The central bank of China probably regrets having released this one last data point before the Chinese New Year on Feb. 8. The celebrations could have been so much nicer without it.

Some analysts estimated Chinese intervention in the currency markets in January was as high as $185 billion, intervention that burns through China’s foreign currency reserves.

According to the latest data released by the People’s Bank of China (PBOC) just before the new year, these estimates were a bit too high, but still. China lost $99.5 billion of its foreign exchange stash, which now totals only $3.23 trillion.

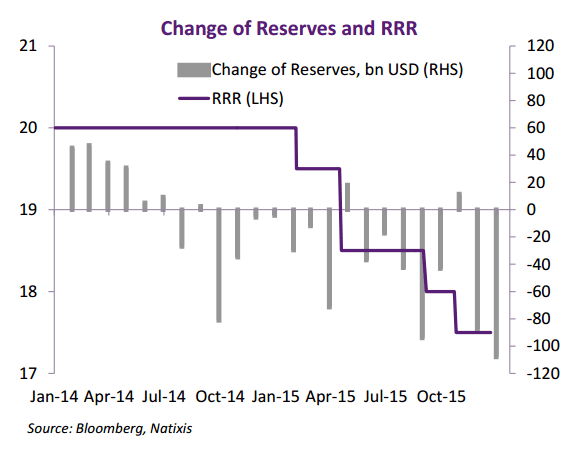

There were several hints that China would bleed more reserves in January, which is not exactly the same as intervention in the currency markets but is a good indicator. For instance, the PBOC pushed $233 billion into the domestic financial system in January.

This is the highest number in years, and the extra liquidity is supposed to make up for foreign exchange sales, which shrink the central bank’s balance sheet and drain liquidity from the banking system.

When the central bank sells dollars to prop up the exchange rate, it has to buy yuan from whoever wants to buy the dollars. Those yuan then vanish from the financial system in an accounting exercise on the PBOC’s balance sheet. This exercise has a negative effect on liquidity in the financial system and by extension the whole economy.

This is why China has to inject massive amounts of new yuan into the system and lower interest rates as well, which ironically leads to more pressure on the exchange rate.

As to actual capital flows for January, we won’t know until data on foreign direct investment as well as the trade balance come out later in February. Usually those bring dollars into the country, and a very simple estimate of capital flows just adds the drop in foreign exchange on top of those two numbers. Foreign direct investment usually adds $100 billion, whereas the trade balance averages around $50 billion. Unless there are significant changes in these numbers, total outflows could be as high as $250 billion.

There are other numbers that influence the reserve figure, such as currency moves which influence the total value of China’s portfolio. It also includes assets denominated in other countries, although the exact composition is a secret.

The International Institute of Finance recently used a more elaborate method to estimate that $676 billion of capital left China in 2015, but the country sold only $513 billion of reserves over the same period, which are also subject to valuation effects.

“With such leaky capital controls, China’s war chest of $3 trillion won’t be enough to hold down the fort indefinitely. In fact, the more people worry that the exchange rate is going down, the more they want to get their money out of the country immediately,” writes Harvard professor Kenneth Rogoff on Project Syndicate.

As to who is moving the capital out of the country, Goldman Sachs has a pretty good idea.

“The estimates, though, do seem to suggest that the incentive for Chinese residents to accumulate foreign assets appears to be the biggest swing factor to the capital flow picture and the trajectory of the yuan,” a report states.

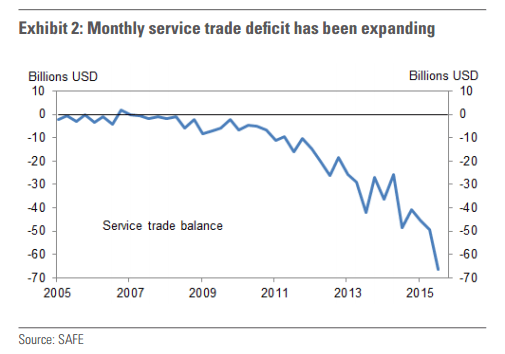

One preferred method for getting money out of a country with capital controls is overpaying for services abroad (mostly tourism), which created a pretty suspicious service sector deficit recently. In fact, the service sector deficit for 2015 was a record $137 billion, up 14.6 percent over the year.

And it gets even worse. If China didn’t have capital controls, which it has been tightening recently, Goldman thinks its citizens would invest 60 percent of GDP abroad. That’s more than $6 trillion and too much for China’s foreign exchange reserves.

Friends Read Free