking industry consolidates into an ever smaller number of firms, smaller communities may lose their access to credit and banking services. Currently, about half of all small-business loans are provided by smaller community banks, according to the ICBA. A constriction in lending, which typically happens when banks are in crisis, has a ripple effect throughout the economy.

Although consumers are in better shape than they were during the 2008 crisis, their financial health appears to be deteriorating.

The Effects of Bank Consolidation

As U.S. banks consolidate into an ever-smaller number of institutions, many worry that smaller communities will suffer.“We don’t want to follow what’s happened in the United Kingdom, for instance,” Cole said. “There are rural areas of Scotland and northern England where they just don’t have banks anymore, and in those rural areas, there’s no place to cash a check, there’s no place to get a small-business loan.

“That is slowly happening in our rural areas,” he said. “It impairs the ability of those smaller communities to grow and to be viable, and it actually accelerates that trend away from the rural areas to more urban areas.”

“The consequences of that history is that we have tended to have a lot of very small banks,” Luther said, “whereas, if you look at Canada then and now, Canada has been characterized by much larger, much more stable banks.”

According to the ICBA, the health of America’s community banks remains strong.

“Our capital quality and our credit quality among the smaller banks is excellent,” he said. “And our guys are telling us that there have not been deposit outflows, even though there are stories about deposit outflows coming out of the regional banks.”

More Like S&L Collapse in the ‘80s

“It’s tempting to make comparisons between the financial crisis of 2008 and current issues in the banking system, but the more apt comparison is actually the savings and loan crisis from the 1980s,” Luther said. “In 2008, we were primarily dealing with credit risks, whereas today, banks are facing problems due to high inflation and rising interest rates, much like they were in the 1980s.”During the 1980s, smaller banks called savings & loans (S&L) took in short-term deposits that they lent out, typically as longer-term real estate loans. An unhealthy competition set in, whereby depositors flocked to the S&Ls, or “thrifts,” that paid the highest interest, rewarding those institutions that assembled the highest-yielding loan portfolios, which were also the riskiest.

This also was a period when the Fed drove up interest rates to fight inflation. When the real estate market receded, loans began to go bad. Depositors became nervous and demanded their money back, and escalating runs on the S&Ls put many thrifts out of business overnight.