All these cases point to only an up-down or boom-bust phenomenon. All were cyclical and far from secular, exhibiting a longer cycle at most. In other words, none of these were sustainable over decades. These were not miracles, and there was no magic behind them. This kind of growth is often a garbage-in-garbage-out (GIGO) without much quality. Whether Japan in the 1980-1990s or China in the 2000-2010s, economic growth was fueled mainly by bricks and mortar; a sharp rise was as easy as a sharp fall.

When encountering abnormal profits, financial returns, or growth, always recall the law of one price. Always ask yourself why others are making 1-3 percent growth, but you have 10-15 percent.

Either you are spending your past (from savings), gaining from your neighbours (the so-called beggar-thy-neighbour), or spending your future (from borrowings). Fair to say, the exceptional low growth during Mao’s era saved China quite some potential after 1978. But the real estate boom since 2003 and especially after 2008 seemed to exhaust their future significantly.

Borrowings result in debt, which has to be paid back ultimately. The experience in the 2010s seemed to suggest this would not happen—a miracle of no repay needed. Now it becomes another miracle instead—an unprecedented twin crisis. Maybe not. This is not new in history but has been repeated many times before. Without going too far back, Japan experienced it in the early 1990s, Asia ex-Japan experienced it in the late 1990s, the U.S. experienced it in the late 2000s, and Europe experienced it in the early 2010s. Cases were abundant every decade.

An appropriate case should be Japan since the nature of the two countries as well as the scale of the bubble are highly similar. U.S. experience showed that eight years was needed to clear the leverage—from mid-2006 when housing prices peaked to mid-2014 when its unemployment rate returned to below seven percent.

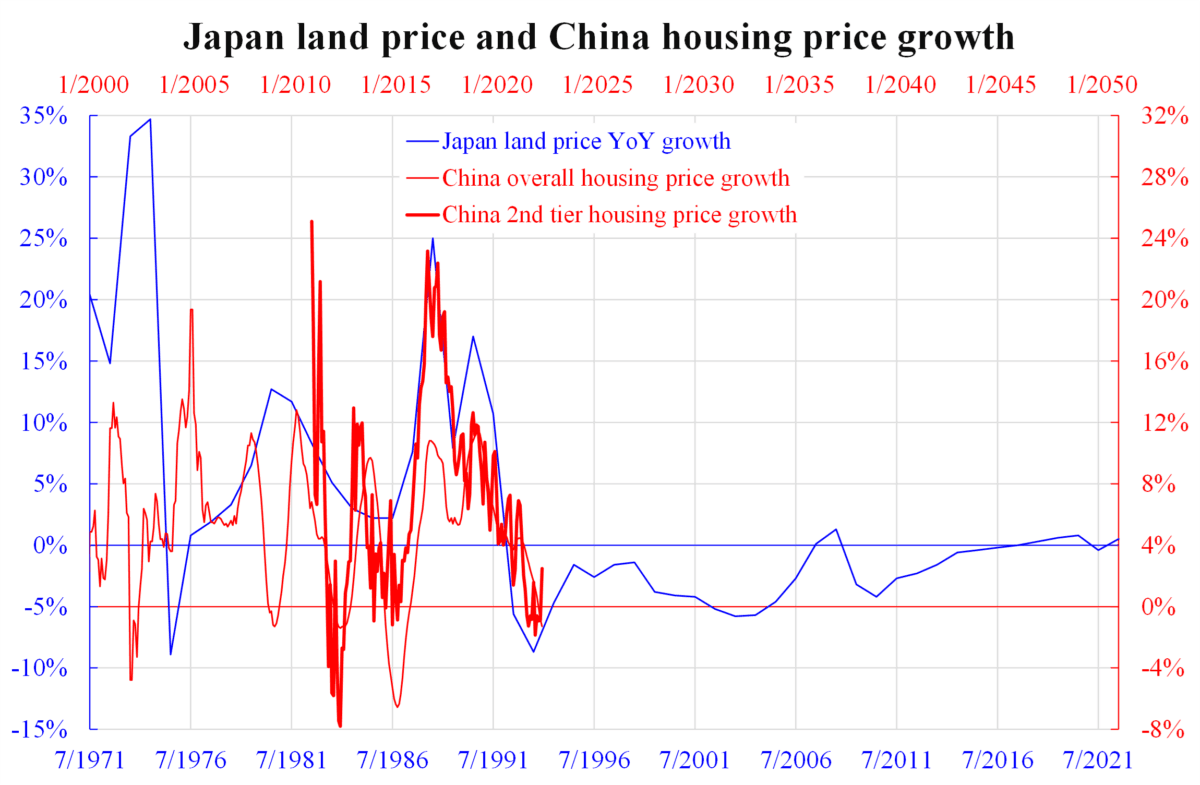

Japan did not publish housing prices but land prices in the past. The accompanying chart shows China is now stepping on Japan’s footprint of 28-29 years ago. The similarity looks amazing should the second-tier housing price (house prices in second-tier cities) be used.

The worst time seems to have just passed, but without allowing a sharp price crash, correction is bound to take an extended time. A prolonged gloom will last another decade or two until the 2030s or even 2040s to fully repay.

Friends Read Free